A More politicized Fed? The Market Yawns

Blog post

April 16, 2019

Could the Federal Reserve Board (the Fed) become less independent, with political forces exerting more influence? Some observers worry that this could become a reality, at a potential longer-term cost to the economy.1 But the market hasn't reacted with any sort of alarm, perhaps suggesting a low likelihood of a politically driven Fed anytime soon.

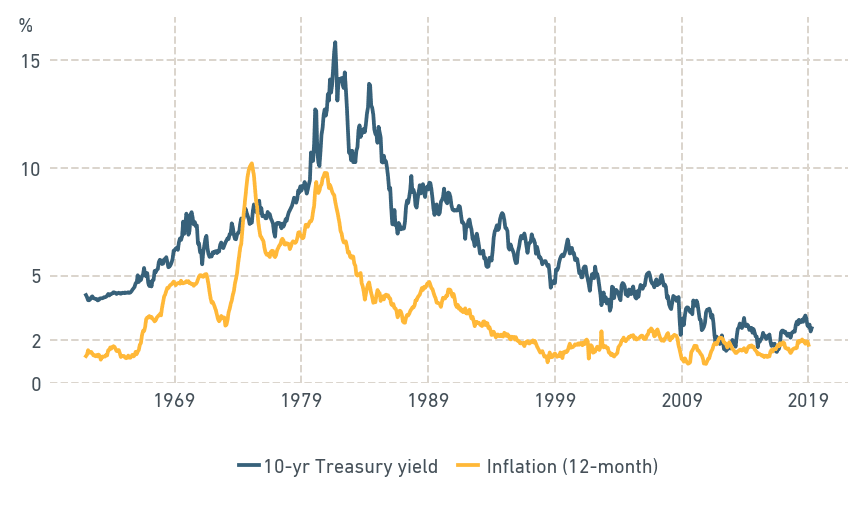

THE LONG VIEW ON US TREASURY YIELDS AND INFLATION

Our analysis of several metrics indicates that the Fed in recent years has generally delivered on key goals of low and stable inflation. An abrupt, politically motivated change of monetary policy could, of course, change this pattern — and lead to levels of inflation and volatility seen only a few times in more than a half century. But so far the pattern of stability has held.

In this post, we draw on data extending back to 1962, to put today's relatively tame inflation and rate environment in perspective. The high interest rates and inflation from the 1970s and 1980s may be a faint memory, but serve as a strong reminder of what can go wrong when monetary policy veers out of control.2

Starting in late 1979, aggressive tightening initiated during Chairman Paul Volcker's Fed tenure coincided with a dramatic decline over time in both realized inflation and bond yields, as shown in the exhibit below. The inflation rate had declined to approximately 2% by 1994. More recently, following a brief period of falling prices in the aftermath of the global financial crisis, inflation has generally been close to, but a little below, the Fed's target of 2%.

UPS AND DOWNS OF INFLATION AND YIELDS

Sources: Bureau of Economic Analysis, Personal Consumption Expenditures (PCE) price index, excluding food and energy; Federal Reserve Board, 10-Year constant-maturity Treasury (CMT) rate

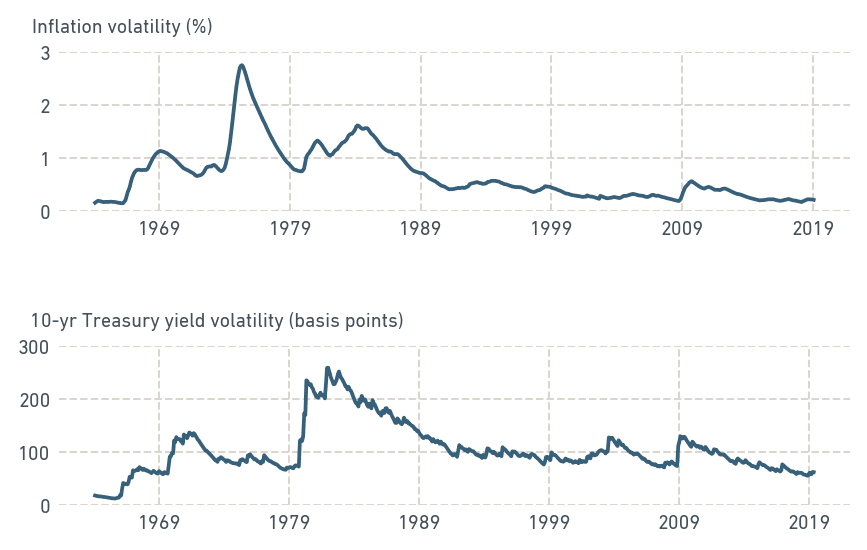

Of course, inflation levels and bond yields do not tell the whole story. Volatility of both inflation and interest rates — often attributed to uncertainty over the direction of monetary policy — can add noise in the real economy, with potentially negative economic effects. And here again it's a story of a dramatic transition to a more stable state of affairs. The exhibit below shows high inflation and rate volatilities in the 1970s and 1980s, followed by a generally declining trend. Volatilities on realized inflation and Treasury yields have been exceptionally low since 2017 and comparable to levels last seen during the 1960s.

RECENT VOLATILITY IN HISTORICAL CONTEXT

Source: MSCI calculations based on data for PCE price inflation and 10-year CMT yields. These calculations weight the historical data using exponential time decay with a half-life of one year.

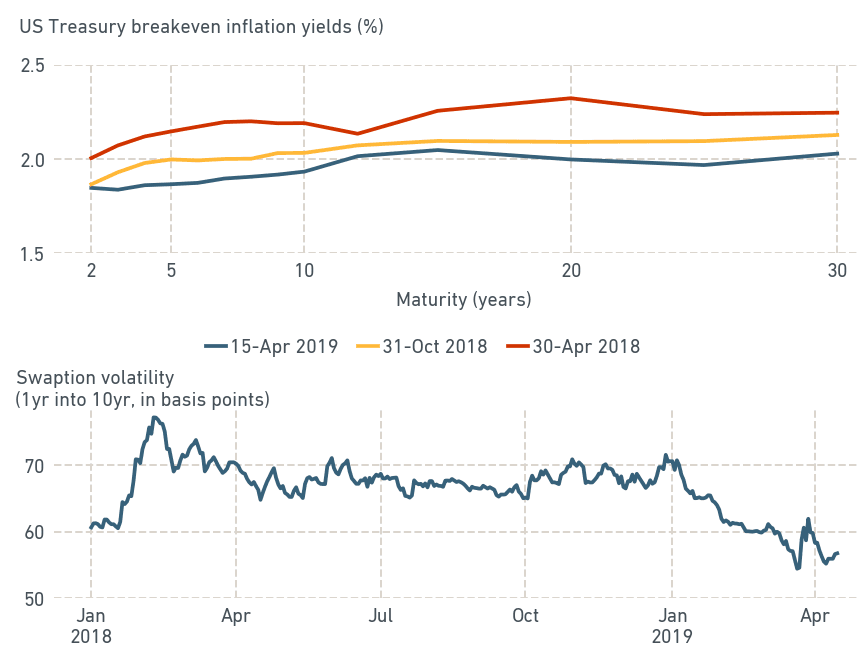

MARKET EXPECTATIONS SUGGEST ONGOING STABILITY

Our final metrics are forward-looking measures of inflation and rate volatility. As shown in the next exhibit, inflation expectations — as measured by breakeven inflation yields — have fallen over the past year and are now firmly anchored around the Fed's 2% inflation target. As of April 12, the breakeven inflation yield for 2-year-maturity U.S. Treasury bonds was 1.86%, while the breakeven yield for 30-year bonds was 2.04%. This relative flatness of the term structure of breakeven yields suggests that the market does not expect inflation to significantly rise over the longer term.

The options market is also firmly downplaying the possibility of a pick-up in rate volatility, consistent with the view of a stable monetary policy going forward. Despite the Fed's recent turnaround on its campaign of rate hikes, volatility in the swaptions market has plummeted so far this year.

TAME INFLATION EXPECTATIONS, FALLING IMPLIED RATE VOLATILITY

Source: MSCI for U.S. Treasury breakeven inflation yields and Tullett Prebon Information Inc. for swaptions data

To sum up, the market doesn't seem to be overly concerned about the chances of an abrupt change in Fed policy. The Fed's credibility with the market appears to remain strong.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1“As Fed Chief, Jerome Powell Navigates an Angry President and Turbulent Markets.” The New York Times, April 13, 2019.2For a review of historical Fed monetary decisions, see: Hetzel, R. (2017). “The Evolution of U.S. Monetary Policy.” Federal Reserve Bank of Richmond.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.