How Can Active Managers Put ESG to Work?

Blog post

May 15, 2018

Our research shows how favorable ESG characteristics have historically had a positive impact on equity valuation, risk and performance.1 But many active managers may have concerns that using ESG data could disrupt their investment process and introduce unintended biases to the portfolio.

We examined two approaches to integrating ESG data and ratings in stock selection and portfolio construction that preserved the portfolio's fundamental characteristics. We tested how these approaches impacted the risk and return of a sample of over 1,000 international equity mutual funds. For these active portfolios, they reduced risk by up to 15 basis points (bps) per year and improved return by up to 30 bps per year from December 2008 to November 2017.

INTEGRATING ESG INFORMATION IN AN ACTIVE STRATEGY

Typically, the first step in the fundamental investment process is security selection. In this step, the manager uses traditional financial analysis to select securities for the portfolio. ESG data and ratings may complement financial analysis by distinguishing between best-in-class ESG companies and those with below average ESG policies. This information can be combined with measures of corporate financial performance to identify companies that may warrant additional investigation or removal from the portfolio.

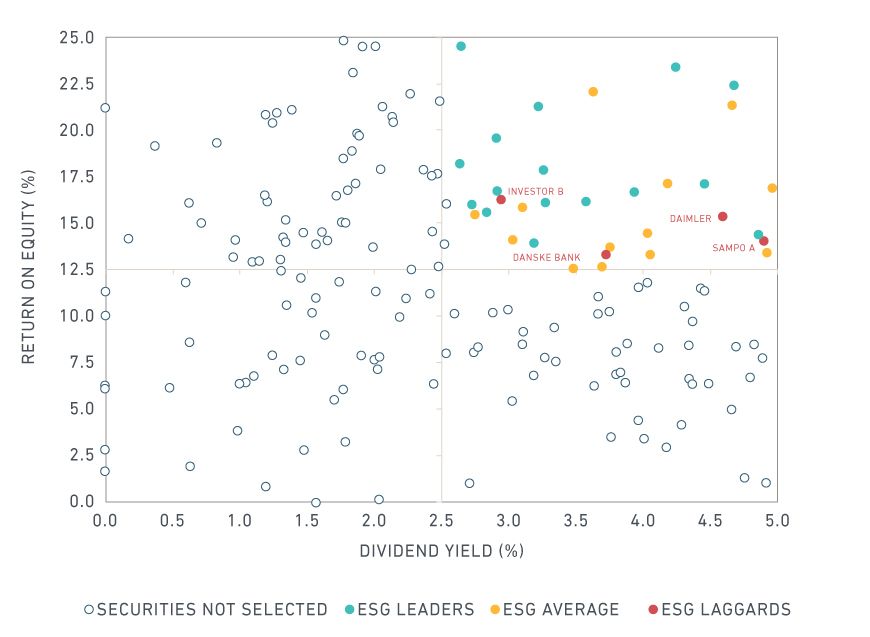

The first exhibit shows securities selected by a hypothetical active fund manager who manages a European "growth and income" equity fund. In this example, the manager has selected 54 securities, out of a total of 446 MSCI Europe Index constituents as of Dec. 31, 2017. The selected securities met the fund's investment objectives as they combined high profitability (return on equity) and high dividend yield.

Using ESG ratings to refine security selection

This graph applies MSCI ESG Ratings to a hypothetical European growth and income fund invested in 54 securities from the MSCI Europe Index as of Dec. 31, 2017.

The manager can integrate ESG ratings at this stage to help refine the list of selected securities. For example, the manager may investigate securities with low ESG ratings to assess the potential impact of their ESG policies on future profitability and ability to maintain their dividends. Alternatively, the manager may remove stocks that have similar financial characteristics to other stocks, but lower ESG ratings, for example eliminating the worst 10% of securities by ESG rating from the portfolio.

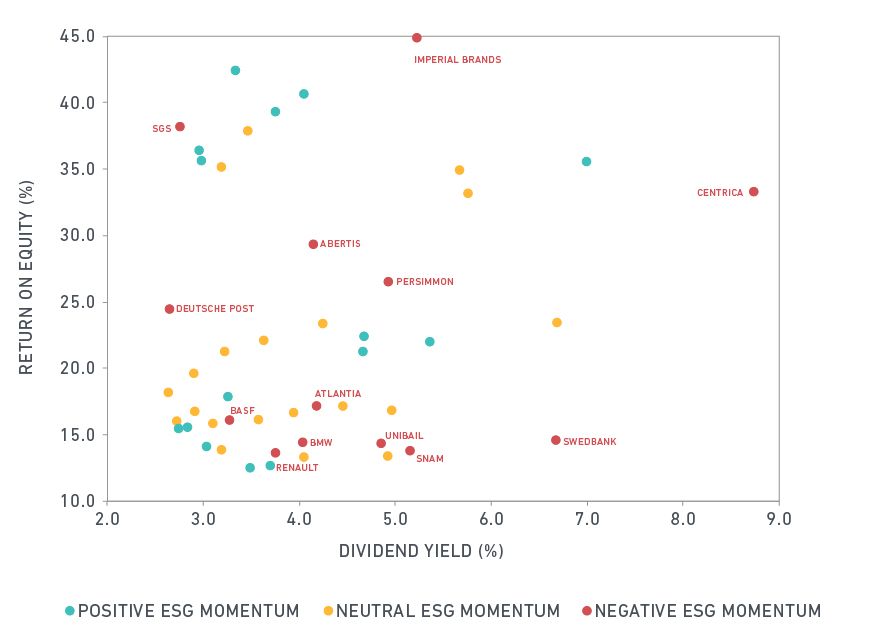

The second step in the active management process is portfolio construction. In practice, various considerations affect the weight of securities in the portfolio, including the manager's conviction about the stock as well as other investment variables, such as country, industry, valuation, volatility, size and liquidity. ESG momentum – the change in ESG rating over the recent past – could be used as one of the criteria to tilt stock weights in the active portfolio. In our example, from the securities that met the profitability and yield criteria and after removing the worst 10% ESG rated companies, the manager could overweight stocks with positive ESG momentum and underweight those with negative ESG momentum, measured over the previous six months.

Using ESG momentum in portfolio construction

Based on a hypothetical European growth and income fund invested in 54 securities from the MSCI Europe Index as of Dec. 31, 2017

TESTING PERFORMANCE IMPLICATIONS IN ACTIVE PORTFOLIOS

We described how an active manager may use ESG ratings and data to exclude securities from the portfolio and to adjust the weights of portfolio holdings. This process did not affect the portfolio's fundamental characteristics and therefore, we assume, did not hinder the manager's investment process. But could this process have improved performance? What would be the impact of incorporating ESG ratings and ESG momentum on the historical performance of actual active portfolios?

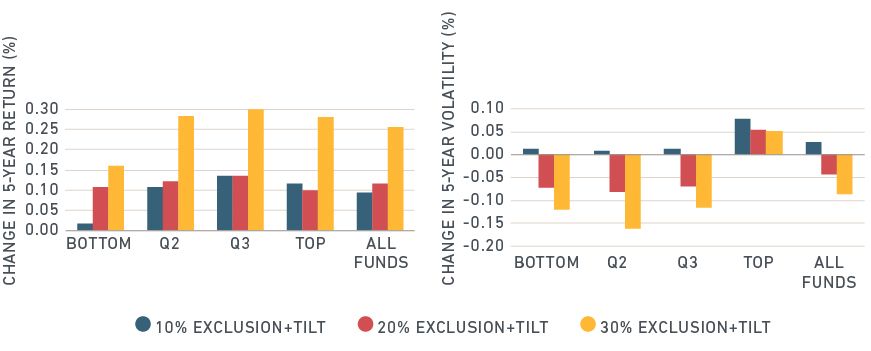

To find out, we applied these two ESG integration approaches to a universe of international equity mutual funds. We divided our sample of over 1,000 funds into quartiles based on rolling 5-year active returns before the application of the ESG overlay. First, we integrated ESG ratings by screening out the worst 10%, 20% and 30% of portfolio holdings based on their ESG rating. Then we doubled the weights of holdings that had positive ESG momentum and halved the weights of holdings that had negative ESG momentum.

Our analysis, summarized in the exhibit below, reveals that integrating ESG information into this sample of active portfolios reduced risk by up to 15 bps per year and improved return by up to 30 bps per year from December 2008 to November 2017. The increase in return was consistent across all performance quartiles while a reduction in risk was achieved for the 20% and 30% levels of exclusion and for the first three performance quartiles. Overall, our analysis shows that integrating ESG ratings and ESG momentum into security selection and portfolio construction would have improved the risk-adjusted performance of this sample of global equity funds over this period.2

Effect of integrating ESG on portfolio risk and return

Source: MSCI Peer Analytics. Based on a universe of 1,182 global and international (global ex US) equity mutual funds. Data from December 2008 - November 2017

ESG data and ratings can provide additional detailed insights into how companies manage ESG-related opportunities and risks. This data can be integrated into the fundamental investment process and may help active managers select stocks and build more ESG oriented portfolios without disrupting the investment process or introducing unintended biases.

The author thanks Zoltan Nagy for his contribution to this post

1 Giese, G. et al. (2017). "Foundations of ESG investing: Part 1: How ESG affects equity valuation, risk and performance." MSCI Research Insight

2 The analysis and observations in this report are limited solely to the period of the relevant historical data, backtest or simulation. Past performance — whether actual, backtested or simulated — is no indication or guarantee of future performance. There are frequently material differences between backtested or simulated performance results and actual results subsequently achieved by any investment strategy. None of the information or analysis herein is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision or asset allocation and should not be relied on as such.

Further reading:

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.