- An approach combining high conviction with a hypothetical factor-index-based portfolio delivered more balanced factor exposure and higher average returns than a pure high-conviction approach, during our study period.

- Combining a diversified model portfolio based on MSCI High Dividend Yield Indexes and high-conviction yield portfolios delivered a high-dividend-yield outcome efficiently over the period of analysis.

- Overlaying active/discretionary with a minimum-volatility allocation historically led to better return and reduced risk, especially during periods of heightened volatility.

Raising the Barbell for Equity Investing

For example, could investors use a "barbell" approach combining high-conviction ideas and a strategy that aims to replicate an index ("an index-based portfolio") to achieve desired outcomes?

We first looked at a generic case where investors were seeking to enhance returns through investing in the equity asset class. At each year-end from December 2009 to December 2019, we simulated hypothetical buy-and-hold high-conviction portfolios based on the top 15, 30 and 50 stocks that were commonly held by high-conviction equity funds.2 Then, for every simulation, we created 50/50 barbell portfolios by allocating 50% weight to the high-conviction buy-and-hold portfolios and 50% to a rebalanced portfolio that tracked the MSCI ACWI Diversified Multi-Factor Index over the one-, two- and three-year periods over the 10 years.3

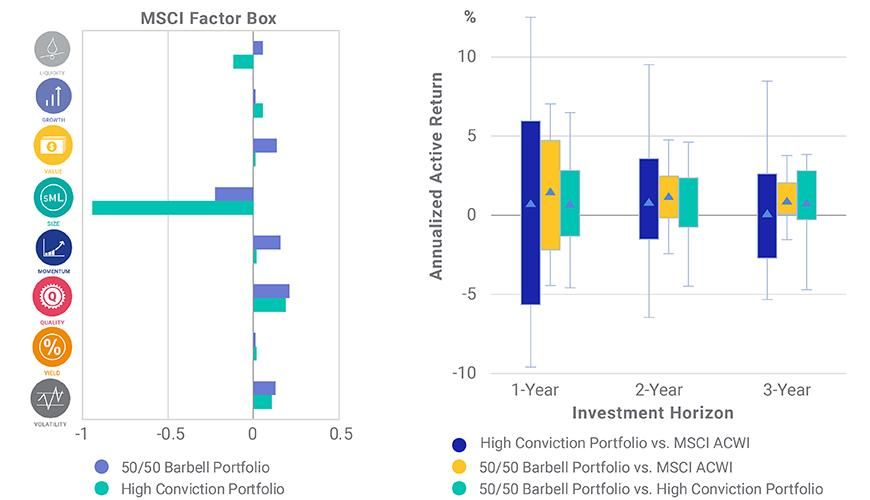

Breaking down those holdings by factors, using MSCI FaCS®, we see that, on average, the high-conviction portfolios were exposed to large-size, low-liquidity, high-quality and low-volatility factors. Comparably, the 50/50 barbell portfolios had a less significant bias to the size factor and higher exposure to value and momentum.

In terms of performance, the high-conviction portfolios, on average, outperformed the MSCI ACWI Index by 0.77%, 0.85% and 0.13% per year, respectively, over a one-, two- and three-year investment horizon.

But we found even stronger results when we compared the 50/50 barbell portfolios to the MSCI ACWI Index. In that case, the barbell portfolio outperformed the MSCI ACWI Index by 1.51%, 1.21% and 0.93% per year, respectively, over the same periods with lower tracking error. In addition, the 50/50 barbell portfolios outperformed the high-conviction portfolios in 59%, 67% and 63% of the simulated results, respectively, over one-, two- and three-year investment horizons.

Barbell Versus High-Conviction Buy-and-Hold: FaCS Exposure and Performance

The 50/50 barbell portfolio refers to simulated portfolios that allocated 50% weight to the high-conviction buy-and-hold portfolios and 50% to a rebalanced portfolio that tracked the MSCI ACWI Diversified Multi-Factor index. The blue triangle marker denotes the mean of each box.

Investing for an Outcome of Income

What about wealth investors investing for sustainable income? Could an index-based high-dividend-yield model portfolio have complemented a high-conviction approach?

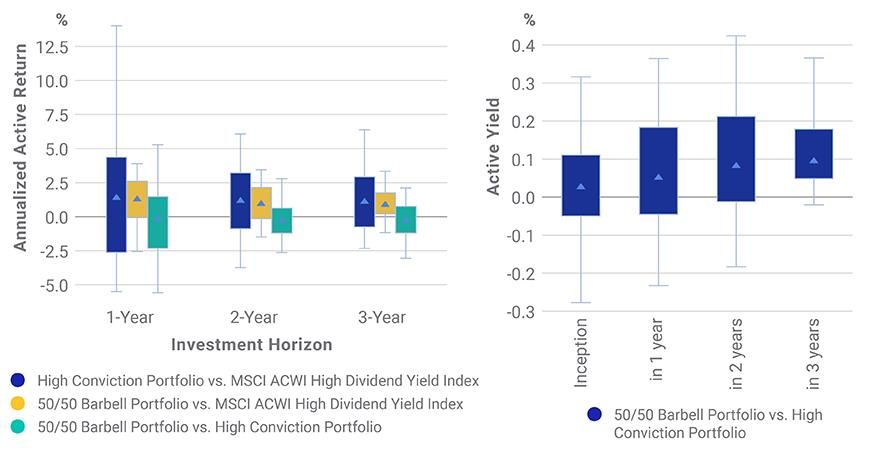

Similar to our methodology in the previous example, we simulated hypothetical buy-and-hold high-conviction high-dividend-yield-focused portfolios at each year-end based on top 15, 30 and 50 stocks that were commonly held by high-conviction global equity dividend funds from December 2009 through December 2019.4 Then, for every simulation, we created 50/50 barbell portfolios by allocating 50% weight to the high-conviction buy-and-hold yield portfolios and 50% to a rebalanced model portfolio that tracks a basket of MSCI High Dividend Yield Indexes over the following one-, two- and three-year periods.5

The exhibit below shows that while the historical performance of the 50/50 barbell portfolios were largely on par with the high-conviction portfolios, the yield outcomes differed.

On average, the 50/50 barbell portfolios improved yields by 5.4 basis points (bps), 8.4 bps and 9.7 bps per year, respectively, compared to the high-conviction buy-and-hold portfolios over the one-, two- and three-year investment horizons. In addition, the 50/50 barbell portfolios' yield enhancement increased with investment horizon.

Barbell Versus High-Conviction Buy-and-Hold: Performance and Yield

The 50/50 barbell portfolio refers to portfolios that allocated 50% weight to the high-conviction buy-and-hold portfolios and 50% to a rebalanced model portfolio created according to endnote 6. The blue triangle marker denotes the mean of each box.

What About Integrating a Minimum-Volatility Tilt into Private Wealth Portfolios?

Some growth-oriented wealth investors could be concerned with heightened market volatility during COVID-19 and the potential negative impact on the performance of their equity portfolios. In this case, we looked at overlaying high-conviction holdings (either in active funds or discretionary portfolios) with a minimum-volatility approach.

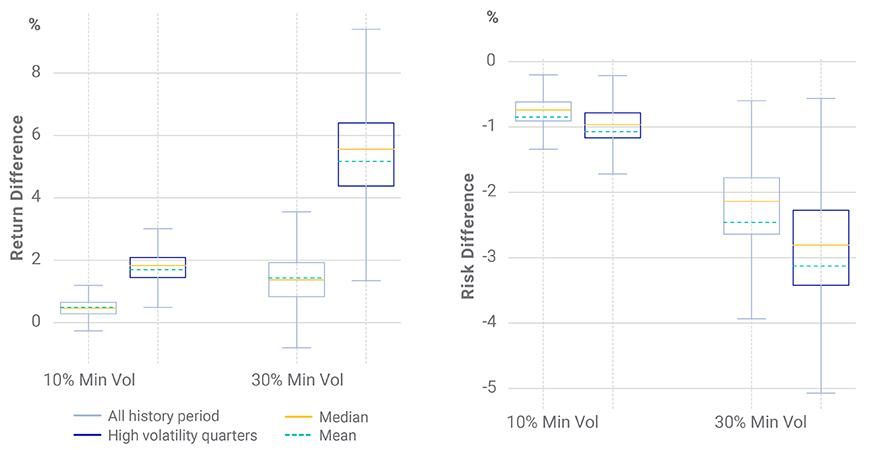

We examined two scenarios: allocating 10% and 30%, respectively, to investments that track the MSCI ACWI Minimum Volatility Index and the rest to an active global equity fund during the sample period from December 2009 to March 2020.6

The exhibit below shows that a 10% allocation to a minimum-volatility tracking portfolio, increased returns in 91% and 97% of the cases, over the full sample period and during periods with elevated market volatility, respectively.7

Overlaying an Active Approach with a Minimum-Volatility Allocation

With a 30% allocation, we saw return enhancement and risk reduction for 90% of the active equity funds during the full sample period: The average return enhancement was 1.4%, and the average net risk reduction was 2.5 percentage points. Both results were more pronounced during periods of elevated market volatility: The average return enhancement was 5.1%, and the average net risk reduction was 3.1 percentage points.

A Strengthened Approach?

Despite being a relatively new concept to private wealth investors, factor investing has some similarity to an outcome-oriented investing approach in achieving targeted outcomes such as equity growth, yield enhancement and risk mitigation. While a high-conviction and active approach could offer simplicity and the potential to harvest alpha, an index-based approach may deliver greater transparency in portfolio construction and higher investment capacity than the high-conviction approach we analyzed. And, as we've seen, a barbell strategy that combines both approaches could have helped achieve a variety of targeted outcomes efficiently.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1Outcome-oriented investing is an investment approach that considers achievement of desired outcomes in addition to return and risk objectives. See, for example: Invesco, “Prioritizing Outcomes and Setting a Plan: Portfolio managers must strike a delicate balance to reach investment goals.” , Feb. 5, 2019.2Based on MSCI Peer Analytics Fund Database and Eikon Lipper, we screened for active global equity funds with 5 to 70 stocks and assets under management (AUM) above USD 100 million. The analysis simulated buy-and-hold portfolios in each year-end and looked at the first two years of performance. This is to mimic private wealth investors who prefer to hold securities longer than a year without rebalance.3MSCI ACWI Diversified Multi-Factor Index is an optimized index that seeks to maximize exposure to value, momentum, low size and quality while maintaining a similar risk profile to its parent index.4Based on MSCI Peer Analytics Fund Database and Eikon Lipper, we screened for active global equity funds, with 5 to 70 stock holdings and fund AUM above USD 50 million. Further, we focus on fund names with keywords such as “Yield,” “Income” and “Dividend.”5In this example, the high-dividend-yield model portfolio comprised: 50% in the MSCI North America High Dividend Yield Index, 15% in the MSCI Europe High Dividend Yield Index, 15% in the MSCI Pacific High Dividend Yield Index and 20% in the MSCI EM High Dividend Yield Index. The model portfolio is rebalanced monthly. The model approach allows for tactical rebalance of the regional blocks based on investors’ preferences and views. The MSCI High Dividend Yield Indexes aim to reflect the opportunity set of companies with high dividend income and quality characteristics that pass dividend-sustainability, persistence and quality screens.6Based on MSCI Peer Analytics Fund Database and Eikon Lipper, we screened for active global equity funds with AUM bigger than USD 100 million.7High-volatility quarters refer to those with realized annualized volatilities higher than 15%.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.