Is Japan’s “lost decade” Over?

Blog post

August 14, 2018

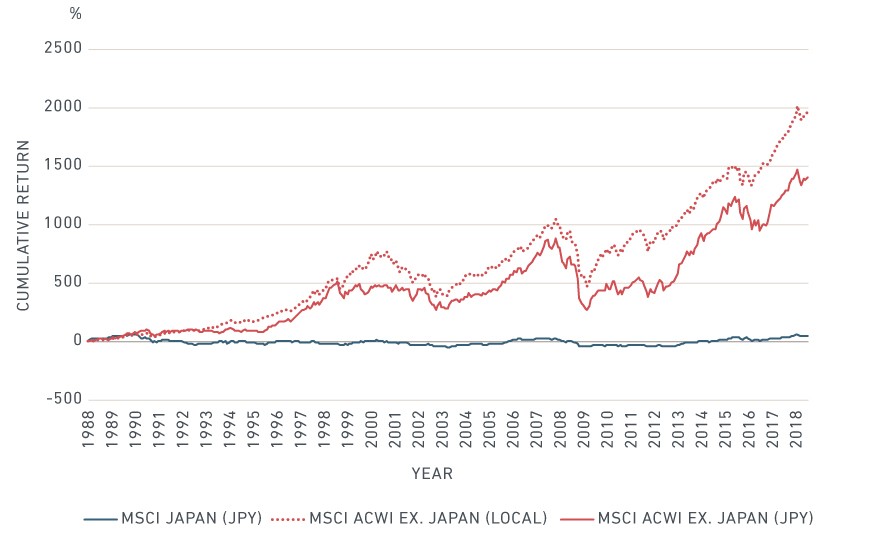

The Japanese equity market's spectacular crash in the early 1990s is referred to as the "lost decade." Recently, this period has been extended to include the decade that followed. Despite this, most Japanese investors continue to favor an outsized domestic equity allocation. This home bias has come with a huge opportunity cost. Since the end of 1987, the cumulative return of global stocks was over 1,400% in yen terms, while the cumulative return of Japanese stocks was only 49%.

CUMULATIVE STOCK RETURN OVER LONG-TERM (GROSS TOTAL RETURN)1

Data from December 1987 to June 2018

REDUCING HOME BIAS

Diversifying assets internationally offers a way to access a broad array of return sources. Many institutional investors in Japan have reduced their home bias equity allocation in recent years. However, the degree remains significant. For example, the domestic equity allocations of Japanese public pension plans is about 50% compared to the country's 8% market capitalization weight in the global equity market.2 While this home bias may reflect institutional investors' investment beliefs and constraints, retail investors typically do not face such limitations.

DIVERSIFYING THROUGH GLOBAL INVESTMENTS

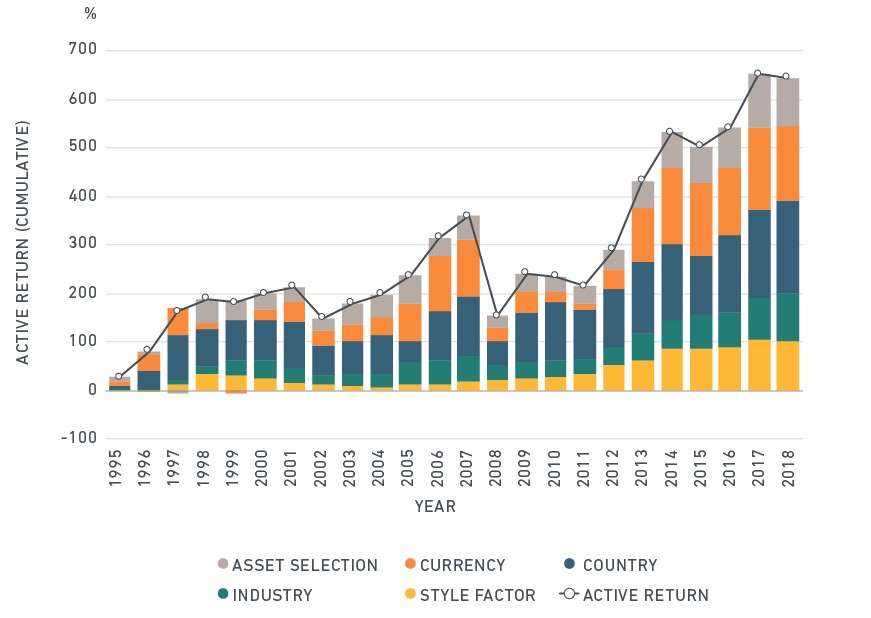

Comparing the sources of return for the MSCI ACWI ex Japan Index against the MSCI Japan Index shows that diversifying exposure to different countries, currencies, style and industry factors has been beneficial historically.

ACTIVE RETURN OF MSCI ACWI EX. JAPAN AGAINST MSCI JAPAN

Return attribution analysis by MSCI's Barra Portfolio Manager using MSCI's Long-Term Global Equity Model (GEMLT), for which data is available beginning December 1994. Data shown is from December 1994 to June 2018.

HOW MUCH HAS CHANGED IN THE JAPANESE MARKET?

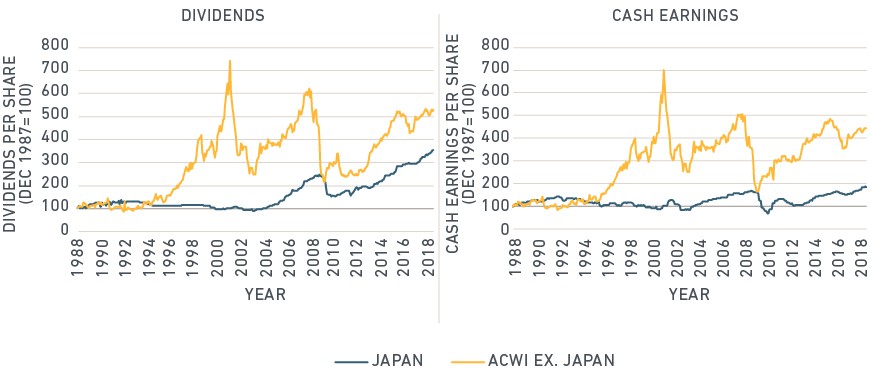

The 1990s collapse of the Japanese equity market followed a huge bubble in equity and real estate prices. However, there has been significant reforms since that era: the recent focus on sustainability and ESG issues is a prominent example. However, as the following exhibits show, there are still sizeable gaps in fundamentals as measured by companies' ability to generate cash flows and reward shareholders.

Fundamentals reveal gaps between Japanese and international firms

Data from December 1987 to June 2018

DÉJÀ VU?

Looking at the makeup of the MSCI Japan Index is also revealing. Nearly 40% of current MSCI Japan Index constituents were also in the index in 1988, while the figures for the MSCI Kokusai Index and MSCI Emerging Markets Index are only 21% and 2.5%, respectively. These companies accounted for 56% of the free-float market capitalization of the MSCI Japan Index, compared to 34% and 3.1% for the MSCI Kokusai Index and MSCI Emerging Markets Index, respectively as of June 2018.

There were numerous factors that contributed to Japan's lost decades. However, given the potential benefits of a globally diversified portfolio and the still-sizeable gaps in the fundamentals between Japanese and international companies, is continued reliance on domestic stocks the wisest way forward?

Further Reading

Subscribe todayto have insights delivered to your inbox.

1 MSCI ACWI ex Japan Index is a market-capitalization-weighted combination of the MSCI Kokusai Index and MSCI Emerging Markets Index.2 Based on the MSCI ACWI Index, as of June 29, 2018

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.