Should bank-loan investors worry about liquidity risk?

Blog post

September 24, 2019

- We compared the liquidity of bank loans and high-yield corporate bonds during the December 2018 sell-off and found that transaction costs for bank loans increased by 140%, while those for the corporate bonds increased by only 20%.

- The market depth for bank loans also shrank by one-third, and the quoted-price uncertainty tripled — in contrast to high-yield corporate bonds, whose market depth remained stable and price uncertainty only doubled.

- This dramatic drop in the liquidity of bank loans during market distress suggests that investors may wish to consider bank loans' higher liquidity risk.

Costs increased …

In our analysis, we considered first- and second-lien B-rated U.S. term loans and B-rated U.S. high-yield corporate bonds. The two markets are both sizable, with USD 500 billion and USD 1.6 trillion for bank loans and high-yield corporate bonds, respectively.

In calm periods, such as September 2018, the transaction costs for second-lien bank loans were higher than for high-yield corporate bonds, while transaction costs for first-lien loans were typically lower than for high-yield corporate bonds. As first-lien bank loans make up the largest portion of the bank-loan market, the observed median transaction costs in September 2018 were lower for the selected bank loans than for high-yield corporate bonds. But how sensitive is the liquidity of these respective types of fixed-income assets to market distress?

We used MSCI's RiskMetrics® LiquidityMetrics to estimate the costs of forced liquidation of a holding of USD 10 million in one trading day, during both calm and distressed periods, breaking down the total transaction cost into two components: half of the bid-ask spread and the market-impact cost. Market-impact cost refers to the transaction cost incurred above the half bid-ask spread, due to the size of the trade above the typical quote size.

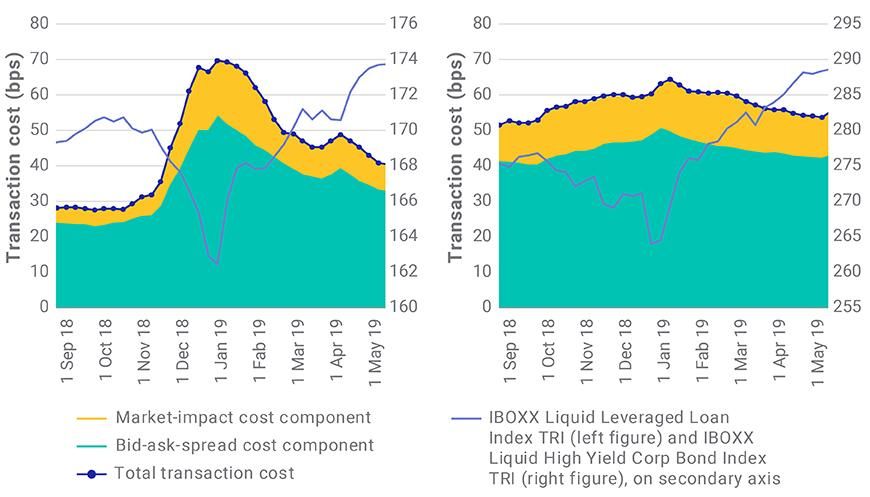

During the December 2018 high-yield sell-off, the bid-ask spread of bank loans more than doubled and their market-impact cost increased by 250%, as shown in the exhibit below. In contrast, we observed a moderate increase of 20% in both transaction-cost components for high-yield bonds. Based on the relevant index levels, the calculated transaction costs reflected market events.

Forced sale had bigger impact on bank loans than on high-yield bonds

Source: MSCI analytics based on IHS Markit data. Bid-ask spread and market impact transaction costs for forced liquidation of a holding of USD 10 million in one trading day (weekly data points, 15-day medians). B-rated first- and second-lien U.S. term loans and B-rated U.S. high-yield corporate bonds are included (not limited to constituents of presented indexes). Relevant index levels, relative to their values on Sept. 1, 2018, are shown on the secondary axis.

… and the depth shrank

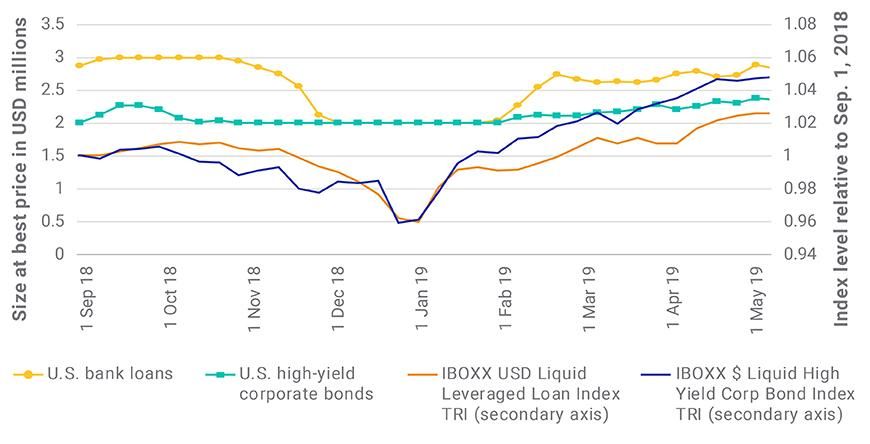

The market size at best price represents the amount that can be liquidated in one trading day at the best bid-ask spread, without incurring any market-impact cost. As a key driver of market impact, the depth at best price is an important liquidity indicator. The exhibit below shows that the depth at best price remained stable for high-yield corporate bonds during the sell-off, while shrinking by 33% for bank loans.

Market depth contracted for bank loans

Source: MSCI analytics based on IHS Markit data. Depth at best price for U.S. bank loans and high-yield corporate bonds (weekly data points, 15-day median). Relevant index levels, relative to their values on Sept. 1, 2018, are shown on the secondary axis.

Where is the price?

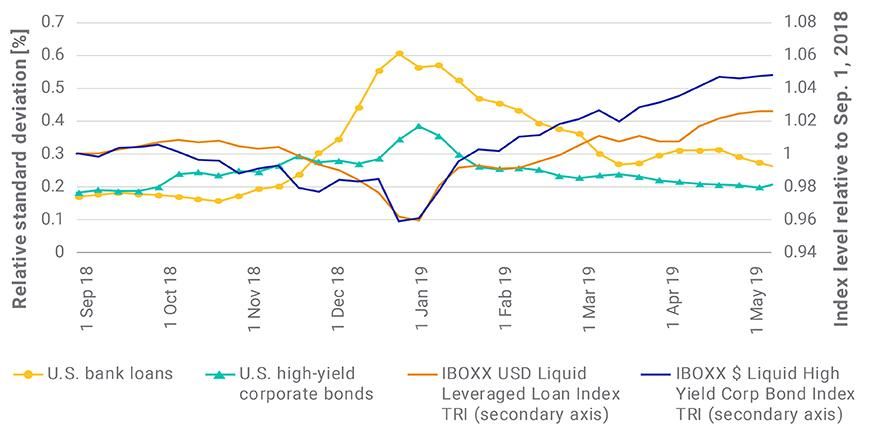

The quoted-price uncertainty may be a useful indicator that reflects market participants' confidence about the price of an asset. During periods of market distress, we would expect the uncertainty to increase. In our analysis, we define this uncertainty as the relative standard deviation of quoted bid and ask prices.

The exhibit below shows the evolution of the quoted-price uncertainty during the observed period. The uncertainty is similar for bank loans and high-yield bonds in calm market conditions, as shown in the exhibit below. However, it tripled for bank loans during the height of the sell-off, while only doubling for high-yield bonds.

Quoted-price uncertainty surged for bank loans

Source: MSCI analytics using IHS Markit data. Quoted price uncertainty for U.S. bank loans and high-yield corporate bonds, defined as the relative standard deviation of quoted prices (weekly data points, 15-day median). Relevant index levels, relative to their values on Sept. 1, 2018, are shown on the secondary axis.

Higher liquidity risk overall

So what does this mean for fixed-income investors? Bank loans' liquidity decreased dramatically during periods of market distress. This contrasts with normal market conditions, where their median transaction costs were lower and their median market size at best price was higher than those of high-yield bonds. On the other hand, high-yield corporate bonds were only moderately affected by the December 2018 high-yield sell-off. Thus, institutional investors may wish to consider leveraged loans' higher liquidity risk during market distress.

Further Reading

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.