Is your real estate portfolio resilient enough?

Blog post

February 10, 2017

Amid recent worldwide political, economic and market uncertainty, how can you increase resilience of your real estate portfolio? The answer to this question boils down to prudent use of three simple portfolio construction strategies: Asset selection, sector allocation and global diversification.

The inherent heterogeneity of private real estate markets complicates the application of these strategies. Asset selection tends to be particularly important for smaller portfolios since they may consist of only a few assets and are hence dominated by asset-specific risk. Only the largest portfolios can hope to allocate in sufficient volume to provide diversified sector or market exposure.

Proper asset selection is crucial in private real estate. Every property is unique and hence, no portfolio, whatever its size, can perfectly represent the market. For this reason, 50% to 60% of the tracking error between a private real estate portfolio and its benchmark is generally attributable to asset selection. Smaller portfolios with proportionately larger exposures to individual assets are even more exposed to this phenomenon.

Variations in portfolio returns are driven by the unique characteristics of each asset, i.e., its physical attributes and location through to its lease structure and the strength of its tenants. While it is impossible to perfectly diversify away asset-specific risk, the resilience of portfolios can be enhanced by combining real estate assets with varying characteristics and by actively managing the physical and cash flow characteristics of the assets themselves.

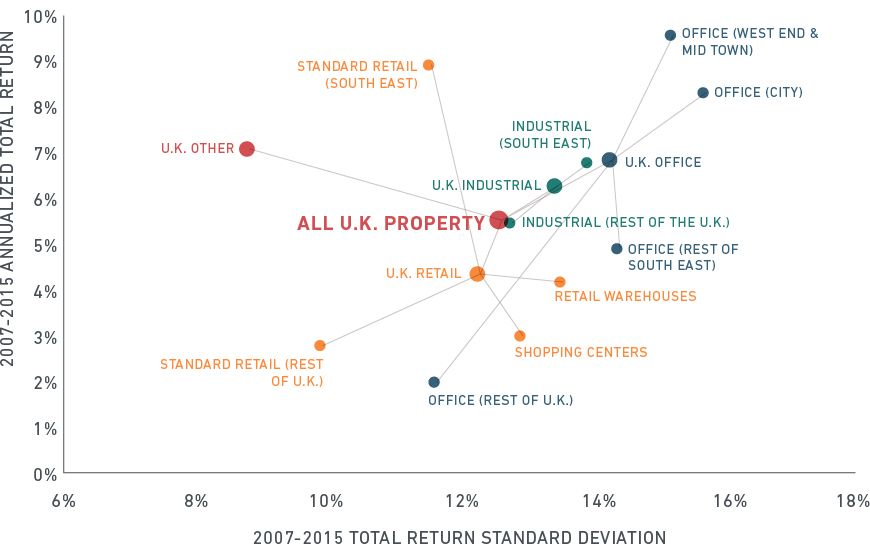

Sector allocation offers another opportunity to build portfolio resilience. By allocating capital to the right sectors, it is possible to strengthen the defensive nature of the portfolio. For example, the annualized return of U.K. office assets topped those of U.K. retail assets by 250 basis points during the 2007-2015 period. Looking at the sub-sector level, performance varied even more over the same period, as can be seen below.

Returns of UK private real estate assets varied greatly by sector and sub-sector

Source: MSCI — Global Intel

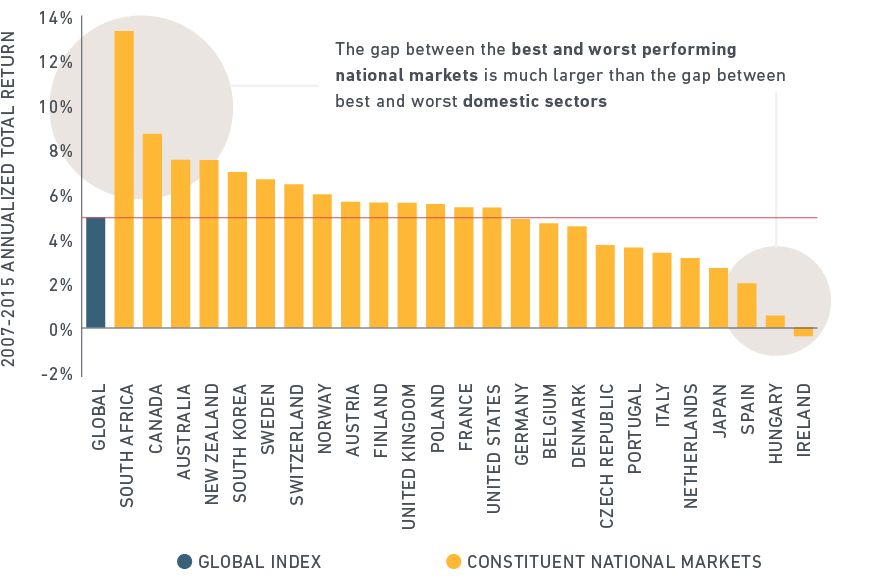

Finally, global diversification has historically offered even more resilience benefits than sector allocation up front. Internationally, there has been a wide range of performance, with over 13 percentage points of difference in the annualized total return of the best- and worst-performing markets in the eight-year period from 2007, as can be seen below. This large gulf in performance highlights both the potential of global diversification and the importance of managing it properly.

Mind the gap: Return differences between best and worst national markets

Most private real estate portfolios are too small to take advantage of these global diversification benefits and thus exhibit a strong home bias. Consequently, cross-border correlations remain low. Funds that are big enough to exploit these low correlations can produce greater portfolio resilience.

The basic strategies of asset selection, sector allocation and global diversification can be borrowed from publicly listed asset classes. However, they must be applied carefully, given the unique characteristics of the private real estate market. Private real estate market data built from the bottom up with detailed asset-level cash flows can help investors optimize the mix of these strategies in a way that is suitable for their portfolios.

The author thanks Bryan Reid and Will Robson for their contributions to this post.

Further reading:

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.