Has ESG Affected Stock Performance?

Blog post

November 29, 2017

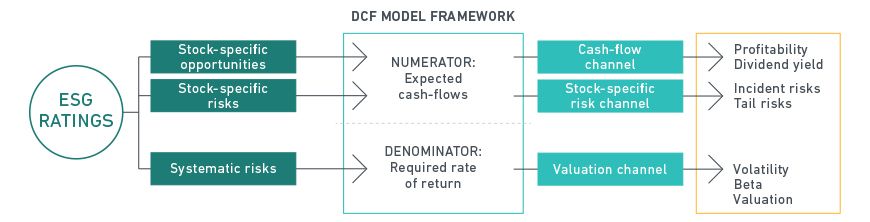

Are ESG characteristics tied to stock performance? Many researchers have studied the relationship between companies with strong environmental, social and governance (ESG) characteristics and corporate financial performance. A major challenge has been to show that positive correlations — when produced — explain the behavior. As the classic phrase used by statisticians says, "correlation does not imply causation." Instead of conducting a pure correlation-based analysis, we focused on understanding how ESG characteristics have led to financially significant effects. This way, we avoided the risk of data-mining and we can differentiate between correlation and causality. We examined how ESG information embedded within stocks is transmitted to the equity market. Borrowing the language of central banks, we created three "transmission channels" within a standard discounted cash flow (DCF) model. We call these the cash-flow channel, the idiosyncratic risk channel and the valuation channel. The former two channels are transmitted through corporations' idiosyncratic risk profiles, whereas the latter transmission channel is linked to companies' systematic risk profiles.

Fundamental transmission channels from ESG to financial values through a DCF model

These channels are based on the following rationales:

- Cash-flow channel: High ESG-rated companies are more competitive and can generate abnormal returns, leading to higher profitability and dividend payments.

- Idiosyncratic risk channel: High ESG-rated companies are better at managing company-specific business and operational risks and therefore have a lower probability of suffering incidents that can impact their share price. Consequently, their stock prices display lower idiosyncratic tail risks.

- Valuation channel: High ESG-rated companies tend to have lower exposure to systematic risk factors. Therefore, their expected cost of capital is lower, leading to higher valuations in a DCF model framework.

ESG and risk management

In our analysis we have looked at both stock-specific risks, which are linked to companies' specific business model and risk management processes, as well as systematic risks, which are macroeconomic in nature and are linked to companies' exposure to changes in the market environment, market prices or changes in regulation.

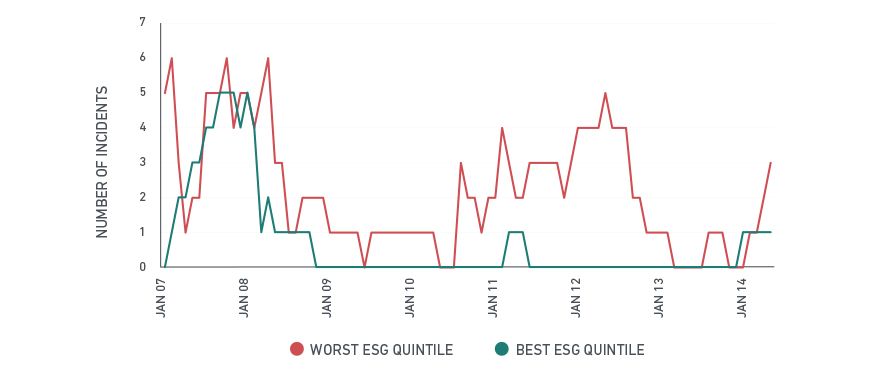

We found that MSCI ESG Ratings provided valuable information for both systematic risks and stock-specific risks. For example, we saw that companies in the bottom fifth of the MSCI World Index experienced large drawdowns (above 95%) three times higher than those in the top fifth, as can be seen in the exhibit below, supporting the assertion that ESG has provided insight into incident risks throughout the 10-year period we studied.

Bottom 20% of ESG stocks experienced large drawdowns three times more than top 20% stocks

MSCI World Index, January 2007 to May 2017. Note: We use a full three-year look-ahead window in reporting results. For each month, we report the number of stocks that realized a more than 95% cumulative loss over the next three years, taking the price at month end as the reference point for the return calculation. Thus, the last data point is from May 2014.

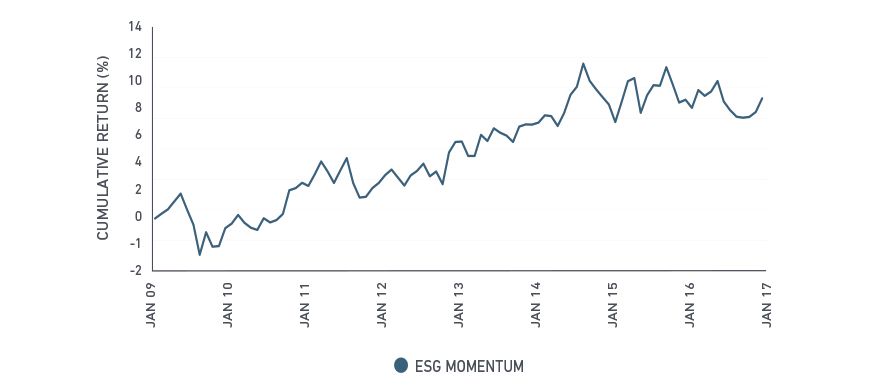

ESG momentum

We then examined to what extent a change in a company's ESG characteristics has been a leading indicator for changes in systematic and idiosyncratic risk, which we call "ESG momentum." We found that ESG rating changes had a time lag of up to three years into changes in our three transmission channels as well as in valuation variables.

This analysis not only provides support that strong ESG characteristics have led to positive stock performance (showing causality), but that ESG momentum may be a useful financial indicator in its own right and investors may choose to use this signal in addition to ESG ratings in portfolio construction methodologies. For instance, while not indicative of future performance, the top ESG momentum quintile consistently outperformed the bottom ESG momentum quintile during our study period, as we see in the following exhibit.

Top ESG momentum quintiles outperformed bottom ESG Momentum quintile

Our research indicated that ESG has affected the valuation and performance of companies both through their systematic risk profile (lower costs of capital and higher valuations) and their idiosyncratic risk profile (higher profitability and lower exposures to tail risk). Thus, the transmission from ESG characteristics to financial value was a multi-channel process, as opposed to factor investing where the transmission mechanism is typically simpler and one dimensional.

In addition, ESG ratings have experienced a longer life than some factors, potentially making them suitable for inclusion in the asset allocation process and policy benchmarks. Classical factors such as momentum typically have persisted for a few months only. In contrast, the impact of ESG ratings on systematic and idiosyncratic risks lasted for several years during the study period.

The author thanks Linda-Eling Lee, Dimitris Melas, Zoltan Nagy and Laura Nishikawa for their contributions to this post.

Further reading:

Foundations of ESG Investing - Part 1: How ESG Affects Equity Valuation, Risk and Performance

Did ESG Ratings help to explain changes in sovereign CDS spreads?

Integrating ESG criteria into factor index construction

Investing for the long run: ESG and performance drivers

Keep it broad: An approach to ESG strategic tilting

MSCI ESG Ratings

MSCI Factor ESG Target Indexes

Integrating ESG info factor portfolios

Can ESG add alpha?

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.