Cyclicals vs. defensives: Did tariffs tip the scales?

Blog post

November 5, 2019

- While U.S. cyclical sectors mostly outperformed defensive sectors in recent years, tariffs imposed by the U.S. and China in May 2019 might have led a shift toward defensive sectors.

- We investigate how exposure to revenue from China might have affected U.S. sectors from January through September 2019.

- Analyzing stocks at the industry group level provided a more nuanced understanding of the impact tariffs may have had on cyclical and defensive stocks.

Defensive sectors showed signs of life

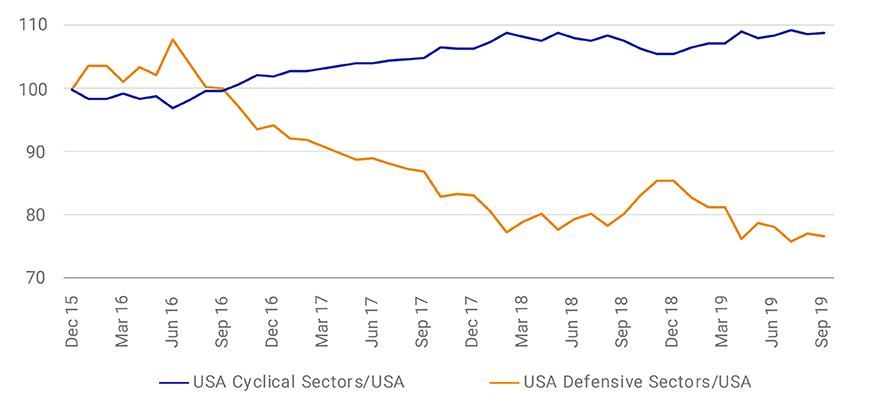

For the three years ended Sept. 30, 2019, the MSCI USA Cyclical Sectors Index outperformed the MSCI USA Index, returning 16.7% versus 13.3% on an annualized basis. Meanwhile, the MSCI USA Defensive Sectors Index returned 6.7% in the same time period. Year-to-date, cyclical stocks' more than doubled the return of defensive ones (22.2% vs. 10.4%).3

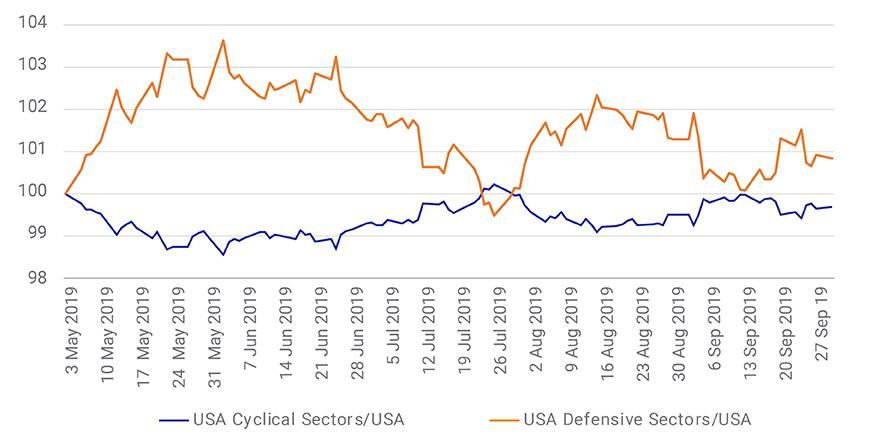

As we can see in the exhibit below, however, the Trump administration's announced trade tariffs on USD 200 billion of Chinese goods on May 5, 2019 may have been an inflection point. (A week later, the Chinese government said it would retaliate with its own tariffs on USD 60 billion of U.S. goods.)4

Cyclicals outpaced defensives over three years…

…but defensives started to rise in May

Cyclicals more exposed to China

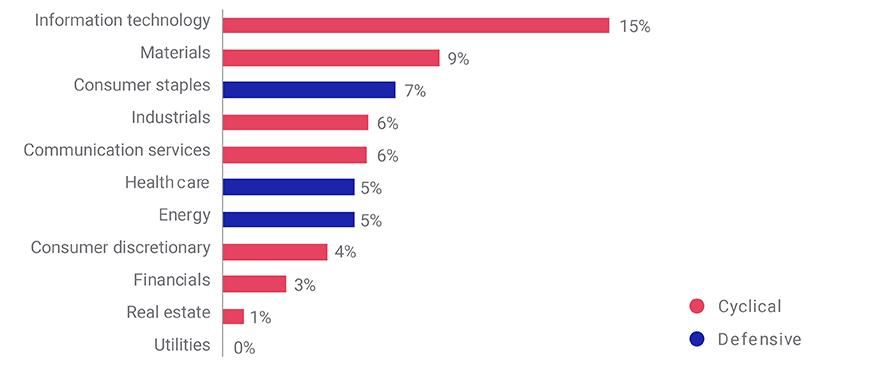

To measure the potential impact from the U.S. and Chinese tariffs, we started with how much revenue exposure each sector within the MSCI USA Index had to China as of May 5, 2019.5 Information technology had the highest exposure (15%) compared to utilities which had none. Notably, the top half of sectors with the highest revenue exposure to China were cyclical except for consumer staples. The sectors ranked in the bottom half of Chinese exposure were a mix of cyclical and defensive sectors.

Revenue exposure to China by sector

MSCI USA Index

Data for stocks in the MSCI USA Index as of May 5, 2019

Trade tariff impact at the sector level

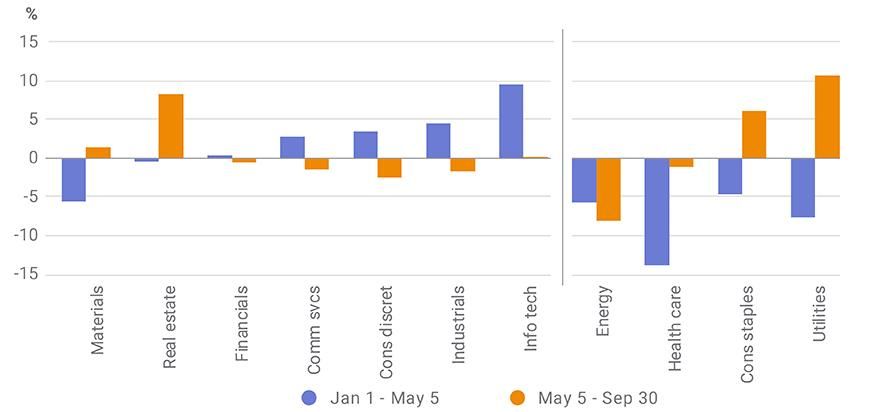

From Jan. 1 through the May 5 trade tariff announcement, five of the seven cyclical sectors (grouped on the left in the exhibit below) outperformed the MSCI USA Index. Industrials and information technology posted the greatest gains, outperforming the index by 9.6% and 4.6%, respectively. In contrast, all the defensive sectors (grouped on the right) underperformed the index.

From May 5 through Sept. 30, most of the cyclical sectors struggled while two defensive sectors, consumer staples and utilities, rebounded sharply from the first part of the year. And real estate and utilities, the two best-performing sectors during this period, had the lowest exposure to revenue from China.

Relative sector performance before and after tariffs

Trade tariff impact at the industry level

Sectors, however, explain only part of the impact of increased tariffs. Within each sector, there were industry groups that had greater exposure to the Chinese economy, and thus were harder hit by the trade tariffs.

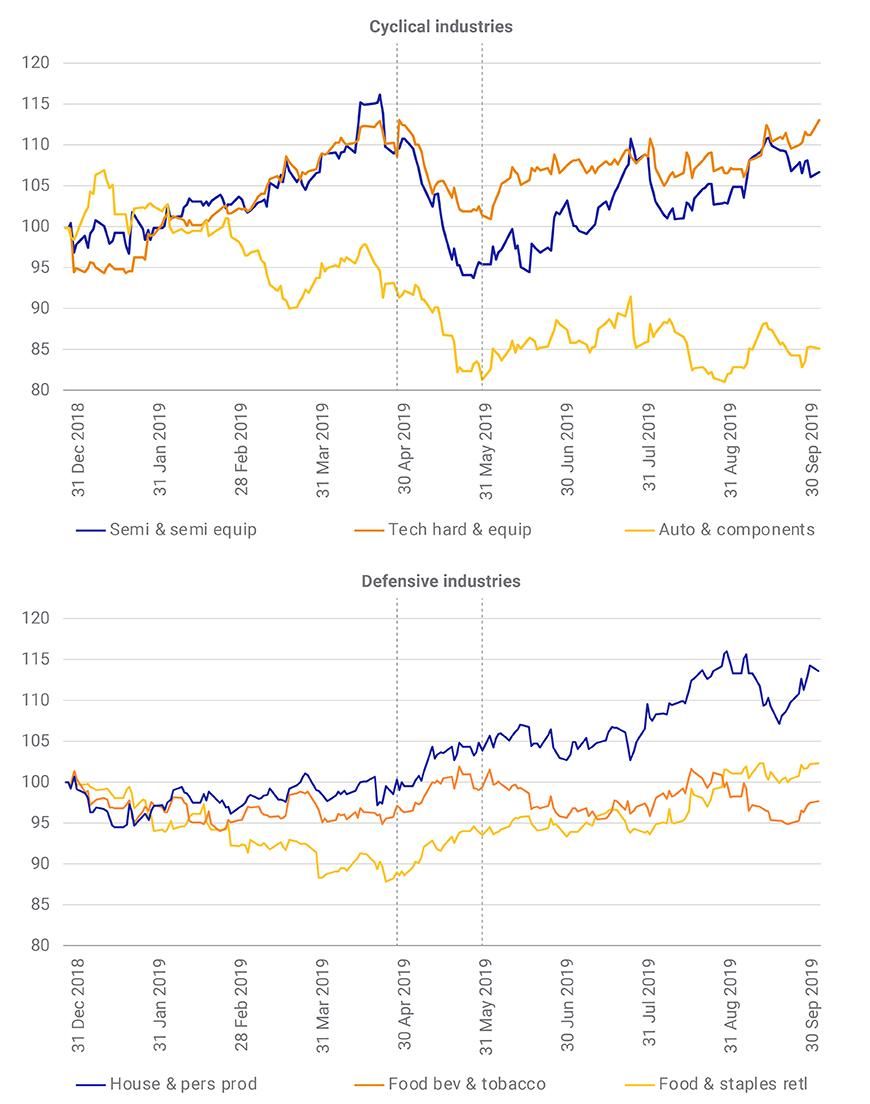

We ranked the 24 industry groups in the Global Industry Classification Standard (GICS®)6 structure by their revenue exposure to China. The top three industries fell within cyclical sectors — namely, semiconductors & semiconductor equipment, technology hardware & equipment (information technology sector), and automobiles & components (consumer discretionary sector). Between the time of the tariff announcement on May 5th and early June, all three industry groups, which included companies such as Qualcomm Inc., Apple Inc. and The Goodyear Tire & Rubber Co., experienced declines between 9% and 13%. While semiconductors & semiconductor equipment and technology hardware & equipment recovered by the end of September, automobiles & components continued to underperform.

On June 2, 2019, China released a position paper on the China-U.S. trade relations. The paper laid out China's position on the trade negotiations and stated that "cooperation is the only correct choice for China and the US and win-win is the only path to a better future."7 This paper's release coincided with the recovery in the semiconductor and tech hardware industry groups. The auto & components industry group, which was also experiencing secular events (labor disputes and sluggish sales) did not show a similar resurgence.

Returns of top cyclical and defensive industry groups by China revenue exposure

If we look at the defensive industry groups that were most exposed to China by revenue over the same period, there was no discernible impact from the trade tariff announcements through the end of May. All three industry groups: product manufacturers, which included companies such as Procter & Gamble and Colgate-Palmolive; food and beverage makers, which included companies such as Coca-Cola and General Mills Inc.; and large retailers, which included companies such as Costco Wholesale Corp. and Walmart Inc., gained between 3% and 4%.

All told, the negative impact of these trade tariffs on the cyclical industry groups appeared to be more significant during May, as highlighted in the exhibit above, whereas the impact on defensive industry groups was minimal. Investors seemed to have dismissed the impact of tariffs on the defensive industry groups.

Taking full measure

While trade tariffs may only directly target certain parts of the economy, they can trigger a ripple effect of economic uncertainty across markets. In much the same way, cyclical and defensive sectors have been good barometers for monitoring broad investor sentiment, and the shift in outperformance to defensive sectors after May's tariff announcements may be telling. However, going a level deeper into industry groups can provide a more nuanced analysis.

The author thanks Raina Oberoi for her contributions to this blog post.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1Consumer discretionary, communication services, financials, industrials, information technology, materials and real estate are classified as cyclical sectors while consumer staples, energy, health care and utilities are classified as defensive sectors.2U.S. GDP increased at an annualized rate of 2.6% from 2017-2018 but over the last four quarters ended June 2019 has contracted to 2.3%3From Jan. 1, 2019 to Sept. 30, 2019.4Wong, D. and Chipman Koty, A.. “The US-China Trade War: A Timeline.” China Briefing from Dezan Shira & Associates, Oct. 12, 2019.5Please refer to the MSCI Economic Exposure methodology document for further information6GICS, the global industry classification standard jointly developed by MSCI and Standard & Poor’s.7"Chinese position on the China-US economic and trade consultations." The State Council Information Office of the people's Republic of China. White paper, June 2019.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.