Robust Selection Paid Dividends

Blog post

May 22, 2020

- Following the economic slowdown caused by COVID-19, many companies across the world postponed, canceled or reduced their dividends.

- In the MSCI ACWI Index, consumer discretionary was the sector affected most: 20% of firms canceled dividends from the end of February to the end of April.

- Compared to a simple approach of dividend-yield ranking, a dividend-yield-focused strategy that screened for financial quality and dividend persistence and sustainability had less exposure to companies impacted by dividend cancellations.

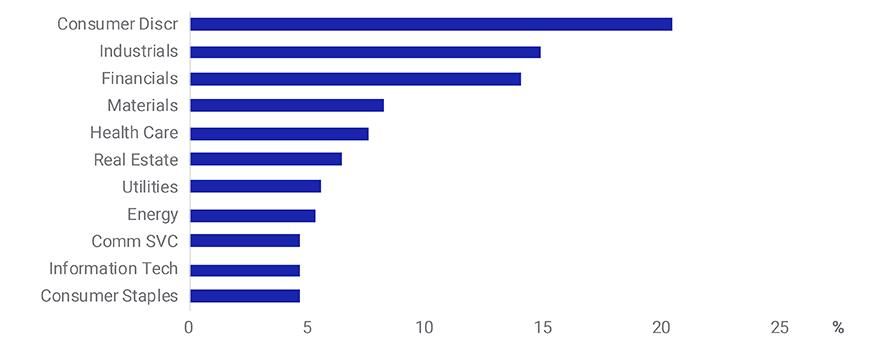

Consumer-Discretionary Companies Were Most Affected by Canceled Dividends

Consumer discretionary was the sector most impacted, with 20% of companies canceling dividends. The current economic situation is striking: Even in the worst financial crises historically, there has rarely been a situation of almost zero revenues. However, it is not entirely surprising that companies have chosen to postpone, cancel or reduce dividends to conserve cash and aim to survive the economic slump, given the nearly complete absence of guests (for hotels), visitors (for resorts and theaters) or customers (for retail shops). Air travel was severely impacted during the period as well, and companies classified in the related sub-industries (aerospace & defence, airport services, airlines and air freight & logistics) were some of the main contributors to dividend cancellations in the industrials sector.

Additionally, the financials sector was affected by the recommendations or directives from various regulators asking companies to consider cutting their dividends, such as with banks in the United Kingdom.1

Proportion of Companies (by Number) in the MSCI ACWI Index that Canceled Dividends, by Sector

Based on data as of April 30, 2020.

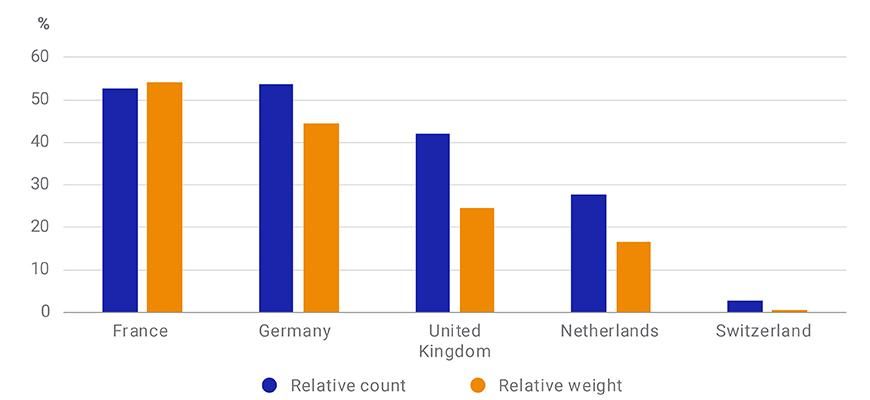

Canceled Dividends Hit European Companies the Hardest

Comparing across regions, Europe saw the highest impact in terms of the relative weight of companies in each region that canceled dividends. Among the top five countries weighted by free-float market cap in the MSCI Europe Index, France saw the highest impact, with around 50% of the companies by weight canceling dividends.

Dividend Cancellations for Top Five European Countries by Relative Count and Index Weight

Based on data as of April 30, 2020.

Quantifying the Impact of the Dividend Cuts

To assess the magnitude of the dividend cuts, we looked at dividend yield for the MSCI ACWI Index from the end of February 2020 to the end of April 2020. We see that the dividend yield decreased to 2.42% from 2.6% during this period, despite a 4.6% price drop. While the price impact resulted in a yield increase of 13 basis points (bps), it was more than offset by a 31-bp drop from the dividend cuts.

Dividend Yield of the MSCI ACWI Index Fell between February and April

Based on data from February through April 2020.

Could Investors Have Avoided Some of the Impact of Dividend Cancellations?

The possibility of encountering such a situation has important implications for dividend-yield strategies that aim to provide regular income to investors. As we highlighted in an earlier blog, while a simple dividend-yield-based selection strategy gave slightly more exposure to the dividend factor, it resulted in lower realized yield during periods of high market volatility than a methodology that incorporated additional screens, such as the one used for the MSCI ACWI High Dividend Yield Index.

We analyzed whether that finding held during the COVID-19 crisis. To do so, we replicated a simple strategy of holding the same number of stocks as the MSCI ACWI High Dividend Yield Index (593, as of the last rebalance in November 2019) selected in decreasing order of their dividend yield to create a "Top Dividend Basket."

For this Top Dividend Basket, we note that it held 89 companies representing 16.5% of the aggregate market-cap weight of companies that canceled dividends. The MSCI ACWI High Dividend Yield Index, on the other hand, included only 72 companies representing 5.9% of the weight.

One reason for this difference may be that the MSCI ACWI High Dividend Yield Index excluded some of the large companies from the banking and automobile-manufacturing sub-industries that were a part of the Top Dividend Basket. The MSCI ACWI High Dividend Yield Indexes Methodology selects potential constituents based on their dividend yield before applying a number of screens, including dividend sustainability, dividend persistence, price performance and quality.

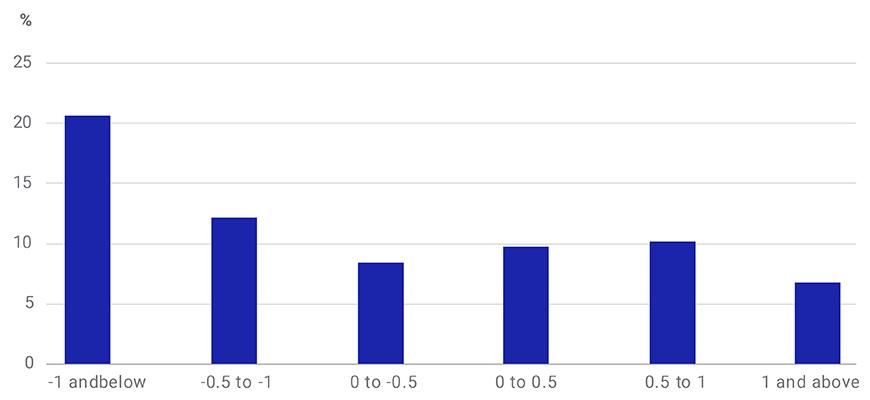

Assessing the Screen for Corporate Financial Quality

To assess the effects of a screen for financial quality, we divided the MSCI ACWI Index into six buckets based on quality z-score and calculated the weight of companies that canceled dividends in each bucket as a proportion of all the companies in that bucket. We find that as the quality score improved, the proportion of companies that canceled dividends during the recent crisis generally lessened.

The MSCI ACWI High Dividend Yield Index requires a minimum quality z-score of zero for new constituents (-0.5 for existing ones) and therefore did not include the companies in the lower-quality z-score buckets (i.e., buckets with the highest proportion of companies with dividend cancellations).

Quality Z-Scores and Weight of Companies that Canceled Dividends

Quality z-scores based on data as of Oct. 31, 2019. These scores were used in the construction of the MSCI ACWI High Dividend Yield Index at the November 2019 Index Review.

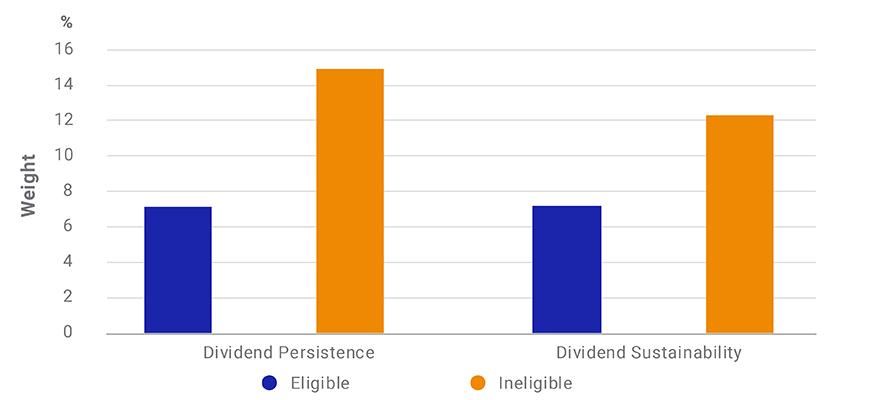

Assessing the Screens for Dividend Persistence and Dividend Sustainability

The dividend-persistence screen excludes securities that have a negative five-year dividend growth rate. To assess its effect, we divided the MSCI ACWI Index into two buckets based on whether a company passed the screen. Within the negative-growth-rate bucket, 14.9% of the companies by weight canceled dividends, as compared to 7.1% of companies that made it into the other bucket.

For the dividend-sustainability screen — which excludes securities that have either a negative, zero or a very high payout ratio (within the top 5% of securities by number within the universe of securities with positive payout) — we divide the MSCI ACWI Index again into two buckets, based on whether a company passed the dividend-sustainability screen. Within the bucket of companies not passing the screen, 12.3% of companies by weight canceled dividends compared to 7.2% of companies in the other bucket. The MSCI ACWI High Dividend Yield Index excludes companies that do not pass the dividend-persistence or -sustainability screens (i.e., the buckets with the highest proportion of companies with dividend cancellations).

Companies that Canceled Dividends Sorted by Dividend-Persistence and -Sustainability Screens

In periods of crisis, it has not been unusual to see companies postpone or cancel dividends to help conserve cash. Our analysis above highlighted how a strategy that screened for financial quality, dividend sustainability and dividend persistence resulted in a lower proportion of constituents that canceled dividends, relative to a simple yield-ranking strategy.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1“PRA statement on deposit takers’ approach to dividend payments, share buybacks and cash bonuses in response to Covid-19.” Bank of England, March 30, 2020.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.