How Smart Beta has Performed Amid the Volatility

Blog post

February 16, 2016

MSCI Factor indexes diverge in performance. Minimum Volatility outperforms significantly.

February 16, 2016

The fitfulness of the global recovery has produced quick and unexpected changes in financial markets and handed portfolio managers the challenge of allocating assets amid the market stress.

A review of performance of the MSCI Factor Indexes from the start of the year through Friday shows the strong outperformance of low-volatility despite investors having bid up the insurance-like protection that it aims to offer.

MSCI Factor Indexes are rules-based indexes that represent the returns of systematic factors, such as low volatility, value and quality, that have historically earned a persistent premium over long periods of time.

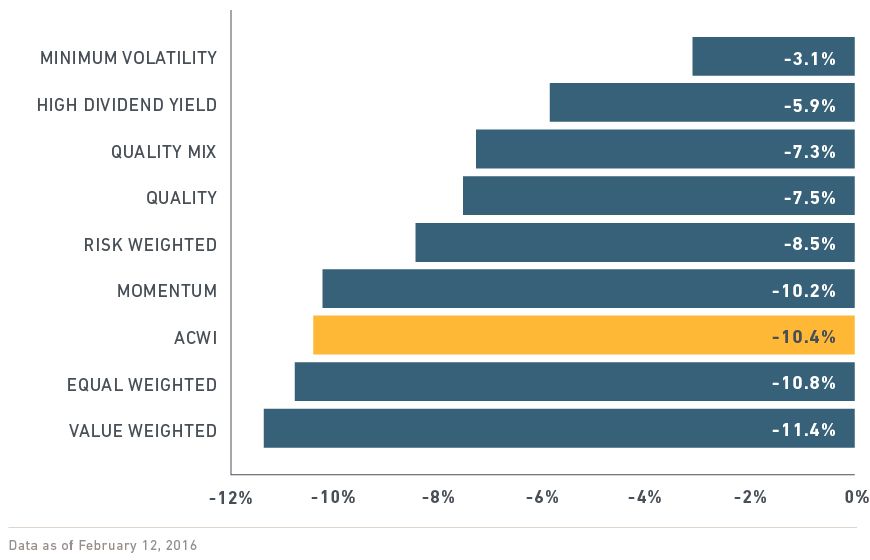

As the chart below shows, the MSCI ACWI Minimum Volatility Index closed Friday down 3.1% (in USD) since January 1, compared with a falloff of 10.4% of the global market, as measured by the MSCI ACWI Index, since the start of the year.1

Year-to-date performance of the MSCI Global Factor Indexes (in USD)

Since January 1, the Minimum Volatility Index, which is designed to reduce risk, has outperformed the MSCI ACWI Index across countries and regions, including +5.6% in the U.S., +4% in Europe and +4.2% in emerging markets.

The High Dividend Yield and Quality Indexes also have demonstrated resilience this year, with High-Dividend Yield down 5.9% and the Quality off 7.5%.

The Value Weighted Index, which emphasizes stocks with lower valuations, has performed worst, with a drop of 11.4%.

Are valuations stretched?

Comparing valuation levels across factor indexes is not straightforward. That's because simply looking at current valuation ratios such as price-to-book or price-earnings will always show the Value factor to be low-priced.

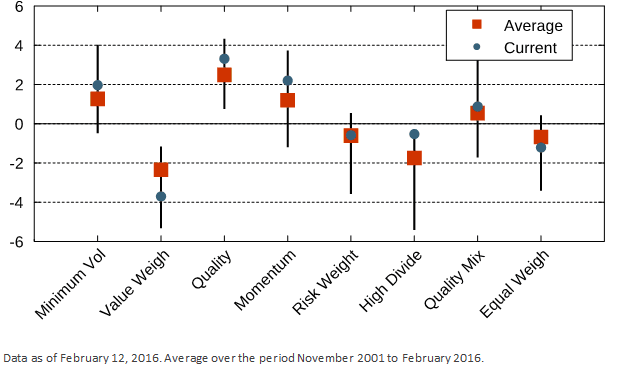

To overcome this hurdle, we compare the valuation levels of each of the factor indexes relative to its history.

Valuation levels for MSCI ACWI Factor Indexes relative to 15-year history

Based on price to earnings, price to book value, price to cash earnings and price to sales at month end dates. Values below 0 indicate the factor is cheaper than the parent. A current value below average indicates that the factor is cheap relative to its own history. The line endpoints indicate historical minima and maxima.

As the chart above shows, the MSCI Value Weighted Index, as of Friday, was relatively inexpensive compared with its history. The High Dividend Yield, Quality, Momentum, and Minimum Volatility Indexes all were relatively expensive compared with their averages over the longer term.

Still, none of the strategies has attained an extreme valuation relative to its history over the past 15 years.

Note, too, that a relatively rich valuation did not diminish the effectiveness of Minimum Volatility. The value of the insurance against volatility that the tilt toward lower risk aims to provide exceeded the run-up in valuation during the current period of high volatility.

These defensive characteristics may explain why many pension funds around the world have used Minimum Volatility strategies in conjunction with higher-beta options such as Value or Momentum in their multi-factor allocations.

Further reading:

Constructing Low-Volatility Strategies, January 2016 – Describes rules-based and optimization-based approaches to constructing low-volatility strategies

MSCI, A Leader in Factor Indexing

1 For the performance of MSCI Factor Indexes over their histories,

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.