Factors in Focus: Risk sentiment and factor dynamics in a crisis

Blog post

April 2, 2020

- Fear, the realization of a global outbreak of COVID-19 and partial shutdown of many countries rattled markets over the first quarter of 2020. Global equities returned -21.3%, rebounding 15.4% from the low on March 23.

- Low volatility, momentum and quality indexes outperformed, while value and yield underperformed. Momentum indexes across regions generally performed best due to their strong outperformance in January and defensive position.

- Among credit factors in USD investment-grade corporate bonds, defensive factors such as low risk and quality outperformed.

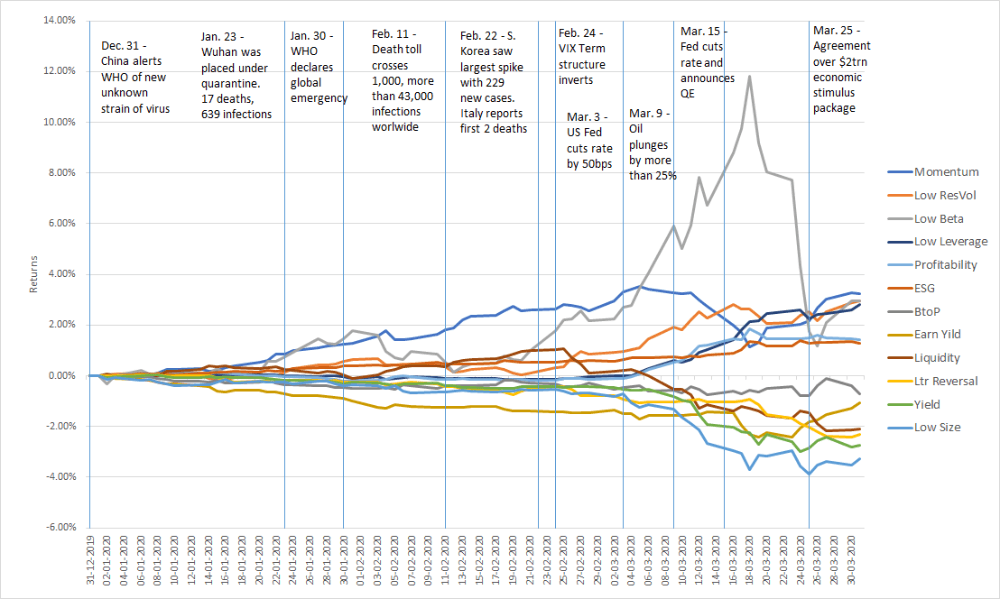

Factor performance through the crisis

The exhibit below shows the timeline of various events of the quarter, along with the performance of the top and bottom six pure factors from MSCI models.1 Stocks with positive momentum, low volatility, strong balance sheets (low leverage, high profitability) and higher ESG exposure outperformed. Low-beta reversed from March 18, 2020, following unprecedented support by both fiscal and monetary stimulus.

Q1 2020 factors as the crisis unfolded

Factor performance of top and bottom six GEM pure factors from Dec. 31, 2019, to March 31, 2020.

Global equity markets posted extremely weak performance over the first quarter of 2020, with the MSCI ACWI Index returning -21.3%, wiping out most of last year's gains. While markets were dominated by news of the contagious spread of coronavirus across the world, the crude oil supply war between Saudi Arabia and Russia erupting on March 8 triggered a major collapse in the price of oil (by approximately 60%) and added to the negative market sentiment. The Cboe Volatility Index (VIX) breached the Nov. 20, 2008, record close of 80.86, with a close of 82.69 on March 16, 2020. In the following section, we look at how factor indexes in equities and corporate bonds performed relative to their MSCI parent indexes.

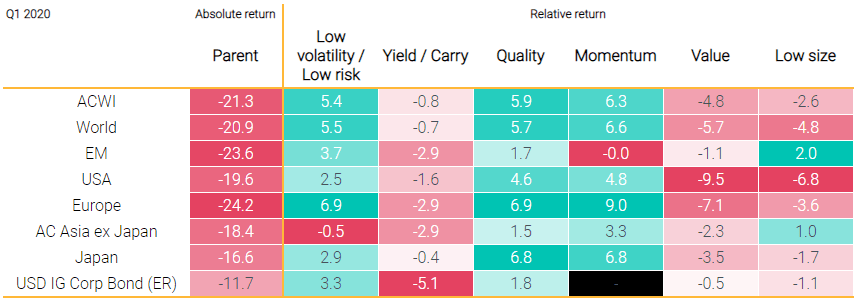

Defensive factor indexes outperformed in both equities and credit, while value underperformed

The table shows regional variations of the MSCI Minimum Volatility Index (USD), MSCI High Dividend Yield Index, MSCI Quality Index, MSCI Momentum Index, MSCI Enhanced Value Index, MSCI Equal Weighted Index, MSCI USD IG Low Risk Corporate Bond (under Low volatility), MSCI USD IG Carry Corporate Bond (under Yield), MSCI USD IG Quality Corporate Bond, MSCI USD IG Value Corporate Bond and MSCI USD IG Low Size Corporate Bond, from Dec. 31, 2019, to March 31, 2020.

Many investors took a conservative stance, on fears of an economic slowdown, as global supply-chain disruptions and pandemic gripped the market. Within equites, the quality and low-volatility indexes outperformed across all regions, supported by defensive sector exposures. By contrast, value and yield registered large underperformance in all regions. Momentum's outperformance was mostly driven by its overweight in the top-performing sectors of utilities, information technology and real estate, and an underweight in energy and financials, as well as a low-beta bias.

Low volatility, quality and momentum equity factors outperformed in all three months

The table shows active return (%) performance of the MSCI ACWI Minimum Volatility Index (USD), MSCI ACWI High Dividend Yield Index, MSCI ACWI Quality Index, MSCI ACWI Momentum Index, MSCI ACWI Enhanced Value Index and MSCI ACWI Equal Weighted Index for Q1, January, February and March 2020.

Defensive credit factors outperformed

The option-adjusted spread (OAS) of the MSCI USD IG Corporate Bond Index started the year at relatively tight levels of 107 basis points (bps) on Dec. 31, 2019, but started widening on Feb. 19, 2020, as COVID-19 spread. To counter the economic slowdown the Federal Reserve cut the interest rate by 50 bps at the start of March. However, it was not until the Fed pledged to buy government bonds in unlimited amounts, purchase investment-grade corporate bonds and provide liquidity to the market that the OAS started to ease from its peak value of 338 bps (reached on March 23) and landed at 246 bps on March 30, 2020.

The pattern among credit style factors were in line with equities. Defensive factors characterized by issuers with shorter durations and stronger balance sheets fared better — perhaps due to their ability to withstand supply and demand disruptions during the widespread lockdown. The low-risk factor outperformed by 3.28%, whereas the quality factor index outperformed by 1.77%, on an excess-returns basis. Carry, defined by bonds with relatively high OAS, experienced the largest drawdown, while the value factor, constructed to target a similar beta to the benchmark, was relatively muted.

Low-risk and quality credit factors outperformed over the first quarter

Active excess returns of the USD investment-grade corporate-bond factor indexes relative to the parent index for Q1, January, February and March 2020. Excess returns computed by subtracting the duration-matched Treasury returns from the total returns of the index over the corresponding period.

A look across sectors

Saudi Arabia and Russia started a supply war in oil that led to a price drop of 25% in a single day, one of the largest single-day corrections in history. As a result, the energy sector took a toll and contributed to a 22.5% relative drawdown with respect to the MSCI ACWI Index in Q1 2020. Financials also suffered, as fears of an economic slowdown and a longer period of lower rates impacted profitability. Technology continued its relative upward trend from last year, while utilities, communication services and real estate outperformed, reversing their trend from last year.

Technology continued to outperform energy… by 30%

Active returns of sectors vs. the MSCI ACWI Index for Q1 2020.

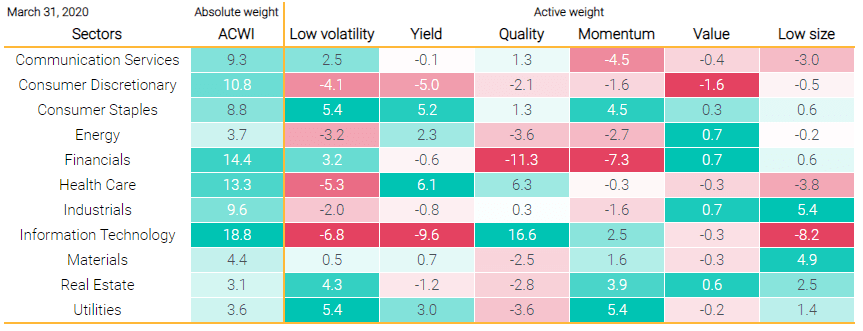

Given the significant rotation in sector performance, the table below presents the positioning of various factor indexes with respect to sectors at the end of Q1 2020. Quality had a large overweight in technology and large underweight in financials, which have been a significant driver of recent returns.

Quality had large overweight in tech and large underweight in financials

Absolute sector weights of MSCI ACWI and active sector weights of MSCI ACWI Factor Indexes, as of March 31, 2020.

The inverted VIX curve and factor dynamics

During normal market conditions, the VIX has typically formed an upward-sloping curve — i.e., the VIX three-month (3M) is typically higher than the spot VIX one-month (1M). During stressed markets, the VIX 1M has historically exceeded the VIX 3M, resulting in a curve inversion, as market participants brace for heightened near-term volatility relative to the medium term. The exhibit below plots the ratio of the spot VIX over the VIX 3M. In the recent market rout, the VIX curve inverted to the highest level since the 2008 global financial crisis and has only recently started to normalize. Despite a flattening of the curve, the overall VIX level was 53.54 at the close business on March 31, 2020.

Steepest VIX inversion since the global financial crisis

VIX 1M / VIX 3M from Jan. 1, 2008, to March 31, 2020.

What are the implications for factor performance?

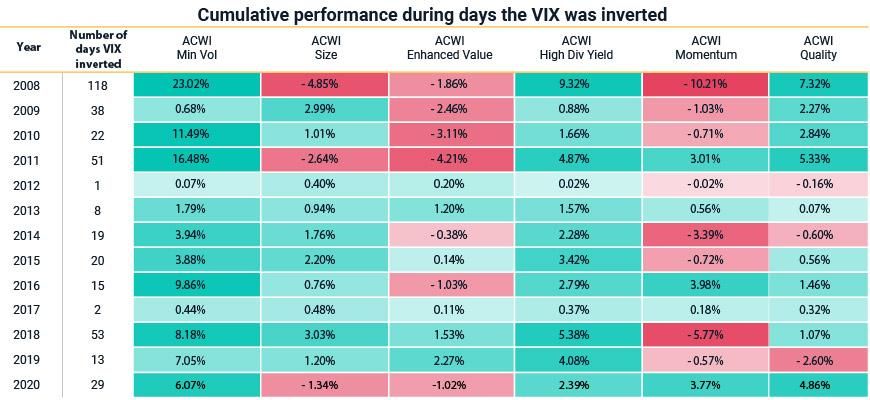

We analyzed all previous episodes of VIX inversion since 2008. During every period in which the VIX inverted, the low-volatility index outperformed the market and was often a consistent outperformer, including the most recent period in February and March 2020. Note that the VIX was inverted for 118 days in 2008, compared to 29 days in Q1 2020.

Active returns of ACWI factor indexes during the days when VIX curve was inverted from Jan. 1, 2008, to March 31, 2020.

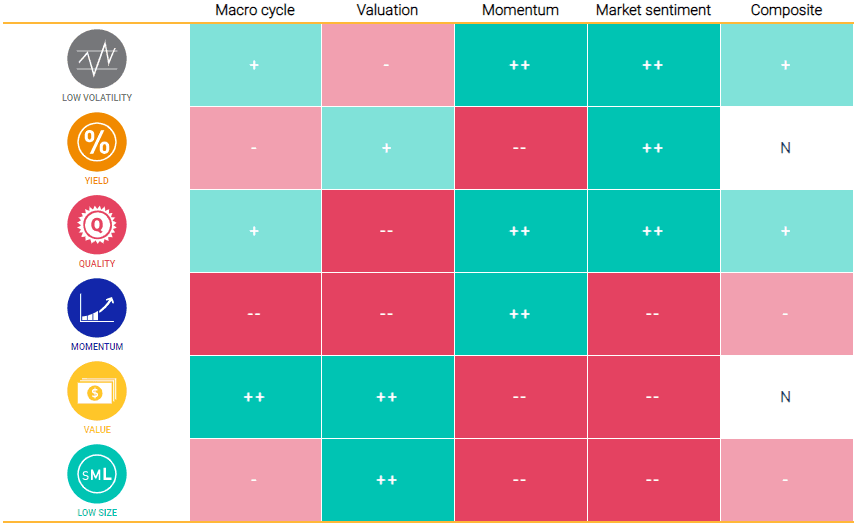

MSCI's adaptive multi-factor allocation model

Our adaptive multi-factor framework2 is a model designed to analyze decisions about tilting toward factors. Our research has shown that factors were sensitive to changing market conditions and suggests there is value in taking a holistic approach to factor assessment that encompasses the macro environment, valuations, recent performance trends and risk sentiment.

As of Mar. 31, 2020, our adaptive multi-factor model showed the following exposures across the four pillars:

- The macro cycle pillar indicated a mixed signal between contraction and recovery and overweighted value, low volatility and quality, based on the Chicago Fed National Activity Index, Federal Reserve Bank of Philadelphia's ADS Index and the PMI.

- The valuation pillar overweighted value, low size and yield, based on the valuation gap compared to an equal-weighted factor mix in the context of nearly 30 years of a factor's history.

- The momentum pillar selected momentum, quality and low volatility, based on the last three months' relative performance.

- The market sentiment pillar showed overweight to low volatility, yield and quality, based on widened credit spread and inverted VIX term structure at the time of reference.

Exposures from MSCI's adaptive multi-factor allocation model

As of March 31, 2020. Positive exposures are denoted as + or ++, negative as - or --, neutral as N.

Overall, in the context of a continued uncertain outlook and heightened market volatility, our adaptive multi-factor model showed a mild overweight to low volatility and quality and a mild underweight to momentum and low size, with yield and value being neutral relative to an equal-weighted mix.

Further Reading

Factor Index Performance scorecard

Factors in Focus: Will 2020 vision sharpen exposures?

Factors in Focus: Momentum hits a valuation speed bump

Factors in Focus: Risky start. Quality finish

Factors in Focus: Dynamic short term, strategic long term

Adaptive multi-factor allocation

A defensive approach to factor portfolios

Subscribe todayto have insights delivered to your inbox.

1We used the MSCI Global Equity Model, which included ESG factors.2Varsani, H. and Jain, V. 2018. “Adaptive multi-factor allocation.” MSCI Research Insight.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.