Navigating market volatility with agency MBS models

Blog post

February 26, 2020

- Volatility in the agency MBS market in 2019 provided comprehensive tests for risk management models.

- The strength of the summer refinance wave and higher stratification of prepayment across MBS pools underscored the importance of modeling refinance regimes and prepayment burnout.

- High volatility in rates and MBS basis made effective MBS hedging difficult, and also demonstrated the importance of benchmarking model durations against market-price dynamics.

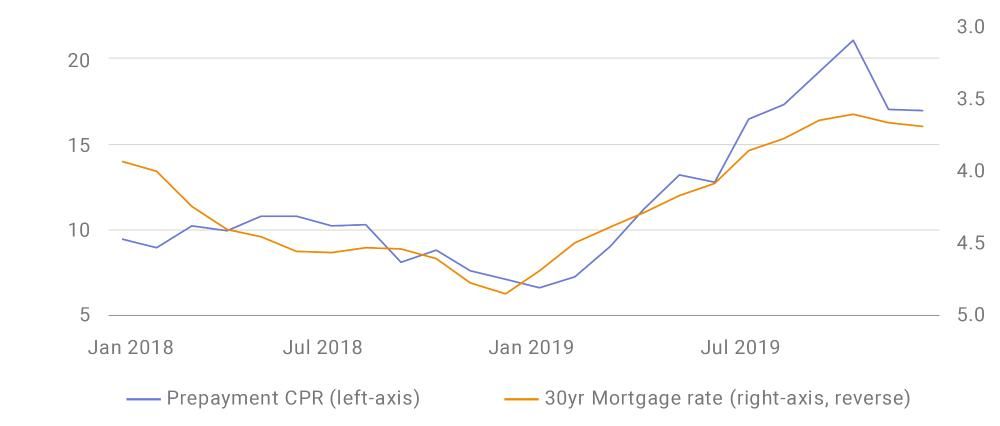

Mortgage rates and basis had significant volatility …

… and prepayment surged as rates approached historical lows

Regulators often require models to be reviewed and updated annually to identify potential model risks.4 MSCI's annual review of its agency MBS model's performance and acceptance uses three criteria: prepayment forecasts, model durations and the value-at-risk (VaR) measure.

Prepayment-forecast error tracking

We reviewed the MSCI model's prepayment forecasts along vintage coupon cohorts, as well as using the rank-based method. The exhibit below shows the average absolute error weighted across all major vintage coupon cohorts. The error was around 0.2 single monthly mortality (SMM), which fell within the acceptance criteria. The model forecasted the summer refinance peak performances within 0.2 SMM.

The model anticipated the 2019 summer refinance wave

Overall model performance: 6-month error unpaid principal balance weighted across all major vintage coupon cohorts for 30-year universe.

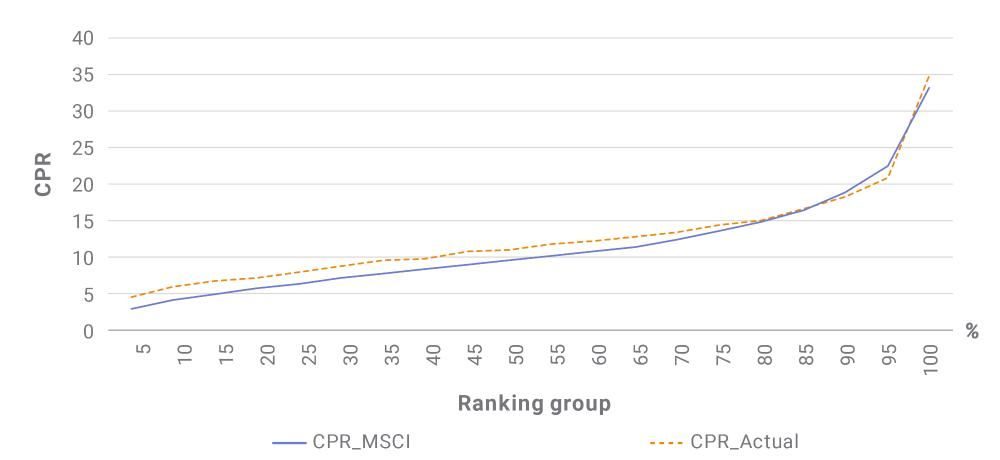

MBS pools and securities have diverse collateral attributes. They also have diverse prepayment performance across different macroeconomic environments — for example, rate rallies and selloffs. Applying a rank-based error-tracking methodology,5 the exhibit below shows the average absolute error is 0.12 SMM (within the model's acceptance criteria) across 200 rank buckets (every 0.5% universe).

Model captured the differentiation between the fastest and slowest prepayment pools and periods

Rank-based error tracking for overall FNCL universe 2019 model performance.

The model was generally able to differentiate the historical prepayment behavior across pool attributes, as well as the refinance waves. The model forecasted the peak speeds relatively well, which were generally observed in the fastest pool cohorts (for example, seasoned large-loan-size refinance pools with the highest weighted average coupon and FICO score) during the summer refinance months.

This is attributed to two model features: the refinance regime and prepayment burnout.6 While mortgage rates in 2019 were comparable to 2016 levels, the agency mortgage universe outstanding was different. Mortgage brokers were much more active in 2019 and their prepayment behavior was much more aggressive. Burnout modeling was also important for 2019, as the majority of seasoned MBS had previous refinance opportunities. We argued in our model review that the traditional cumulative-incentive approach to model burnout might not have been adequate for projecting the 2019 refinance wave.

Duration backtesting

MBS valuation and risk measures can be partially driven by prepayment-model assumptions that are not entirely determined by historical data. Many of these model features are forward-looking and based on assumptions of secular trends in the mortgage industry — for example, long-term mortgage primary-secondary spreads7 and long-term prepayment regimes due to credit policy and technology advancements.8

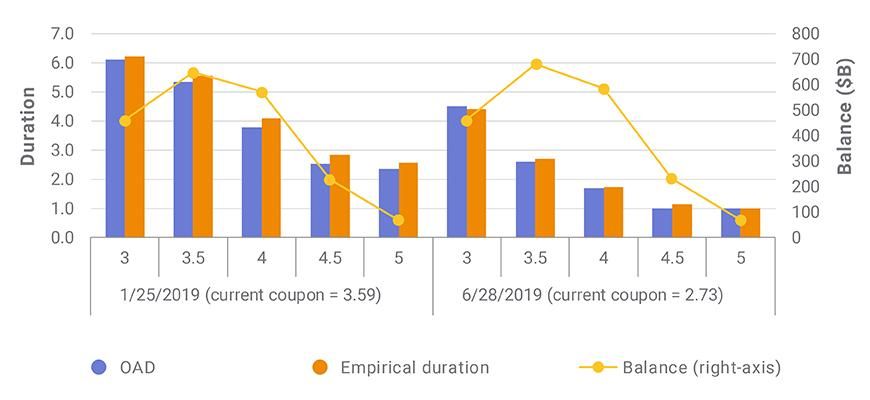

These model assumptions are checked against market views reflected in the price dynamics. Here we compare the model durations versus the empirical durations for to-be-announced (TBA) prices. The exhibit below shows these durations are generally consistent for the relatively high rate levels on Jan. 25, 2019, as well as for the rate rallies around June 28, 2019.

Checking the MSCI MBS model's duration against empirical duration

Model durations versus empirical durations on Jan. 25, 2019, and June 28, 2019.

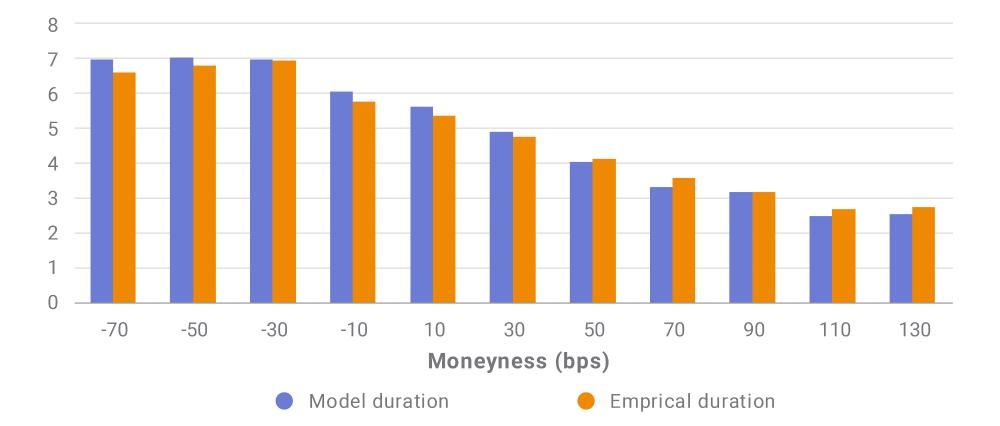

In the exhibit below, we bucket these duration comparisons for all TBAs across rates scenarios in 2019. It shows the model produced market-expected price dynamics across the volatile rates environment in 2019.

Model durations were consistent with empirical durations across moneyness buckets

A comparison of model duration versus empirical duration for all TBAs across all rate scenarios in 2019, bucketed based on moneyness of the coupons, defined as the difference between the TBA coupons and current coupons.

Empirical MBS durations are also affected by factors other than prepayment behavior — e.g., supply/demand issues and the prepayment-uncertainty risk premium. For example, TBA empirical durations significantly extended during the "taper tantrum" episode, and the period of the Fed's MBS QE uncertainties around July 2019.9 The occasional gaps between model durations and empirical duration need to be examined and understood in this context.

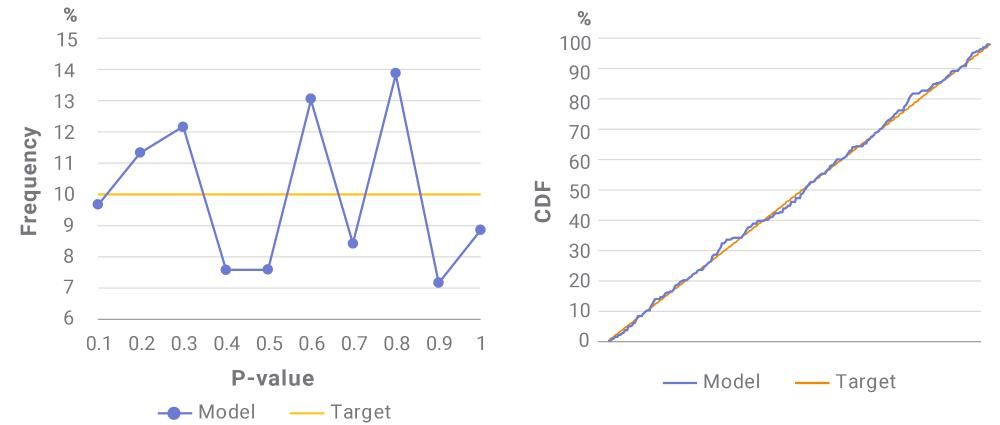

Accuracy of MBS VaR

VaR modeling needs an accurate pricing model and generally requires the risk factors to exhibit a stationary property.

We tested the p-value of the option-adjusted spread's (OAS) daily change against the uniform distribution.10 The exhibit below shows this distribution for Fannie Mae 30-year coupon 4 in 2019. The Kolmogorov-Smirnov statistics for the cumulative distributions was 0.038, within the acceptance criteria.

Model-risk factor is stationary and suitable11 for risk forecasts like VaR measure

P-value of the FNCL 4s OAS daily change compared with the uniform distribution (left). The Kolmogorov-Smirnov statistics for the cumulative distribution is computed at 0.038 (right).

10This is similar to the Basel Committee on Banking Supervision's standards.

11We tested for model "suitability" using the p-value test, which compared the model-based frequency and the targeted frequency.

Further Reading

MSCI agency MBS model performance review 2019 (client access only)

MBS prepayment in 2020: Looking back, looking ahead

Is MBS refinance risk increasing?

How mortgage fees affect rates and spreads

A reality check for MBS duration risk

MBS investors: quantitative easing déjà vu?

MBS prepayment modeling: AI 1, Humans 0?

Subscribe todayto have insights delivered to your inbox.

1 Zhang, J. 2020. “MSCI Agency Prepayment Model Performance Review 2019.” MSCI Model Insight. (Client access only.)2Mortgage basis, or the spread between MBS and Treasurys, is a common gauge of the attractiveness of the U.S. mortgage market.3Goldfarb, S. “Mortgage Bonds Attract Investors in Low-Yield World.” , Dec. 27, 2019.4See, for example: “SR ll-7: Guidance on Model Risk Management.” Federal Reserve Board and Office of the Comptroller of the Currency, April 4, 2011.5Zhang, J. 2019. “MSCI Rank-Based Error Tracking for Agency MBS Prepayment Models.” MSCI Model Insight. (Client access only.)6For details, see: “MSCI Agency Prepayment Model Performance Review 2019.”7Yu, Y. “How mortgage fees affect rates and spreads.” MSCI Blog, Feb. 7, 2019.8Zhang, J. “Is MBS refinance risk increasing?” MSCI Blog, Oct. 12, 2018.9Zhang, J. “MBS investors: quantitative easing déjà vu?” MSCI Blog, Sept. 5, 2019.Zhang, J.MSCI Blog, Sept. 5, 2019.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.