Saudi Arabia inclusion and emerging markets

Blog post

March 28, 2019

Saudi Arabian stocks will be included in the MSCI Emerging Markets Index and the MSCI ACWI Index in a two-step process starting in June this year. With the first step of inclusion of the MSCI Saudi Arabian Index coming shortly, we ask how inclusion of this Middle Eastern market would have affected the MSCI EM Indexes.

Result of improved market access

The decision to include Saudi Arabia in the MSCI Emerging Markets Index was taken in consultation with international institutional investors. It followed a number of regulatory and operational enhancements in the Saudi Arabian equity market that effectively improved market access for such investors.1

Saudi Arabia's inclusion in the emerging markets (EM) index may provide expansion of the investment opportunity set, and the country has previously demonstrated diversification benefits. These include the market's past dividend yield, its distinct sector composition, low sensitivity to other emerging markets and its previous natural currency hedge.

Implementation – a two-step process

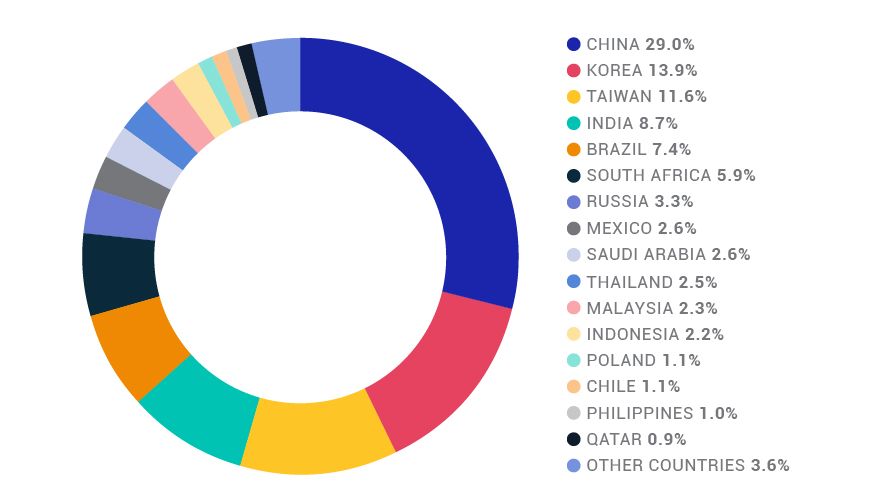

On a pro forma basis, the MSCI Saudi Arabia IMI will represent approximately 2.6% of the MSCI Emerging Markets IMI (which includes small-cap stocks) and will add 69 securities to the latter index. There will be a two-step inclusion process, at the May and August Semi-Annual Index Reviews.

Saudi Arabia's weight in provisional MSCI Emerging Markets IMI

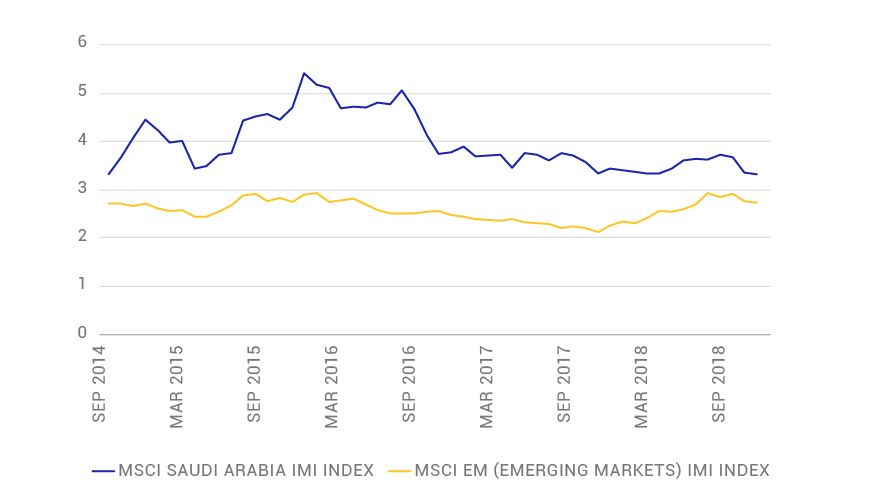

Recent Dividend Yields History

Though not an indicator of future yields or performance, Saudi Arabian equities offered above-average dividend yields for the available history since September 2014. Following the global financial crisis, central banks around the world tried to stabilize their respective economies by cutting their primary interest rates. In effect, these central bank actions made bond yields appear relatively less attractive, with many institutional and retail investors seeking exposure to high dividend-paying equities as a way of meeting their income needs. Over the last four years, Saudi Arabia's yield has, on average, exceeded the emerging markets' yield by 140 basis points (see exhibit below).

Saudi Arabian equity yields

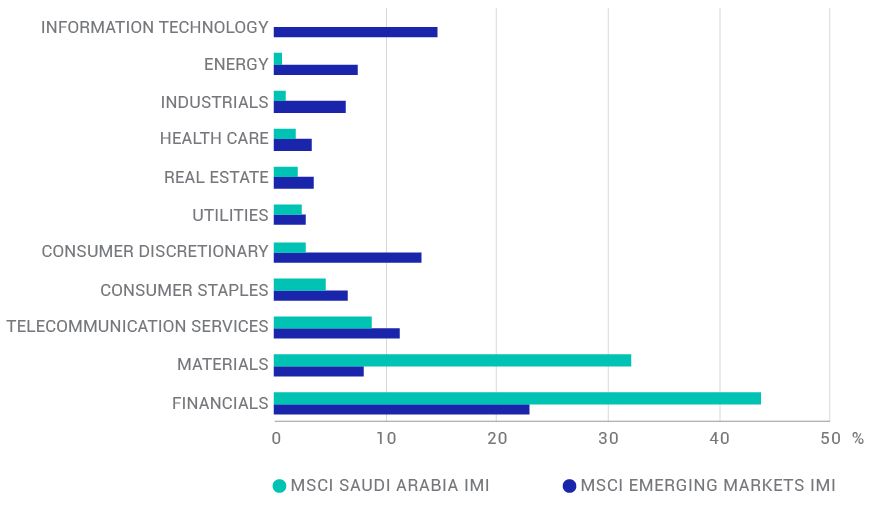

Distinct Sector Composition

Saudi Arabia has a distinct sector composition as compared to emerging markets as of Feb. 28, 2019. Financials and materials comprised more than 75% of the IMI, which could be regarded as a concentration risk for a standalone Saudi Arabia investor. However, for an EM investor, this has offered diversification opportunities, as this sector weighting is distinct from the sector composition of the MSCI Emerging Markets IMI. Information technology, which is generally one of the biggest sectors globally, had no representation in Saudi Arabia, while industrials and healthcare had relatively low exposures as well, as we can see in the exhibit below.

Saudi Arabia's sector exposures

This distinct sector composition contributed to Saudi Arabian equities' low correlation to other emerging markets, exhibiting low-to-negative correlation on a 1-year rolling basis (the correlation has increased more recently).

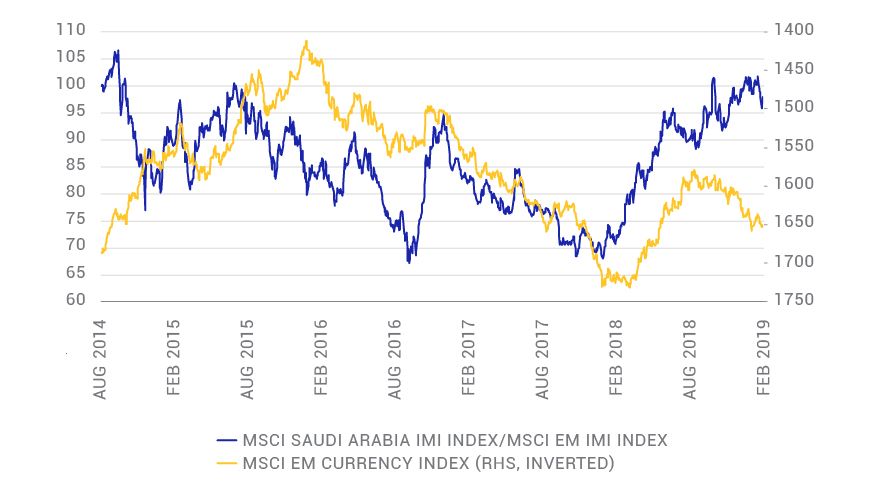

Performance as a natural currency hedge

While investing globally has historically yielded diversification benefits in terms of asset allocation, it also means investors are exposed to currency risk. Our analysis shows that since May 1994, the MSCI Emerging Markets IMI returned 8.0% on an annualized basis, in local currency terms. The USD returns were substantially lower at 5.0%. While this shortfall is hypothetical, as it is difficult to secure the local currency returns in each emerging-market country without bearing a hedging cost, it illustrates how currency depreciation has affected emerging-market investors.

As the Saudi riyal is pegged to the U.S. dollar, U.S. dollar investors were previously unaffected by the riyal's fluctuations with other currencies. While U.S. dollar appreciation impaired emerging markets in 2018, Saudi Arabia outperformed emerging markets as a whole. Currency was one of the main contributors to Saudi Arabia's outperformance in 2018, adding 4.3% to performance. From August 2014 through February 2019, the currency factor contributed 2.2% on an annualized basis.

Saudi Arabia performance during EM currency stress

Saudi Arabia's forthcoming inclusion in the emerging markets investment universe is part of a wider emerging markets story which includes China's recent inclusion. Like China, Saudi Arabia needed to satisfy many inclusion criteria prior to being included in emerging markets. Saudi Arabia's distinct sectoral composition and natural currency hedge have historically provided diversification benefits. Institutional investors may want to examine how the inclusion affects their portfolios.

The author thanks Raman Aylur Subramanian for his contributions to this post.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1 June 2018 Annual Market Classification Review. Saudi stocks will be added to other global and regional indexes as applicable.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.