Can the Right Benchmark Improve your Vision?

Blog post

July 26, 2018

As interest in ESG investing continues to grow, so does the number of actively managed strategies that integrate environmental, social and governance considerations into their investment processes. However, institutional investors and managers have been benchmarking many of these ESG-tilted strategies against standard market-cap-weighted indexes. While these indexes provide a broad basis for evaluating performance, they lack the ability to provide the insights that might be gained from ESG-focused benchmarks. Such indexes may help improve investors' vision and understanding of managers with high ESG scores.

APPLES TO APPLES

We use the MSCI ESG Leaders Index series1 to illustrate the importance of choosing the right benchmark. Using the MSCI Peer Analytics database, we select equity mutual funds benchmarked to the MSCI World Index with assets under management (AUM) greater than USD 25 million. As of Dec. 31, 2017, this group comprised 287 funds with USD 172 billion of AUM. We then sorted these funds by their ESG scores at year-end from 2013 through 2017.2

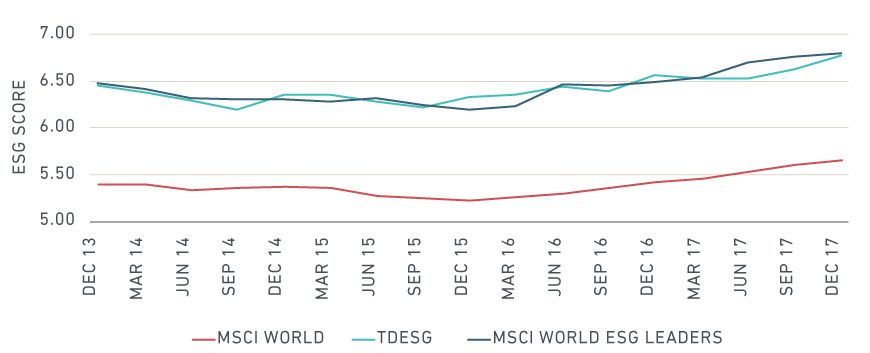

As we can see in the exhibit below, the ESG scores for the top decile managers (TDESG) tracked closely with the ESG scores for the MSCI World ESG Leaders Index from December 2013 to December 2017. This suggests they were well aligned, i.e., both the managers and the index targeted best-in-class companies with high ESG scores. Conversely, the ESG scores for the MSCI World Index were consistently lower than both managers and ESG leaders as the cap-weighted benchmark is constructed to reflect the full investable opportunity set without distinguishing the ESG profile of companies. Given the opportunity set of top-decile ESG managers were not aligned with the broad capitalization-weighted benchmark: The index may not provide the best window into understanding this group of managers.

The ESG-focused index has been more aligned with top ESG managers

Data from December 2013 to December 2017

CREATING A BETTER VIEW INTO PERFORMANCE

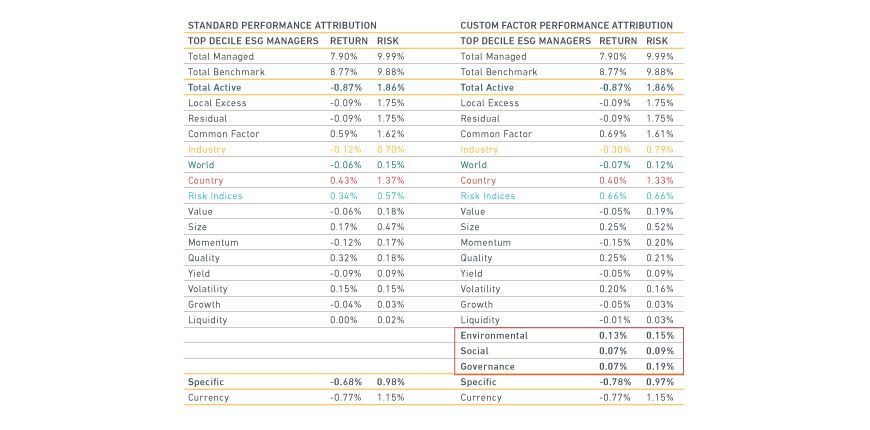

To understand how this lack of alignment can impact ESG-focused managers, we created an equal-weighted hypothetical portfolio of top-decile ESG managers based on year-end ratings from 2013 through 2017, and rebalanced it on a quarterly basis. Over the four-year period, the portfolio returned 7.90% versus the MSCI World Index's return of 8.77%. What's behind that underperformance?

Using MSCI analytical tools, we compare a standard performance attribution of this portfolio versus the MSCI World Index with a custom factor performance attribution. Our custom attribution includes ESG pillar scores3 as explanatory variables within the risk indexes.

Both attribution methods (displayed in the exhibit below) showed an annualized active return of -87 basis points (bps), indicating that these managers underperformed the benchmark. However, the custom factor model attribution showed that 27 bps of return could be attributed to environmental, social and governance pillars, stemming from industry exposures. The custom attribution also showed 10 bps more of return erosion from specific return – which represents managers' stock-picking skills – than the standard analysis; though neither attribution analysis provided evidence of superior stock-picking skills.

Performance Attribution of Top Decile ESG Managers vs. MSCI World Index

Data from December 2013 to December 2017

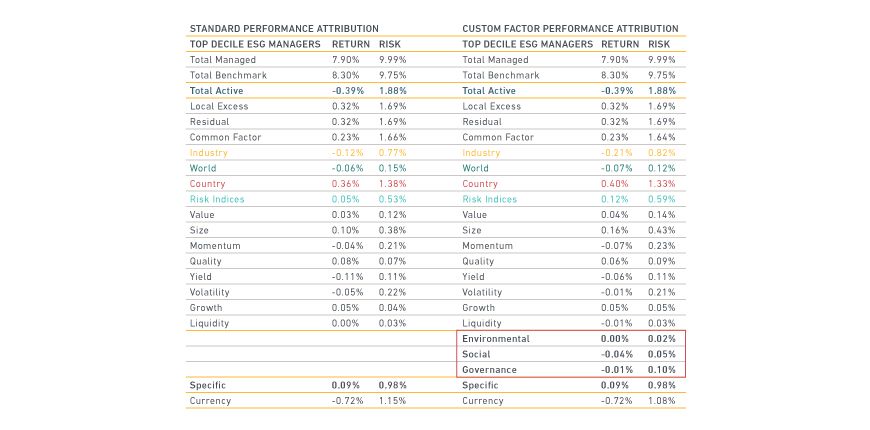

Next, we conducted the same side-by-side attribution analyses over the same period, substituting the MSCI World ESG Leaders Index as the benchmark. The return for the TDESG remained 7.90%, of course. The MSCI World ESG Leaders Index returned 8.30%.

As before, we see that both attribution methods showed a negative annualized active return (-39 bps), though relative performance of TDESG improved when compared to the ESG-focused benchmark. The custom factor model attribution now shows that -5 bps of return could be attributed to environmental, social and governance pillars, stemming from industry exposures. The lower amount of return attributable to ESG pillars also implies a better alignment between the MSCI World ESG Leaders Index and the TDESG given that they both target exposure to stocks with high ESG scores. We also see that specific return shifted from negative to positive, suggesting evidence of the TDESG managers' stock-picking skills, and illustrating how a better-aligned benchmark may help ESG-focused managers highlight their abilities.

Performance Attribution of Top Decile ESG Managers vs. MSCI World ESG Leaders Index

Data from December 2013 to

While there are good reasons why market-cap-weighted indexes remain the most widely used barometers of market performance, using ESG-oriented benchmarks and the framework outlined here, ESG-focused investors and managers may improve their vision and understanding of their portfolios.

The author thanks Raina Oberoi and Raman Aylur Subramanian for their contributions to this blog post.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1 The ESG Leaders Index series targets sector and region weights consistent with those of the underlying indexes to limit the systematic risk introduced by the ESG selection process. The methodology aims to include securities of companies with the highest ESG ratings representing 50% of the market capitalization in each sector and region of the parent index.2 ESG scores range from 0-10 and are derived from the MSCI ESG Ratings framework, which rates companies according to their exposure to industry-specific ESG risks and their ability to manage those risks relative to peers. This four-year period was selected for the availability of applicable data.3 MSCI’s ESG Ratings are comprised of individual environmental, social, and governance pillar scores.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.