Factors and ESG: The Truth Behind Three Myths

Blog post

March 20, 2019

Understanding the true relationship between factors and environmental, social and governance-related (ESG) issues is relevant for fundamental and quantitative managers as they consider ESG criteria as part of their investment process. Yet misperceptions persist. We explored three common myths and observed that, contrary to popular belief, quality was not the same as ESG, momentum and ESG were compatible and some smaller-cap stocks had superior ESG characteristics.1

Myth #1: ESG is just another way of saying quality

We have previously seen positive correlations between quality style factors and ESG scores.2 We have also found that ESG scores could have been improved without a meaningful reduction in exposure to the quality factor. But that does not mean they are the same thing.

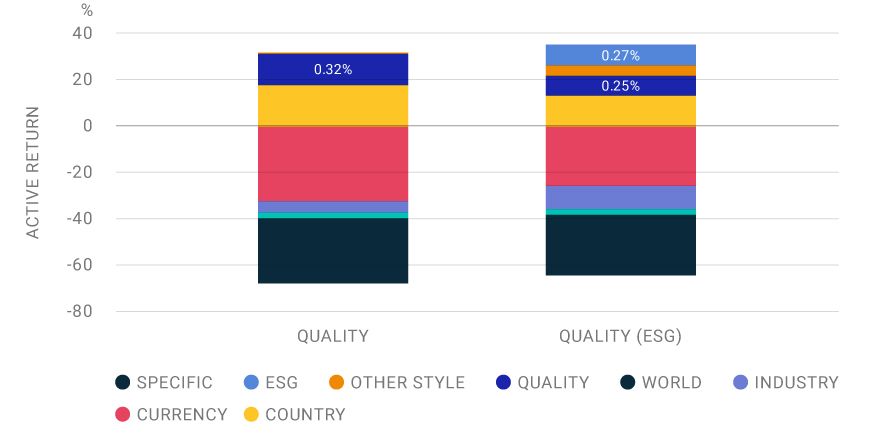

Quality contribution remained relatively stable when ESG was included in the risk model

We decomposed the active return for the top-decile ESG manager portfolios (TDESG) over the period from Dec. 31, 2013 to Dec. 31, 2017 using the Barra Global Total Market Equity Model for Long-term Investors (GEMLT), excluding and including ESG criteria.3

When excluding ESG in the risk model (column labeled "Quality" in the exhibit above), we found the quality factor contributed 32 basis points (bps) to the active return during the period. When we included ESG (column labeled "Quality (ESG)" in the exhibit), we saw an ESG return contribution of 27 bps, and the quality return contribution decreased by only 7 bps (from 32 to 25). While the return contribution from industry, specific and other style factors showed more meaningful shifts, the fact that the return from quality remained relatively stable suggests it is distinct from ESG.

Myth #2: Momentum and ESG are incompatible

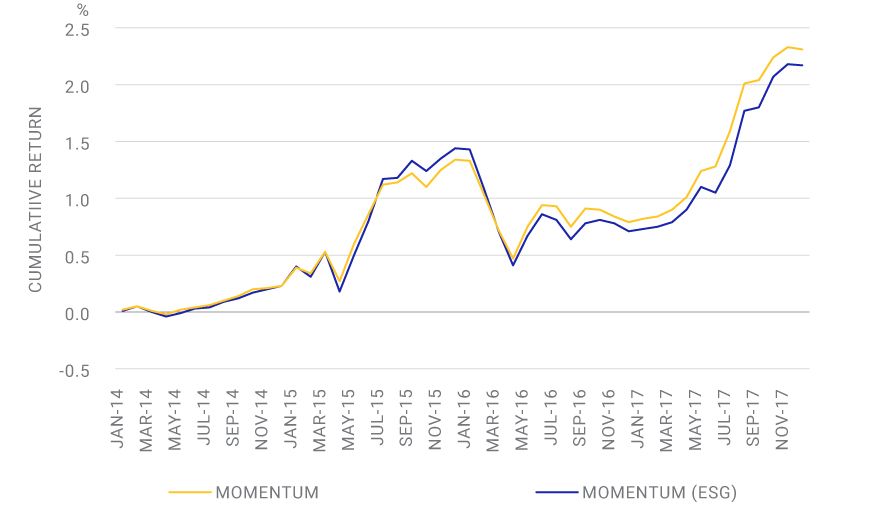

While the momentum factor has appeared to have very low correlation to ESG,4 we observed return from momentum within a subset of the TDESG portfolios.

We compared the cumulative return for this subset from Dec. 31, 2013 to Dec. 31, 2017 using risk models with and without ESG.5 As we see in the exhibit below, the cumulative return for the momentum factor using the standard global equity model was 2.3% compared to 2.2% using the same model and including ESG. In other words, introducing ESG as an explanatory risk factor did not meaningfully impact the return from momentum — meaning momentum and ESG appear to have been compatible after all.

Including ESG in the risk model did not meaningfully impact momentum-factor returns

Myth #3: Small-cap stocks have low ESG ratings

This myth stems from the early years of ESG research when larger companies were better able to disclose ESG-related data compared to smaller ones. However, our research shows that starting in 2009, the company-size reporting bias was mitigated due to more disclosures by mid-cap companies, as well as enhancements made to the MSCI ESG Ratings model.6

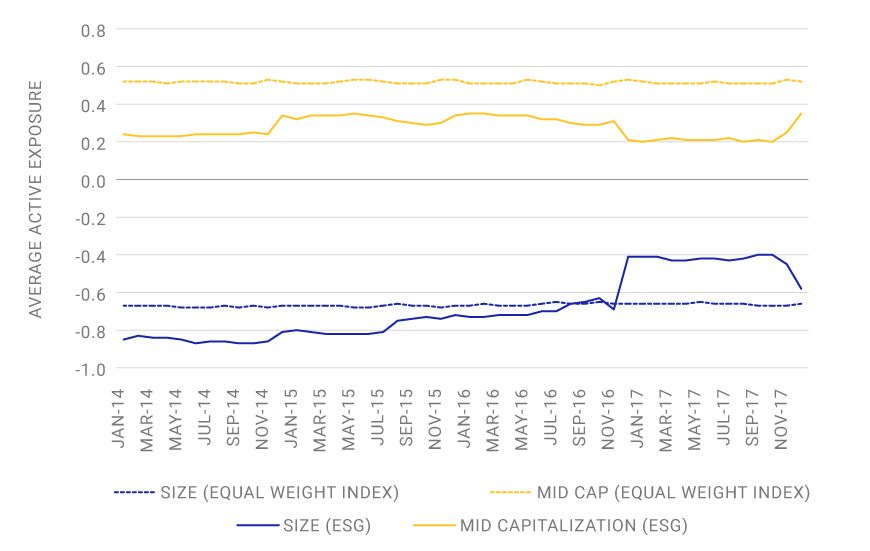

Portfolios with high ESG scores maintained persistent exposure to low-size factor

We looked at the mid-cap and low-size factors7 and found the TDESG portfolios maintained meaningful exposure to both. As a proxy for low-size exposure, we use the MSCI World Equal Weighted Index (the dotted lines in the exhibit above) In comparison, the solid lines show the average active exposure for a subset of the TDESG portfolios. Over the period from Dec. 31, 2013 to Dec. 31, 2017, the TDESG portfolios had virtually identical average active exposure to size compared to the MSCI World Equal Weighted Index (-.68 versus -.67) and an average active mid-cap exposure of .24 versus .52. Persistent exposure to the low-size factor along with a high ESG score provides evidence that the low-size factor could have been targeted within an ESG-oriented portfolio.

Myths are powerful. And they have a way of outliving the evidence that disproves them. However, given the importance of factor investing within managers' investment processes and the impact ESG criteria can play over the long term, there may be value in challenging preconceived notions when making decisions.

The author thanks Raman Aylur Subramanian and Raina Oberoi for contributing to this blog.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1 This blog builds on previous research published in “Can the right benchmark improve your vision?” That blog post analyzed the performance of top-decile ESG managers benchmarked to the MSCI World Index from December 2013 through December 2017.2 Kulkarni, P., M. Alighanbari and S. Doole. (2017). “The MSCI Factor ESG Target Indexes.” MSCI Research Insight.3 This portfolio had an average ESG score from December 2013 to December 2017 of 6.43.4 Kulkarni et al. (2017).5 This portfolio had an average ESG score from December 2013 to December 2017 of 6.50.6 Nagy, Z., A. Kassam and L.-E. Lee. (2015). “Can ESG Add Alpha?” MSCI Research Insight.7 Please refer to the MSCI FaCS Methodology for additional details.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.