Where were the (factor) crowds this summer?

Blog post

August 21, 2019

- U.S. price momentum and global profitability factors, which experienced elevated crowding scores and vulnerability to negative performance at the end of 2018, suffered sizable drawdowns and had negative performance in the first half of 2019.

- We found that as of end of June, price momentum was not significantly crowded globally, but was in the U.S., which implied elevated drawdown risk to U.S. momentum strategies.

- We observed no significant crowding or uncrowding levels in other factors we looked at, including global profitability factor, though value and earnings yield continued to be moderately uncrowded, globally and in the U.S.

What happened in the first half of 2019?

We examined how crowding in factor strategies evolved over the first six months of the year using the MSCI Factor Crowding Model. We found several changes that are tied to investor behavior, including elevated levels of crowding and potentially higher drawdown risk for U.S. price momentum and lower crowding levels for global momentum and profitability. Current crowding scores suggest potentially lower risks for all global factors.

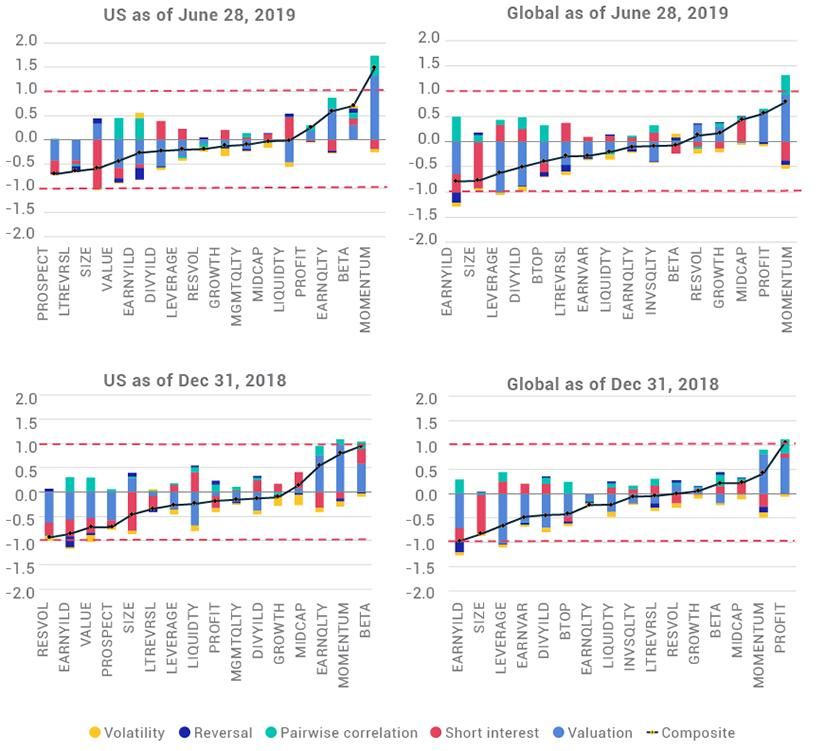

In the exhibit below, we compare style factors' crowding scores as of Dec. 31, 2018, and June 28, 2019, ordered by integrated crowding score.1 The integrated crowding score brings together five measures of factor crowding: valuation spread between top- and bottom-quintile stocks, short-interest spread between top- and bottom-quintile stocks, average return correlation of stocks in the top and bottom quintiles to corresponding quintile average portfolios, forecasted factor volatility relative to forecasted market volatility and factor reversal based on trailing factor return over the last 36 months.

As of June 2019, U.S. price momentum was crowded again (with a crowding score of 1.5), even after having moderated when markets sold off in 2018 and suffered a sizable pullback in the first four months of 2019. Meanwhile, historical beta, which was crowded at the end of last year, fell to 0.7; and residual volatility and earnings yield came off high uncrowded levels (near -1.0) at the end of last year, but were still moderately uncrowded as of the end of June.

Globally, profitability crowding subsided at the end of June to 0.55 from 1.06 at the end of December. Global price-momentum crowding increased to 0.78, but was still below last year's peak levels of about 1.0. Changes to, and current levels of, global earnings-yield crowding were similar to those in the U.S.

Snapshots from our model showed notable changes in crowding scores

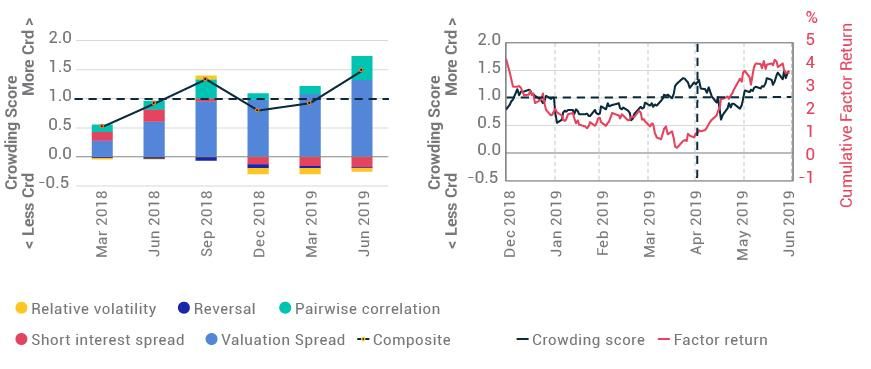

Price momentum turned defensive

It is also notable that price momentum showed defensive, rather than pro-cyclical, characteristics — i.e., was negatively correlated with market performance, due to the outperformance of defensive stocks in the second half of last year. As the exhibit below shows, the valuation-spread component of the momentum factor remained virtually unchanged over the first quarter of 2019, even as the return was negative in rising markets. The valuation spread increased in the second quarter, as the factor bounced back during the market sell-off in May, when investors rewarded defensive stocks. As we moved into June, co-movement within high- and low-momentum stocks intensified, as shown by increased average pairwise correlation. Thus, with a composite crowding score materially above 1, crowding and drawdown risk appeared elevated for U.S. price momentum at the end of June. For global momentum, however, we measured more moderate crowding for the same period.

Crowding increased for US price momentum

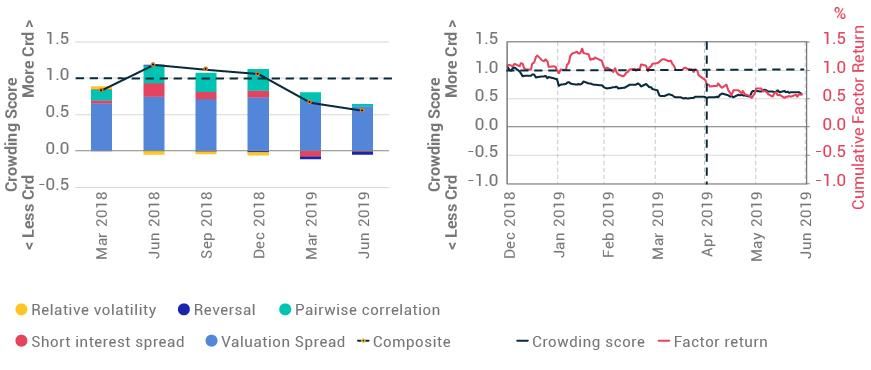

Global profitability crowding receded

Over the first half of 2019, global profitability crowding subsided from its elevated levels last year, and the factor's performance suffered a 0.50% drawdown after generating around +1% in 2018. As the exhibit below shows, the valuation spread compressed, suggesting that investors' preferences for the most versus the least profitable companies lessened even during the down market in May. Further, the short-interest-spread component turned negative during the first quarter, which suggests hedge funds reduced their exposure to profitability. However, the lower average pairwise correlation shown below may suggest investors have finished lowering their exposures to the factor.

Global profitability was less crowded through June

In short, as of the end of June, the MSCI Factor Crowding Model showed elevated levels of crowding for U.S. price momentum, but lower levels of crowding for global momentum and profitability. The model did not suggest elevated risks for other factors.

1 The scores are expressed as standardized z-scores. An integrated crowding score of 1.0 or higher indicates the level at which we have observed significantly higher drawdown risks than when the score is below 1.0. A score of -1.0 or lower indicates the factor is currently out of favor with investors. The solid black line is the combined crowding score, while the colored bars represent component contributions.

Further Reading

Factors in Focus: Dynamic short term, strategic long term

Equity markets in November — Do pro-cyclical risks remain?

Equity markets in October — Has the tide turned?

Is momentum a crowded trade that is starting to unwind?

MSCI Integrated Factor Crowding Model

Did FAANG stocks lead the US stock market drop?

MSCI Factor Investing

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.