A coronavirus stress test for global markets

Blog post

March 4, 2020

- The global spread of coronavirus is already affecting global growth. We've conducted a what-if scenario analysis that assumes a short-term drop in growth of 2 percentage points and a risk-premium increase of 2 percentage points.

- Our model indicates that, in such a scenario, there's room for further short-term losses: U.S. equities — already down 11% from Feb. 19 through March 3 — could drop a further 11%, while a hypothetical 60/40 global multi-asset-class portfolio could lose another 7%.

- From a long-horizon perspective, if a pandemic caused a shock to trend growth and the economy declined, the rebound from a market correction may be slower, and markets would feel a longer-lasting effect.

How could a pandemic impact the macroeconomy?

The global spread of COVID-19 is already affecting global growth. Disruptions in the global supply chain and decreased consumption affect companies' earnings in the short term. Combined supply and demand shocks could lead to a severe short-term decrease in GDP growth.2 It is less clear whether the coronavirus will have long-lasting effects. A sustained crisis could, for example, lead to persistent changes in global supply chains, contributing to a partial reversal of global trade and how companies conduct their businesses.

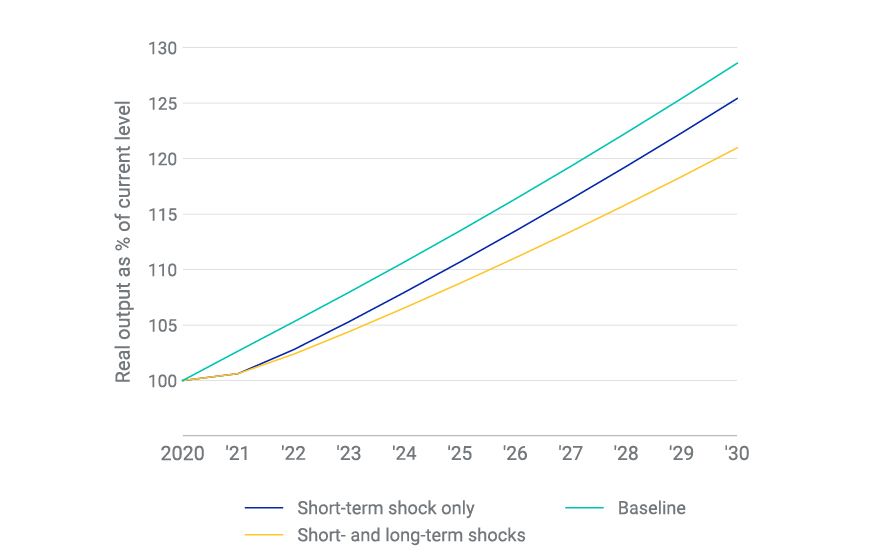

The exhibit below compares a short-term shock only (dark blue) with a combination of short- and long-term shocks (yellow). While the short-term scenario leads to only a one-time drop in output — after which we return to a normal growth regime — the long-term scenario leads to persistently lower growth. The latter could have significant implications for future equity-market performance.

From different shocks, macroeconomic outcomes may vary

The relative macroeconomic impact of the short-term growth shock (blue) and a combination of short- and long-term growth shocks (yellow), according to MSCI's macroeconomic model. Source: MSCI.

But there is a further driver for financial markets. As uncertainty increases over future growth, investors may turn more risk-averse and demand a higher premium to compensate them for the additional risk they are taking on. If they do so, they would discount future earnings more aggressively and lower companies' valuations, affecting market prices.

Implications for markets

How much room is there for further losses in the near term? In our scenario, we assume short-term growth drops by 2 percentage points and the equity risk premium increases by 2 percentage points in response to heightened uncertainty about long-term growth.3 Based on those assumptions, our model indicates the potential for a 22% drop in the U.S. equity market in the near term, relative to a baseline scenario without the growth and risk-premium shocks, according to our model.

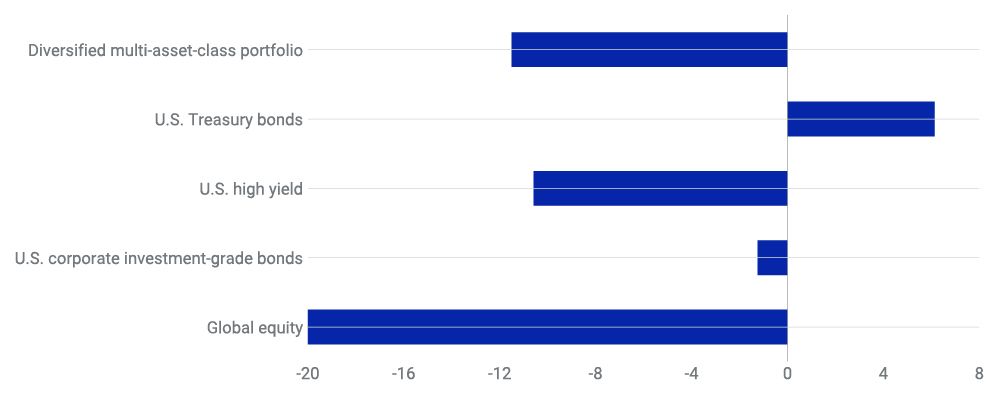

To see the potential short-term impact on a global multi-asset-class portfolio, we created a stress test using MSCI's predictive stress-testing framework to propagate our main assumptions to all other risk factors impacting portfolio returns.4 We assume that U.S. equities could drop 22% in the near term, relative to a baseline scenario. We also assume that the 10-year Treasury yield could drop by 90 basis points (bps); U.S. investment-grade credit spreads could widen by 60 bps; and high-yield credit spreads could widen by 200 bps.

Potential implications for a hypothetical 60/40 equity/bond portfolio relative to the baseline scenario

U.S. Treasurys and high-yield bonds are represented by Markit iBoxx indexes. The equity market is represented by the MSCI ACWI Index and U.S. investment-grade corporate bonds by the MSCI USD Investment Grade Corporate Bond Index. Based on Feb. 19, 2020, market data. Source: IHS Markit, MSCI.

Under this scenario, our stress test shows that a 60/40 model portfolio could lose approximately 12% and global equities could lose slightly less than 20% compared to the baseline scenario — while Treasury bonds could gain 6%, offsetting some of the equity losses. Both corporate investment-grade and high-yield bonds could suffer market-value losses as credit spreads widen, but those losses could be partially offset by the decrease in yields.5 The market has already reflected some of the changes; as of the end of trading on March 3, this hypothetical portfolio could drop 7% under our scenario.

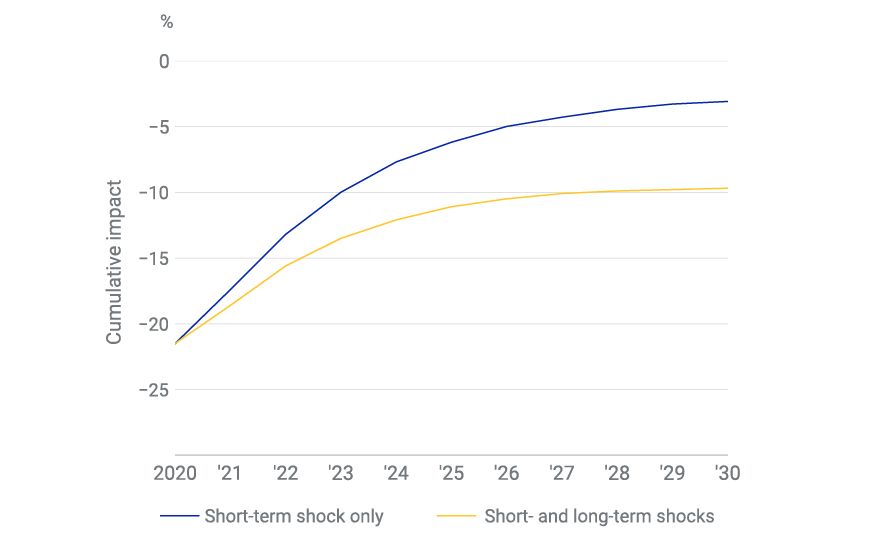

If the global economy suffers only short-term pain, the market could bounce back once the shockwave of uncertainty dissipates, according to our analysis. However, if long-term growth — and as a result, corporate earnings — took on a lower trajectory due to the pandemic, the market impact could be felt over a much longer horizon. By 2030, our model shows that the cumulative impact on U.S. equity could improve to -3% (from -22%) with only a short-term shock, but could rebound to only -10% with both short- and long-term shocks, as we can see in the exhibit below.

Macroeconomic model's projections of cumulative impact on MSCI USA Index

Equity-market impact under two macroeconomic scenarios, relative to the baseline scenario where there were no shocks to growth or risk premium. Whereas the immediate impact is mostly driven by a short-term growth shock and investors' sentiment, a long-term shock could have a longer-lasting impact. Source: MSCI.

As the coronavirus spreads across the globe, investors are assessing the potential impact on the economy and their portfolios. As we show in our stress test, there is still room to fall for both U.S. equities and a global diversified portfolio. A longer-term shock could have more severe implications.

The authors thank Rodrigo Gil for his contribution to this blog post.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1Berlinger, J. “WHO chief warns ‘we are in uncharted territory’ as number of coronavirus cases worldwide passes 90,000.” CNN, March 3, 2020.2“Interim Global Economic Outlook Assessment.” Organisation for Economic Co-operation and Development, March 2020.3We drew our assumption for the equity-risk-premium shock from a range of historical events that also stirred uncertainties in the market, as suggested by our model: The bursting of the dot-com bubble in 2002 (2%-3%), global financial crisis in 2008 (3%) and eurozone crisis in 2011 (1.5%).4The results shown in the exhibit below are generated based on this methodology, using MSCI's BarraOne®, whereby we used current correlations to propagate the shocks to a hypothetical multi-asset-class portfolio. MSCI clients can access this scenario on MSCI's client-support site. This scenario can then be used in MSCI's BarraOne® and RiskMetrics® RiskManager®.5Note that this stress test focuses on the aggregate market effect without making any explicit assumptions about sectoral divergences.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.