What’s driven capital growth in real estate portfolios?

Blog post

February 6, 2020

- In real estate investing, capital growth has historically been more volatile and less predictable than income return and has therefore been responsible for most of the observed variability in total returns.

- Investors looking to monitor and evaluate their portfolio's capital growth may use a suitable benchmark to calculate relative returns, which can help identify areas of under- or outperformance.

- Decomposing relative capital growth provided additional context that helped shed light on what has driven relative performance, and how much could be attributed to variables like yield compression and income growth.

Capital growth helps tell the story of portfolio performance

Capital growth has historically been more volatile and less predictable than income return in MSCI's private real estate indexes. For that reason, there is often a demand to better understand what has driven capital growth. Using a simulated portfolio of U.K. property assets and measuring its performance against the MSCI UK Quarterly Property Index, we demonstrate how capital-growth decomposition can shed light on the drivers of portfolio performance. In this exercise, we decomposed capital growth into four components based on equivalent yield.1

The first component, active-management impact, represents how much transactions and developments contributed to capital growth. Equivalent-yield impact shows how much the change in asset values was attributable to movements in equivalent yield. Income impact represents how much of the change in asset values came from growth in initial and expected rental income. (Added together, the equivalent-yield impact and income impact show the total change in asset values.) And the investment impact, the difference between asset-value growth and capital growth, equals the amount of capital expenditure reinvested in the hypothetical portfolio.

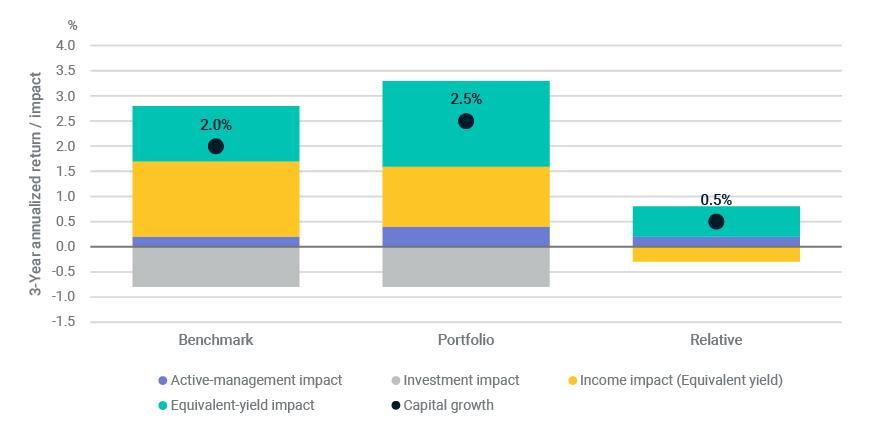

In the example below, we observe that the simulated portfolio achieved higher capital growth than the benchmark over a three-year period ended September 2019. The drivers of capital growth in the portfolio also differed from those of the benchmark. For the benchmark, the largest driver was income impact; but in the simulated portfolio, it was equivalent-yield impact that provided the largest positive contribution. Active-management impact also played a bigger role for the portfolio than it did for the benchmark.

Decomposing capital growth shows drivers of return

A simulated U.K. real estate portfolio's three-year annualized figures to September 2019. Source: MSCI Real Estate Enterprise Analytics

From these results we can infer that the hypothetical portfolio outperformed the market in terms of transaction and development activity, as well as in terms of equivalent-yield compression, but that income growth acted as a drag on relative performance. An investor reviewing these results may decide to increase their focus on income growth in the portfolio. The fact that the primary driver for the simulated portfolio was different from that of the benchmark provides a useful illustration of why it may not always make sense to try to explain the performance of a portfolio using broader market trends.

The story can differ within the portfolio

We next broke down the hypothetical portfolio and benchmark into consistent segmentations to delve even deeper into what drove relative capital growth for different parts of the portfolio. The exhibit below segments properties by sector to show how the drivers of relative capital growth varied within the simulated portfolio. As the exhibit highlights, the impacts' magnitudes and directions can vary, so it may be useful to understand these more granular trends. For example, unlike the overall portfolio, the office exposure actually outperformed in income growth, but did not benefit as much as the wider market from yield compression, suggesting that a different focus may be required for this part of the hypothetical portfolio.

Segmenting portfolios for additional insight

A simulated U.K. real estate portfolio's three-year annualized figures to September 2019. Source: MSCI Real Estate Enterprise Analytics

As the above results demonstrate, decomposing capital growth can show what has driven growth in a hypothetical portfolio, how those drivers compare to the wider market and whether there are differences within the portfolio. Given the important role that capital growth plays in real estate portfolios, capital-growth decomposition may therefore be a useful part of a performance-benchmarking process.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1As this blog post examines a simulated U.K. portfolio, our decomposition is based on equivalent yield, the most commonly used yield in the U.K. market. Capital-growth decomposition could also be performed using other yields.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.