What Yield-Curve Inversions Have Meant For Markets

Blog post

April 5, 2019

Inversion of the yield curve has historically been a reliable indicator that a recession is coming. But what has it implied for stock prices and Treasury rates? There, the answers are far from clear.

After the Federal Reserve Board lowered its growth expectations at its March 19-20 meeting, short-term yields surpassed long-term yields — a phenomenon known as a yield-curve inversion — as the market focused on prospects of lower economic growth and softer inflation.1 Historically, yield-curve inversions have signaled the likelihood of recessions occurring. In fact, all seven U.S. recessions in the last 50 years have been preceded by an inverted curve, although some commentators have questioned whether this connection will continue.2

We define and analyze yield-curve inversions based on the constant-maturity Treasury (CMT) rate, using data published on the Federal Reserve Economic Data website (FRED). By our definition, we have identified eight periods (excluding the current one) of yield-curve inversion over the past 50 years, although recessions actually followed in only seven of those periods.

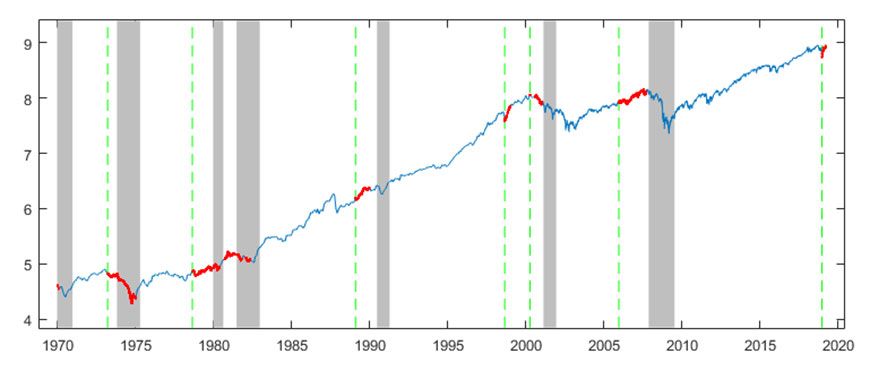

INVERTED YIELD CURVES HAVE PRECEDED SEVEN PREVIOUS RECESSIONS

Logarithmic graph of the MSCI USA Index. Red lines indicate periods of a yield-curve inversion — i.e., when the 1-year/5-year CMT spread was negative. Gray bars indicate recessions. Green vertical lines mark the initial inversions, or those that were preceded by at least six months without an inverted curve.

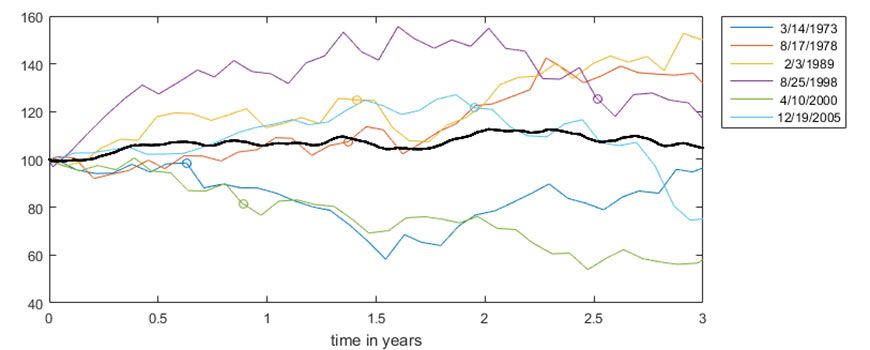

STOCKS HAVE PRESENTED NO CLEAR PATTERN AFTER YIELD-CURVE INVERSIONS

Relative level of the MSCI USA index each month after a 1-year/5-year CMT inversion, scaled so that the value at the start of the inversion is 100. The initial inversion dates are shown in the legend. The mean path is shown in black. The start of every recession is marked with a circle.

But what about stocks? In the exhibit above, we plotted the three-year path of a price after various historical inversions. The colored paths correspond to the MSCI USA Index's performance during the three years after each inversion. The circles placed along the paths mark the point at which a subsequent recession began, confirming that significant periods of time passed before recessions began. The black path is the vertical mean of all the paths.

We can make three observations based on these exhibits:

- Inversions did precede the recessions, but there was a false-positive in August 1998, when the yield-curve inversion did not lead to a recession, as can be seen in the first exhibit.

- The time between inversion and the onset of recession has been highly variable, ranging from 0.5 and 2.5 years, as is clear from the second exhibit.

- The view that an inverted curve portends negative stock-market performance is questionable, at best. For example, with four out of six inversions depicted in the second exhibit, stock prices were higher one year after the onset of inversion.

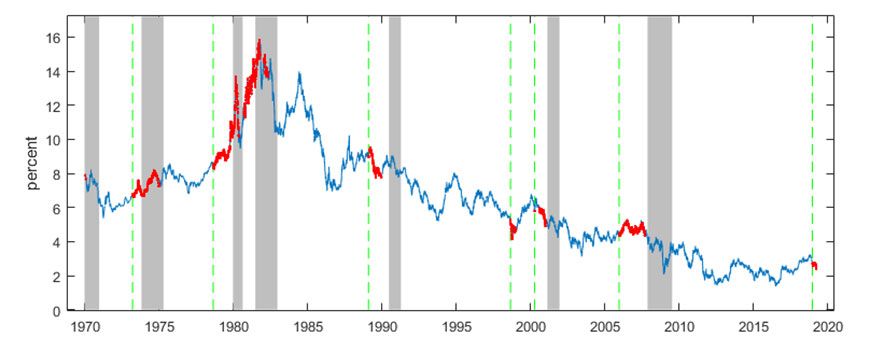

BOND YIELDS SHOW NO TENDENCY TO GO UP OR DOWN AFTER CURVE INVERSION

The 10-year CMT rate is painted in red during periods of yield-curve inversion. Gray bars indicate recessions. Green vertical lines mark the initial inversions, or those that were preceded by at least six months without an inverted curve.

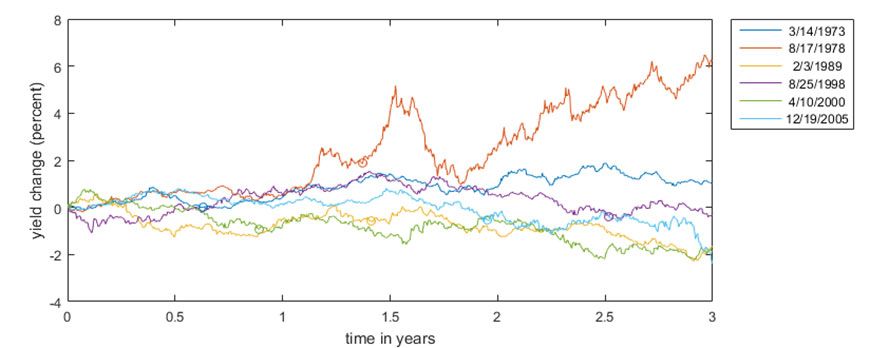

Change in the 10-year CMT after a 1-year/5-year CMT inversion. The initial inversion dates are shown in the legend. The start of every recession is marked with a circle.

Contrary to general opinions, the 10-year CMT rate has not tended to decline after a yield-curve inversion.3 This is apparent in the last exhibit.

Based on these observations and because there are only a handful of data points, we cannot claim the curve is a reliable predictor of stock prices and interest rates. After a yield-curve inversion, markets have not tended to immediately trend in one direction or the other. Asset allocators may need other signals to guide their portfolio decisions.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1In March, the 10-year yield declined by more than 30 basis points and the 1-year/5-year spread by more than 20.2Dudley, W. “Let’s Not Stress About the Next U.S. Recession.” Bloomberg Opinion, April 1, 2019.3See, for example: McWhinney, J. (2019). “The Impact of an Inverted Yield Curve.” Investopedia. The article says: “Historically, an inverted yield curve has been viewed as an indicator of a pending economic recession. When short-term interest rates exceed long-term rates, market sentiment suggests that the long-term outlook is poor and that the yields offered by long-term fixed income will continue to fall.”

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.