What if the U.S.-China Trade War Escalates?

Blog post

April 13, 2018

Markets appear to have priced in the recent tariffs, but the risk of a broader trade war still looms. Market scenarios based on economic studies suggest an all-out trade war could drive global equity prices down another 10%, with U.S. investors receiving the worst of it.

After the steel and aluminum tariffs were imposed in March, retaliatory threats came from China and the U.S. And there is fear that a sequence of tit-for-tat measures between the two countries could escalate the conflict. The vast majority of economists polled1 agree on the negative impact of tariffs on the U.S. economy. Studies from the Organisation for Economic Cooperation and Development2 (OECD) and the International Monetary Fund3 (IMF) go further, concluding that there are no winners in a trade war.

Comparing U.S.-China and all-out trade war scenarios

We explored two hypothetical scenarios: a trade war contained to the U.S. and China, and an escalation in which all countries increase tariffs against each other. Under both scenarios (see exhibit below), the global economy slows down while inflation picks up in the short term, and the U.S. dollar appreciates relative to the yuan, due to decreased demand for yuan as bilateral trade4 diminishes.

Note: While we assess the impact to the overall economy here, we will analyze the potential impact on sectors in a subsequent blog post.

Trade war scenarios: Main macroeconomic assumptions

Chart assumptions derived from OECD and IMF analyses

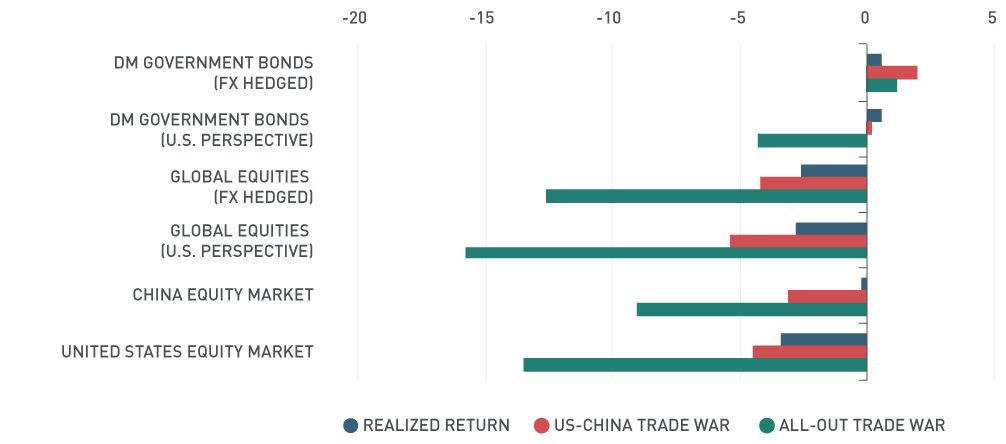

Using MSCI's stress-testing tools,5 we applied these scenarios to a global equity and a developed market government bond portfolio.6 We compared the results with the realized return between March 8, the day President Trump signed the order for steel and aluminum tariffs, and April 4, to gauge how much the markets had priced in a trade war during that period.

Our findings

Net of currency effects, global equities lose under both hypothetical scenarios, with worse losses under the all-out trade war scenario. For government bonds, there are two opposite impacts: slowing growth puts downward pressure on yields, which, for nominal yields, is partially offset by the positive inflation shock. Overall, these bonds gain under both hypothetical scenarios, but the gain is larger in the U.S.-China trade war scenario where the inflation shock is smaller. Including currency effects, the global equity and bond returns under both scenarios would be worse for U.S. investors, driven by a strengthening U.S. dollar.

Impact on asset classes, net of and including currency effects

So what does this mean?

The realized returns from March 8 through April 4 were similar to the hypothetical U.S.-China trade war scenario, which suggests that equity markets have approximately priced in this scenario. However, we find there is room for a further 10% price drop should tensions escalate to an all-out trade war.

And while the U.S.-China scenario is in good agreement, generally, with what has been realized, the Chinese equity market actually outperformed the scenario projection. This suggests that, for now, financial markets deem China to be more resilient than the modeled scenario while U.S. markets have almost completely priced in the recent tariffs.

Further reading

Stress-testing risk-parity strategies

Building predictive stress tests: MSCI's best practices

What the rise in populism may mean for your portfolio

1 Sarkar, S. "Economists United: Trump Tariffs Won't Help the Economy." Reuters, March 14, 2018.

2 Organisation for Economic Cooperation and Development. (2016). "OECD Economic Outlook". Vol. 2016, No. 2.

3 Anderson, D. et al. (2013). "Getting to Know the GIMF: The Simulation Properties of the Global Integrated Monetary and Fiscal Model." International Monetary Fund.

4 The scenario does not consider the possibility of China retaliating by selling U.S. Treasurys, which would put pressure on the U.S. bond market and on the U.S. dollar. Note that such retaliation might backfire, as it could inflict losses on China's reserves inventories.

5 MSCI Analytics include RiskManager and BarraOne. Clients will find guidance on how to implement the stress tests in RiskManager and BarraOne at our client support site (access restricted).

6 We proxy the equity portfolio with MSCI ACWI and the government bond portfolio with the ICE BofAML Global Government Index. Source: ICE BofAML Global Research, used with permission.

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.