How Funds Are Positioned for a Low-Carbon Future

Blog post

October 25, 2017

As the world moves toward a low-carbon future, companies of many stripes are adopting renewable and clean-energy technologies. That, of course, has implications for stocks and the portfolios that hold them. How can asset owners understand the carbon-transition risks in their portfolios?

One way is to categorize funds by different types of exposure to carbon-transition risk. Using a matrix approach, asset owners may be able to better understand what long-term bets — intended or not — are embedded in their portfolios. This approach may also help investors develop more resilient investment and risk management strategies as the global energy mix evolves.

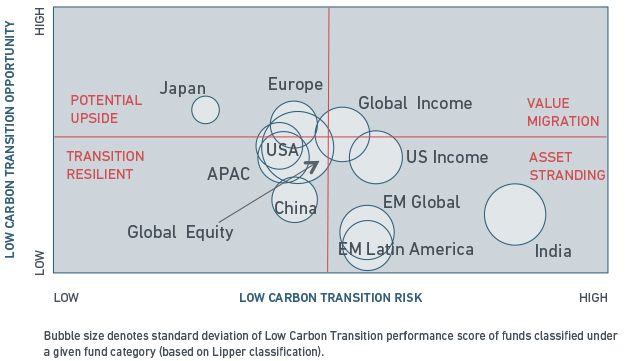

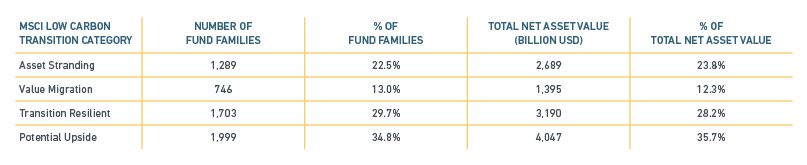

MSCI's Low Carbon Transition Matrix classifies 5,737 U.S.-domiciled equity mutual funds and exchange-traded fund families into four categories:

- Asset-stranding: investment strategies with high exposure to carbon-intensive assets probably at risk of becoming obsolete, or dependent on revenue derived from fossil-fuel activities. Dominant sectors: energy and materials.

- Value migration: funds exposed to both high risk and high opportunity during the transition to low-carbon techniques. Dominant sector: utilities, where technology is driving a migration from fossil-fueled power generation to renewable energy-based methods.

- Transition-resilient: funds that have low direct exposure to carbon-intensive sectors but might have indirect exposure, e.g., through carbon-intensive supply chains. Dominant sectors: healthcare, telecommunications, consumer staples and consumer discretionary.

- Potential upside: funds focused on sectors that appear likely to benefit from transition such as renewable energy, electric vehicles and energy-efficient equipment. Dominant sectors: information technology and industrials.

Diversified equity fund categories by their exposure to carbon transition risk

U.S.-domiciled funds, as of Sept. 6, 2017

To arrive at this framework, we used MSCI ESG Research's proprietary data sets, Carbon Metrics and Environmental Impact Metrics, to assess exposure – both to low-carbon transition risks and to opportunities. On the risk side, these tools measure fund-weighted average carbon intensity (a fund's exposure to carbon-intensive companies) and fossil-fuel revenue exposure (exposure to fossil-fuel and related businesses such as thermal coal mining). On the opportunity side, they calculate revenue exposure to low-carbon solutions such as renewable energy, energy-efficient equipment and green buildings.

Key findings

(summarized in exhibit below):

- Close to 1,300 fund families with approximately USD 2.7 trillion in net asset value (NAV) were exposed to asset-stranding risk. They represented 24% of U.S.-domiciled equity-fund NAV based on Lipper's classification.

- Some 3,702 fund families (USD 7.2 trillion in NAV) showed potential upside or appeared transition-resilient.

- Although energy and materials funds are, unsurprisingly, in the stranded-asset category, there was considerable exposure variation within each sector.

- Japanese equity funds had the highest exposure to companies providing low-carbon solutions.

Low-carbon transition matrix: fund risks and opportunities

Source: MSCI ESG Research. U.S.-domiciled funds, as of Sept. 6, 2017

This matrix can be used by:

- Asset owners to understand the intended and unintended bets embedded in their portfolios

- Fund allocators, when screening or selecting more climate-aligned funds

- Fund managers to inform their climate-risk integration strategies

Further reading:

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.