Integrating ESG in emerging markets and Asia

Blog post

March 18, 2020

- MSCI ESG Ratings were generally lower for equities in emerging markets (EM) and Asia ex-Japan than they were for developed-market (DM) equities.

- During our study period, higher-ESG-rated equities tended to perform better in EM and Asia ex-Japan regions, and ESG integration enhanced returns in those regions.

- Integrating ESG consideration could have effectively improved the performance of active EM and Asia equity portfolios and the historical return enhancement was more pronounced for Asia ex-Japan funds.

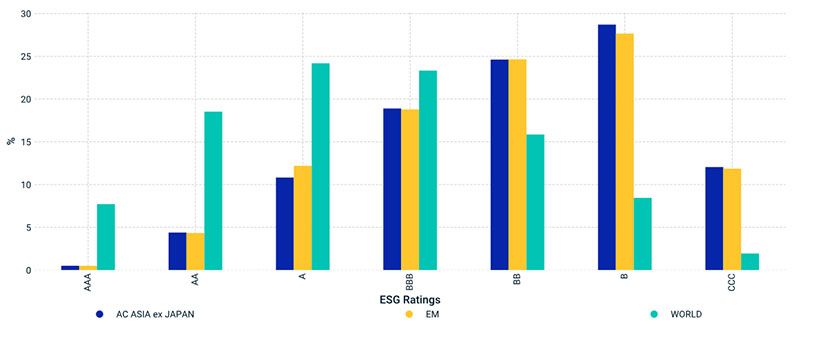

ESG ratings were not equally distributed

The exhibit below shows the dispersion of MSCI ESG Ratings as of Sept. 30, 2019. More than 80% of the constituents of the MSCI World Index received an ESG Rating between BB and AA. Conversely, more than 80% of the constituents of the MSCI Emerging Markets Index and the MSCI AC Asia ex Japan Index were rated at or below BBB.2

Wide dispersion of MSCI ESG Ratings across geographies

Data as of Sept. 30, 2019, based on the MSCI World Index, MSCI EM Index and the MSCI AC Asia ex Japan Index

This difference in ESG distribution has many implications. For example, it may mean that applying minimum ESG standards in EM and Asian equities may involve screening out more stocks than for developed-market equities.

ESG integration delivered alpha in EM and Asia

Last year, we showed that ESG integration generally demonstrated historically higher active return profiles in EM and Asian equities than in developed markets, based on the MSCI ESG Leaders Index.3 For this blog post, we analyzed a broader set of ESG strategies based on the MSCI ESG Leaders Index, MSCI ESG Universal Index and MSCI ESG Focus Index in developed, emerging and Asian-ex Japan markets.4

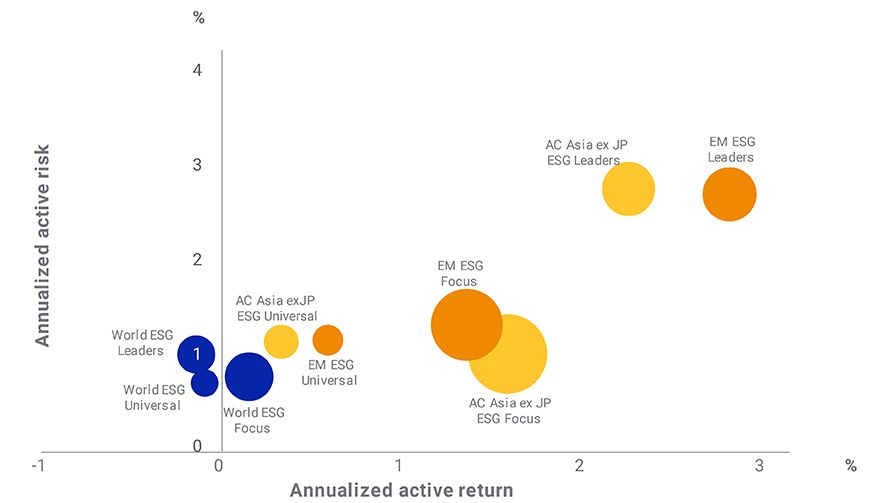

The exhibit below shows that, during our study period from December 2013 to December 2018, all three types of ESG indexes outperformed their respective cap-weighted benchmarks in EM and Asia, but delivered close to zero active returns in DMs. Compared to their cap-weighted parent indexes, the MSCI ESG Universal Indexes delivered the lowest tracking error in both DM and EM, while the MSCI ESG Focus Indexes delivered the largest ESG score enhancement.

Consistent with our previous research, the MSCI ESG Leaders Indexes — a more concentrated index with best-in-class-security selection and higher tracking error — delivered larger active returns and risks in EM and Asia than the MSCI ESG Universal and MSCI ESG Focus indexes during this study period.

MSCI ESG Indexes outperformed in EM and Asia historically

Data from Dec. 31, 2013 to Dec. 31, 2018 except for the MSCI AC Asia ex Japan ESG Universal Index which starts on May 30, 2014. The size of the bubbles corresponds to the percentage of ESG score improvement from cap-weighted parent indexes.

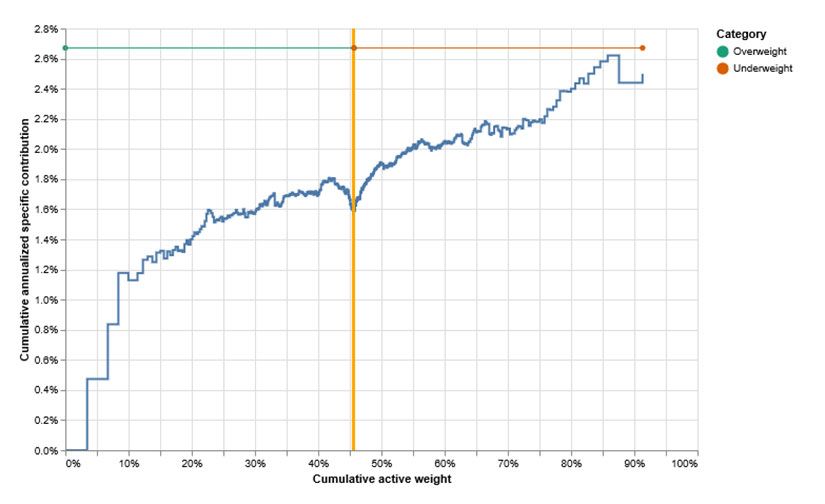

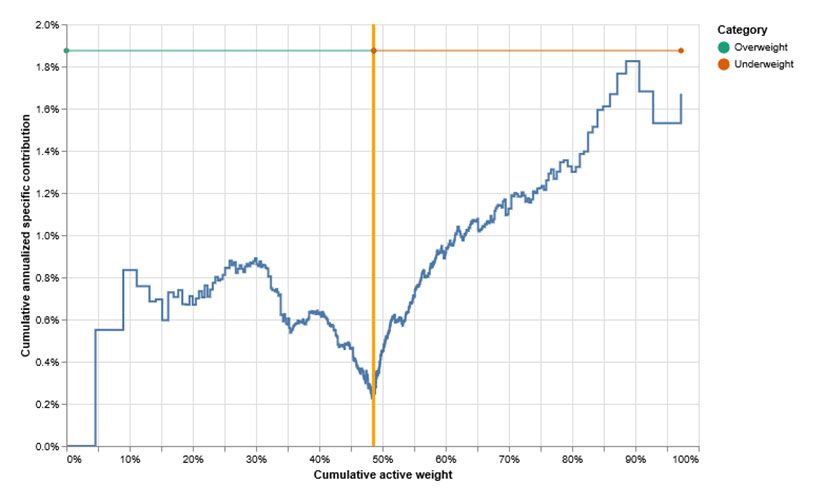

Drivers of EM and Asia ESG Leaders' outperformance

Understanding the sources of historical outperformance is important for investors evaluating the integration of ESG into EM and Asia portfolios.

We analyzed the historical performance of the MSCI EM ESG Leaders Index and the MSCI AC Asia ex Japan ESG Leaders Index from December 2013 to December 2018.5 We found that 75% and 66% of the outperformance versus market-capitalization-weighted benchmark indexes, respectively, was due to specific drivers that were not explained by traditional factors such as country, industry or style tilts.

Further, the exhibit below shows that — while the overweight of ESG leaders and underweight of ESG laggards contributed roughly 1.6% and 0.9%, respectively, to the idiosyncratic outperformance of the MSCI EM ESG Leaders Index over the period we analyzed — the main contribution to the idiosyncratic outperformance of the MSCI AC Asia ex Japan ESG Leaders Index was the underweight of ESG laggards.6

ESG drove historical outperformance in EM and Asia

Overweight of ESG leaders and underweight of laggards helps explain MSCI EM ESG Leaders Index performance

Underweight of ESG laggards helps explain MSCI AC Asia ex Japan ESG Leaders Index performance

Data from Dec. 31, 2013, to Dec. 31, 2018. The exhibit shows cumulative annualized specific contribution of the MSCI EM ESG Leaders and MSCI AC Asia ex Japan ESG Leaders Index versus cumulative overweights and underweights (index constituents are sorted from largest to smallest active weight).

Did ESG integration benefit active managers of EM equities?

A concern shared by some investors for integrating ESG into EM and Asian active portfolios is whether tilting toward higher-ESG-rated companies may reduce the total opportunity set and may lead to suboptimal performance.

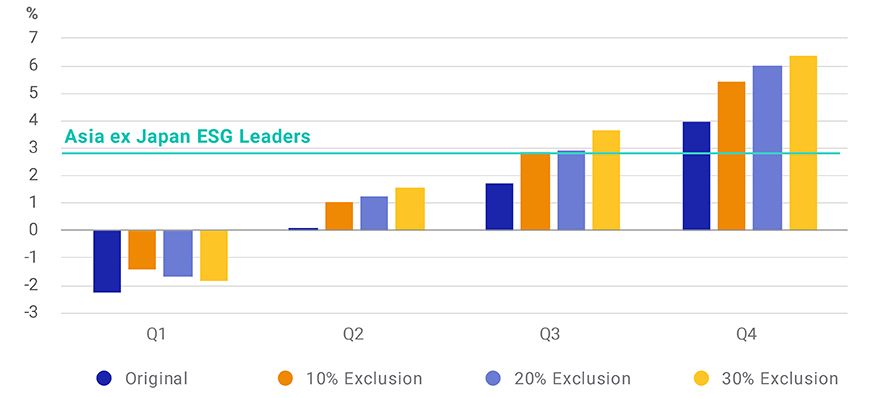

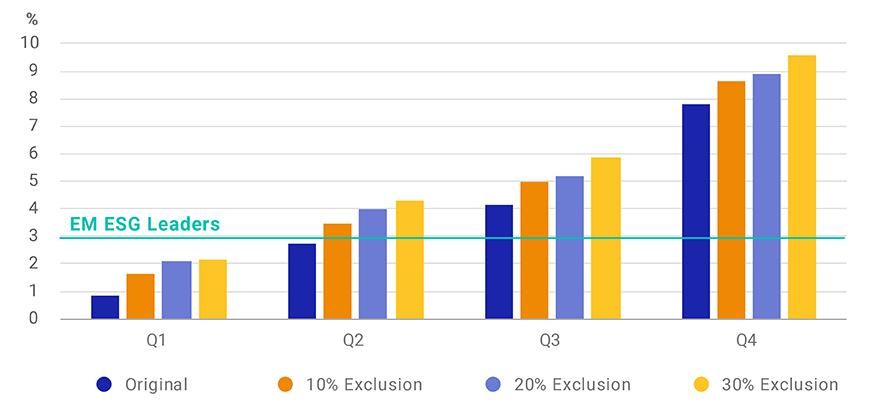

Our analysis based on 335 active EM funds and 115 active Asia-ex-Japan funds shows that simply excluding 10% of the worst ESG performers in the fund holdings enhanced performance by 73 to 82 basis points (bps) per annum for EM funds and 87 to 146 bps per annum for Asia ex-Japan funds, from December 2013 to December 2018.7

The return enhancement was more significant for better-performing Asia ex-Japan funds: 146 bps and 241 bps per annum at 10% and 30% exclusion levels, respectively, for funds in the best-performing quintile.

Integrating ESG into EM and Asian active portfolios improved returns

Integrating ESG into active EM portfolios

Integrating ESG into active Asia portfolios

Note: The exhibit above shows the annualized active performance of active EM funds versus the MSCI EM Index and active Asia ex-Japan funds versus the MSCI AC Asia ex Japan Index, during the period from December 2013 to December 2018. We grouped the funds into quartiles based on historical active performance: Q1 denotes the worst-performing group of funds, whereas Q4 denotes the best-performing group of funds. Three levels of ESG laggard exclusion were tested: 10%, 20% and 30%, where the ESG scores were neutralized for country, industry and size biases. The analysis is based on the MSCI Peer Analytics database.

In short, our findings suggest that ESG integration might have played a unique and positive role for EM and Asian equities during our study period.

The author thanks Naoya Nishimura and Shuo Xu for their contributions to this post.

1 Giese, G., Lee, L.-E., Melas, D., Nagy, Z., and Nishikawa, L. 2019. "Foundations of ESG Investing: How ESG Affects Equity Valuation, Risk and Performance." Journal of Portfolio Management

.

2 MSCI applies a consistent methodology to the ESG rating of companies across the globe. We observed lower ratings in markets where ESG is a relatively new concept and firms had less experience in managing related risks and disclosing relevant data points.

3 The MSCI ESG Leaders Indexes target companies that have the highest-ESG-rated performance in each sector of the parent index. The indexes target a 50% sector representation versus the parent index, aiming to include companies with the highest MSCI ESG Ratings in each sector.

4 See https://www.msci.comhttps://www.msci.com/esg-indexes for details on the index methodologies of different ESG strategies.

5 ESG coverage of emerging markets is inconsistent prior to 2012. We examined the MSCI Leaders Index series because of its symmetrical construction methodology, which targets the 50% top ESG-rated stocks in each GICS sector.

6 Active return performance attributions for the MSCI EM ESG Leaders Index and the MSCI AC Asia ex Japan ESG Leaders Index were based on EMM1 (MSCI's Barra Emerging Markets Equity Model) and ASE2 (MSCI's Barra Asia Pacific Equity Model) models, respectively.

7 We used a different time period from the one discussed earlier to ensure a large enough sample set for the EM Asia ex-Japan funds, while still covering a significant time horizon.

Further Reading

The PRI ESG and alpha in China report (English)

The PRI ESG and alpha in China report (Chinese)

The PRI blog 'ESG and alpha: the mainstream argument for ESG integration in China'

ESG investing in emerging markets

Understanding MSCI ESG Indexes

Foundations of ESG Investing

Weighing the Evidence: ESG and Equity Returns

Factors and ESG: the truth behind three myths

Can ESG Add Alpha?

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.