Research - Ric Marshall - U.S. CEO Pay and Long-term Investment Returns

U.S. CEO Pay and Long-term Investment Returns

Ric Marshall author and video

Ric Marshall

Corporate Governance Research (ESG)

Sidebar Navigation

- Executive Summary

- Introduction

- Realized Pay Poorly Aligned with Returns

- What Led to Poor Alignment?

- Pay for Performance and "Say on Pay"

- Conclusion

- Appendix

- Download the Research Paper

- Related Information

Out of Whack

Out of Whack U.S. CEO Pay and Long-term Investment Returns

-

Executive Summary

-

Chapter 1 - Introduction

-

Chapter 2 - Realized Pay Poorly Aligned with Returns

-

Chapter 3 - What Led to Poor Alignment?

-

Chapter 4 - Pay for Performance and “Say on Pay”

-

Chapter 5 - Conclusion

-

Chapter 6 - Appendix

Executive Summary

-

Last year, we asked whether pay packages given to U.S. chief executive officers reflected long-term shareholder returns and found they did not.1 The bottom fifth of companies by equity incentive award outperformed the top fifth by nearly 39% on average on a 10-year cumulative basis.

That study looked at awarded pay — of which 60%-70% reflected incentive stock awards. Awarded pay figures, which are based on the value of the company’s stock at grant date, lay out the range of potential CEO earnings, and is intended to align their interests with those of the company owners. We now extend that study to examine realized pay — how much compensation CEOs actually took home when they exercised their equity grants.

Does realized pay indicate any better alignment between CEO pay and long-term company performance? If anything, realized pay was even more out of whack than awarded pay. More than 61% of the companies we studied showed poor alignment relative to their peers.

KEY FINDINGS

- More than three-fifths of 423 MSCI USA Index constituents had cumulative 10-year realized CEO pay totals that were poorly aligned with the company’s 10-year total shareholder return (TSR) performance, based on the 2006-2015 period.

- Among the most poorly aligned companies, 23 underpaid their CEOs for superior stock performance and 18 overpaid for below-average stock returns, relative to their sector peers.

- The 18 companies that overpaid for underperformance (just 4.3% of our sample) and accounted for nearly 10% of the total sample market cap, which could magnify the impact of their pay for performance misalignment on investors.

- Short-term performance assessments, an over-reliance on share price-related performance measures, poor succession planning and SEC-mandated annual reporting standards were the main factors exacerbating this misalignment.

- None of the companies in the poorly aligned group experienced consistent disapproval on CEO pay, suggesting that shareholders were more focused on payouts in individual years than over longer time horizons.

Long term, these findings suggest that the 40-year-old approach of using equity compensation to align the interests of CEOs with shareholders may be broken.1 Marshall, R. and L.-E. Lee. (2016). “Are CEOs Paid for Performance?” MSCI ESG Research.

Chapter 1 - Introduction

-

Last year, we asked whether CEO pay was aligned with long-term company stock performance.2 In short, we found the answer was “no.”

In that report, we focused on the total CEO pay figures reported in the Summary Compensation Table of U.S.-listed company proxy filings. These figures do not represent what CEOs are actually paid, but rather establish potential pay targets (because the realized value of equity incentive awards may not be known for some time). Our primary objective was to test whether higher CEO incentive targets resulted in higher long-term investment returns, thus benefitting shareholders. Instead, we found an inverse relationship between the two: Companies with lower total awarded pay outperformed companies with higher total awarded pay by nearly 39% on average on a 10-year cumulative basis. By studying a 10-year period, we gain new insight into the extent of the misalignment, as most studies and industry practice focus on shorter time horizons.

In this new report, we extend the scope of our study to include total realized pay, or the amounts that CEOs actually took home, to determine the extent to which these amounts were well aligned with long-term performance.

METHODOLOGY

As we did last year, we compared 10 years of CEO pay figures against 10-year total shareholder returns (TSR). Starting with the MSCI USA Index, which as of March 31, 2017 included 627 large- and mid-cap U.S. companies, we identified 434 companies where a full 10 years of both CEO pay and performance data were available from 2006 through 2015.3

Based on their market capitalization as of that date, the smallest company included was Diamond Offshore Drilling, at $2.3 billion and the largest was Apple Inc., at $615 billion. We arrived at a final sample set of 423 companies by excluding 11 outlier companies with 10-year total shareholder returns exceeding 1,000%, whose inclusion might skew our analysis.

Of these 423 companies, 167 employed the same CEO throughout this 10-year period; pay figures for over 750 individual CEOs were included in the analysis. At companies where two or more individuals served as CEOs in the same year, we included the aggregate amount paid or awarded: Our goal was to evaluate the relationship between pay and performance for each company, rather than for a particular CEO.

Unless otherwise specified, all peer group comparisons cited were based on GICS® sector4 classifications; please see Appendix 2 for a sector breakdown.

To test each company’s 10-year pay figures against its 10-year TSR for the same reporting period, we first compiled cumulative total realized CEO pay for each company. Total realized pay figures represent the amounts actually realized by individual CEOs and other executives in a particular reporting period. These long-term totals are not typically reported but must be calculated using figures reported in individual proxy statements, based on realized amounts attributed to multiple prior awards. They may also include signing bonuses awarded to incoming CEOs and any special severance awards due exiting CEOs.

2 Op. cit. Marshall and Lee.

3 This data was reported in company proxy statements during subsequent years. Thus, the reporting periods were from 2007 through 2016.

4 GICS is the Global Industry Classification Standard jointly developed by MSCI Inc. and S&P Global.

Chapter 2 - Realized Pay Poorly Aligned with Returns

-

How strongly was 10-year cumulative CEO realized pay correlated with 10-year investment returns over this period? Exhibit 1 shows that there was little correlation.

Exhibit 1: 10-Year Total Shareholder Return vs. 10-Year Cumulative Realized Pay

10-year TSR as of Dec. 31, 2015 vs. 10-year cumulative total realized CEO pay as reported in 2007-2016 proxy statements, reflecting a one-year lag in reporting.

Source: MSCI ESG Research

If CEO pay practices were truly well aligned with long-term performance, we would expect to see those companies whose CEOs realized the highest pay levels exhibiting the highest investment returns, and those with the lowest pay levels exhibiting the weakest returns. This was not the case. Instead, the scatter chart indicates an overall lack of correlation between long-term performance (10-year TSR) and cumulative realized pay, as indicated by the very low R2 of 0.0093.5

To better understand this low level of correlation, we organized the companies in our sample into both pay and performance quartiles, based on their 10-year cumulative realized pay and 10-year TSR figures, relative to their GICS sector peers. We used sector-based peer groups rather than industry-based groups to ensure we had adequate numbers of companies in each group.

Exhibit 2 shows how companies’ realized pay lined up against long-term shareholder returns. The green text and shading highlights the groups where pay and performance were generally well aligned, while the red text and shading indicate the most extreme cases of misalignment. The remaining companies fall into boxes with yellow highlighting, indicating some degree of misalignment.

As we can see, more than three-fifths (61.5%) of the companies — 260 of the 423 firms in our sample — experienced poor alignment between realized pay and shareholder returns. In comparison, only 163 companies (38.5% of the total) had pay practices that were generally well aligned with TSR. At the extremes of the poorly aligned group, 23 companies underpaid their CEOs for long-term outperformance, and 18 companies overpaid for long-term underperformance.

Exhibit 2: 10-year Pay for Performance Alignment Analysis

Higher TSR → Higher Pay → Severely Misaligned 23 companies Highest TSR Quartile

Lowest Pay QuartilePoorly Aligned 55 companies Highest TSR Quartile

Average Pay QuartilesGenerally Well Aligned 30 companies Highest TSR Quartile

Highest Pay QuartilePoorly Aligned 51 companies Average TSR Quartiles

Lowest Pay QuartileGenerally Well Aligned 99 companies Average TSR Quartiles

Average Pay QuartilesPoorly Aligned 58 companies Average TSR Quartiles

Highest Pay QuartileGenerally Well Aligned 34 companies Lowest TSR Quartile

Lowest Pay QuartilePoorly Aligned 55 companies Lowest TSR Quartile

Average Pay QuartilesSeverely Misaligned 18 companies Lowest TSR Quartile

Highest Pay QuartileCompany count per pay versus performance alignment, based on 10-year TSR relative to GICS sector peers as of Dec. 31, 2015 vs. 10- year cumulative total realized CEO pay relative to GICS sector peers as reported in 2007-2016 proxy statements of Dec. 31, 2016. Reflects a one-year reporting lag.

Source: MSCI ESG Research

While those 18 companies who most severely overpaid for underperformance represented just 4.3% of our sample by count, they represented more than 9.7% of the total by market cap, which could magnify the impact of their pay for performance misalignment on investors.6 The average 10-year TSR for this group was a cumulative 20.2% — one eighth of the 172% cumulative return for the overall sample. Average cumulative realized pay for companies that overpaid for underperformance during this period was $242.4 million, compared to $136.7 million for all companies — a spread of $105.7 million per company.

Thus, we find that CEO realized pay over the past 10 years was poorly aligned with long-term investment returns at a majority of large-cap U.S. companies, and in some cases severely so. Other researchers have disagreed,7 but most of these studies used shorter time periods for testing alignment. When we cut the scope of our analysis to just five years instead of 10, we arrived at results similar to these other studies. Exhibit 3 plots realized pay totals as reported for the single year of 2016 against five-year total shareholder returns as of the end of the same performance period and finds a somewhat higher — but still weak — R2.

Exhibit 3: Realized Pay Better Aligned with Short-term Results

Five-year TSR as of Dec. 31, 2015 vs. one-year total realized CEO pay, as reported in 2007-2016 proxy statements.

Source: MSCI ESG Research

There is a higher degree of correlation between pay and performance in this instance than for the 10-year period, where little exists. We found similar results when we examined other individual year pay totals against both three- and five-year performance cycles, while comparing five-year pay totals against five-year total returns reduced the correlation by half.While such results were more supportive of current pay for performance practices, for long-term investors all of these combinations are too short term-oriented, and fail to take into consideration how equity investments delivered value over longer holding periods.

At least one other recent study, which covers a similar time period but looks at an even larger sample set, bears out the importance of analyzing pay over extended periods. Compensation consultant Stephen O’Byrne found that, “Only about a fifth of S&P 1500 companies have relatively well managed CEO pay.” This study also found that 10-year total returns relative to peers were higher at those companies where pay was best aligned.8

5 The R-squared value (R2) indicates the percentage of the variance explained by the model. A very low figure indicates that the model provides little explanation.

6 No clear pattern of board leadership, diversity or independence emerged among these companies. Seven retained the same CEO throughout the period under review. Among the remaining 11 companies where CEO changes did occur, five experienced well managed successions, but three experienced multiple CEO transitions in a single year. All either were or had been regular dividend payers, and most have been active participants in corporate stock repurchase programs, but two have experienced problems so severe that they were forced to suspend the payment of dividends.These companies were also representative of a wide range of sectors, sizes and ownership types, and their pay plans varied in several key respects. All but one relied primarily on three-year performance tests and vesting standards, and none reported cumulative realizable pay on a regular basis. Twelve employed share price-based performance measures, in some cases along with fundamental measures, or as a modifier to those measures, but the other six did not.

7 For example, see Kay, I. T., B. J. Lane and B. Wilby. (2015). “CEO Pay Well Aligned with Company Performance.” Pay Governance LLC.

8 O’Byrne, S. “Pay For Performance At S&P 1500 Companies.” (2017). Seeking Alpha, June 13, https://seekingalpha.com/article/4081082-pay-performance-s-and-p-1500-companies. This study also suggested two tools to use to improve pay for performance: a sharing analysis and a “perfect” pay plan.

Chapter 3 - What Led to Poor Alignment?

-

At nearly all of the large-cap companies that comprise the MSCI USA Index, equity award targets were granted on an annual basis, even when the intent was to incentivize long-term performance. Once vested, these awards can be exercised, and those realized amounts are reported on an annual basis. While there were other pay elements that also contributed to total pay, including base salary, perquisites and short-term incentives, these equity awards comprised on average 60%-70% of total awarded CEO pay and an even greater percentage of total realized pay.9

In theory, such awards are intended to incentivize long-term performance by better aligning the interests of company managers – the agents – with the interests of the company’s investors – its owners or principals.10 In reality, a number of conditions subvert this objective:

- An over-reliance on performance measures that are overly sensitive to short-term share price movements.

- The prevailing assumption that three years is a sufficiently “long term” measurement period for equity awards.

- Poorly managed CEO successions,11 which too often resulted in extraordinary one-year payouts that were poorly aligned with long-term performance.

In most instances where misalignment occurred, a key underlying problem was the susceptibility of executive pay plans to extraordinary short-term single-year payouts.12 Not surprisingly, these enormous payouts were poorly aligned with long-term investment returns, a problem that was often hidden beneath these plans’ sheer complexity.When it comes to aligning incentive payouts with long-term strategy, any measure that tests performance in as little as three years may suffer from a degree of sensitivity to short-term price changes.

Exhibit 4: Short-term Price Movements vs. Long-term Returns

10-year Total Shareholder Return Decomposition

Data from 2006 to 2015.

Source: MSCI BarraOneExhibit 4 shows an approximation of the relative contribution of the three key factors that account for changes in total shareholder return over time: share price movement, dividend yield and dividend growth, over 10 one-year periods. In four of these periods, share price movements accounted for the largest shifts up or down; this particularly applied in the mortgage crisis years of 2008 and 2009.

Using longer time periods, however, dramatically changes the results, as we can see in Exhibit 5. The contributions of dividend yield and dividend growth became much more significant than share price movement. Research shows that the relative contribution of share price movement diminished even further over time.13 From the perspective of long-term investors who seek sustainable returns, dividend yield and dividend growth may be more valuable measures.

Exhibit 5: 10-year Total Shareholder Return Contribution – Average Returns

MSCI USA - Average return contributions 2006-2015

Chart shows absolute values, ignoring whether contributions were positive or negative. Source: MSCI BarraOne

Companies whose CEO pay practices were poorly aligned with shareholder returns also experienced greater variability in pay from year to year, reflecting greater frequency of extraordinarily high one-year payouts. Variability from year to year was somewhat higher among the poorly aligned companies compared to the well-aligned companies, and significantly higher among the 18 companies (a subset of the poorly aligned group) that overpaid for underperformance (Exhibit 6). Nearly all of these companies experienced one or more years of extraordinarily high realized pay totals, relative to the entire universe.

These problems were exacerbated further by the prevailing three-year standards that are used for both testing and vesting Long-Term Incentive Plan (LTIP) equity awards. After just three years, the value of the awards can easily be influenced by short-term price changes, which may or may not be aligned with the company’s eventual long-term performance.

Exhibit 6: Year-to-Year Total Realized Pay Variability

Based on year-to-year standard deviations over the 10-year period observed.

Source: MSCI ESG Research

Were companies with certain ownership structures or board attributes more likely to experience pay misalignment than others? We did not find this to be the case. Controlled and widely held ownership forms were represented equally among both well and poorly aligned companies, as were the incidence of combined CEO/Chairman roles, overboarded directors (those serving on too many boards) and overly entrenched boards. Both groups included almost exactly the same percentage of companies that experienced one or more CEO changes during the 10-year period studied, and very similar mixes of long- and short-tenured CEOs. Both groups were also very similar in terms of average market capitalization.

9 Jensen, M. C. and K. J. Murphy. “CEO Incentives - It's Not How Much You Pay, But How.” (1990). Harvard Business Review, No. 3, pp. 138-153.

10 This agent-principal theory originated more than 40 years ago. See Jensen, M. C. and W. H. Meckling. (1976). “Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure.” Journal of Financial Economics, Vol.3., No.4, pp.305-360. Jensen and Meckling’s piece is widely viewed as having initiated modern CEO pay incentive theory.

11 The higher incentive pay costs identified here represent only a small fraction of the total costs that result from poor succession planning. For additional insights into the potential costs involved, see Harrell, E. (2016). “Succession Planning: What the Research Says.” Harvard Business Review, December, pp. 70-74.

12 Exceptionally high single-year payouts were either due to the costs associated with changes in CEOs, resulting in overlapping payments and one-time exit awards and/or signing bonuses. In addition, these payouts may have reflected how sharply rising stock prices could buoy the value of previously granted equity awards.

13 Gupta, A., D. Melas, R. Suryanarayanan and A. Urban. (2016). “Global Markets & Return Drivers.” Analysis for the Ministry of Finance, Norway, MSCI.

Chapter 4 - Pay for Performance and “Say on Pay”

-

We also examined whether shareholder votes on company executive compensation (“say on pay”) bore any significant relationship to the alignment of CEO pay with long-term shareholder interests.14 We found that they did not.

None of the companies in the poorly aligned group experienced consistently negative voting results on CEO pay packages. This was especially true for the group that was overpaid for underperformance, all but one of which garnered favorable votes on say on pay in excess of 90% of all votes cast in at least one year.

Rather than focusing on CEO pay and stock performance over time, we found that shareholders in general were more focused on payouts in an individual year.

- Even where strongly negative votes were cast in a particular year, pay plans at those same companies generally were well supported in both prior and subsequent years.

- In many cases, a strongly negative vote appeared to reflect an immediate response to elevated levels of pay.

- In some instances, the negative vote was based on higher awarded pay figures, while in others it was based on higher realized pay figures.

- Other instances appeared to be driven by prior year stock performance problems, regardless of the level of pay, or by concerns related to a transition in CEOs which may not have had any discernible relationship to the company’s CEO pay practices.

In his own recent report on CEO pay and long term performance, Stephen O’Byrne15 reported a similar lack of concern for long-term pay for performance alignment among U.S. say on pay voters.14 The 2010 Dodd-Frank Wall Street Reform and Consumer Protection Act mandated that U.S. listed companies periodically submit CEO pay plans to shareholders for a non-binding vote. We now have five full years of Say on Pay voting results to draw upon, comprising 1,999 discrete voting results,

15 Op. cit.

Chapter 5 - Conclusion

-

Last year, we asked whether CEO pay awards reflected company stock returns and found that they did not. This year, we examined the relationship between realized CEO pay — how much CEOs actually earned — and long-term stock performance, and found they were misaligned in more than three-fifths of the companies we studied from 2006 to 2015.

Why were pay and performance so out of whack at the majority of U.S. large-cap companies in our study? We found that an over-reliance on short-term measures of stock price performance, use of three years as the performance testing and vesting period for equity awards, poorly managed CEO successions that too often resulted in extraordinary one-year payouts, and annual, SEC-mandated reporting standards were the primary culprits.

When we looked at the most severely misaligned companies, we found that 23 of these underpaid their CEOs for superior stock performance and 18 overpaid for below-average stock returns, relative to their sector peers. The 18 companies that overpaid for underperformance included six of the largest companies we examined, accounting for nearly 10% of the total sample market cap. Severe misalignment among these companies could magnify the impact on investors.

A board’s ability to align CEO pay with the company’s long-term investment returns is one of its most important challenges and responsibilities. For the past 40 years, the use of equity-based incentive awards as a means of accomplishing this critical task has gone virtually unchallenged, despite widespread concerns about the level of CEO pay at many U.S. companies.

Are equity awards still the best means for aligning CEO pay with the interests of long-term investors? The degree of misalignment between realized CEO pay and long-term investment returns at more than three-fifths of the companies included in this report should be more than sufficient cause for reevaluation.

Further reading

Out of Whack: U.S. CEO Pay and Long-term Investment Returns

Chapter 6 - Appendix

-

APPENDIX 1: CEO PAY TERMS AND DEFINITIONS

We generally favor use of the simpler term “pay” over “compensation” or “remuneration,” but consider all three terms to be interchangeable.

We define total awarded pay as the total pay figure reported in the summary compensation table that appears in all publicly held U.S. companies’ annual proxy filings. We previously used the term total summary pay for this figure but feel that total awarded pay is a more accurate description. For U.S. companies, these figures include the total annual pay awarded plus the grant date value of any stock option or restricted share grants awarded.

Though widely regarded as the baseline measure of CEO pay, these total awarded pay figures very rarely end up being the amounts actually paid out to a particular individual. Instead they serve as target amounts which may or may not vest, or become realizable, at some point in the future. As of December 2016, the average vesting period for such awards was three years, and the amounts realized have ranged from as little as zero to more than three times the original target value, depending on the terms of a particular pay plan.

Because most companies initiate new long-term incentive awards annually, the total realizable pay that is potentially available to a particular CEO quickly accumulates, shifting continuously up or down with the company’s share price. While the SEC has mandated since 2006 that the value of each individual award be reported, as of the report date, these awards are rarely reported as cumulative totals, making it difficult for investors to estimate potential future payouts.

We define total realized pay as total annual pay plus any prior period equity-based award values actually realized in the course of the reporting year. As with realizable pay, the SEC mandates the reporting of these values individually, but aggregate totals are rarely presented.

For purposes of this report, we calculated both cumulative total awarded pay and cumulative total realized pay, in this case for the entire 10-year period under study (from proxy year 2007 for performance year 2006 through proxy year 2016 for performance year 2015). The SEC does not require companies to disclose such long-term figures, but we believe both are essential to analyzing CEO pay over long term periods.

APPENDIX 2: GICS SECTOR PEER GROUPS

Unless otherwise specified, all peer group comparisons cited here were based on GICS sector classifications.

Exhibit A1 – MSCI USA Sample Set Sector Distribution

MSCI USA sample set companies by GICS sector, as of March 31, 2017.

Source: MSCI ESG Research

APPENDIX 3: SECONDARY COMPENSATION TABLESWhile the summary compensation table is the cornerstone of the current compensation discussion and analysis (CD&A) reporting standard, more detailed data can be found in several secondary tables:

- Breakdowns of the short- and long-term incentive plan awards are cited in the main summary table. These breakdowns generally include a description of the performance measure(s) that must be met before such awards can be realized, including any peer-based benchmarking conditions and relevant vesting schedules.

- Year-over-year pension gains and cumulative pension entitlements, based on the number of years of service credited to each individual. These figures represent tax-qualified pension plan benefits.

- Non-qualified deferred compensation (NQDC) awards. These figures represent additional deferred pay awards of various types, including Supplemental Employee Retirement Plans.

- Severance entitlement figures, based on various termination scenarios, including possible change of control.

Companies must also report any gains actually realized by each individual over the course of the prior year.16 In most cases, such gains appeared in one of two forms: either option award gains realized or share awards realized on vesting, both of which are based on achieving past equity incentive plan goals. Disclosure regarding such awards can vary considerably from company to company. A few companies have even begun reporting on potential realizable pay, which refers to any remaining awards still outstanding. But disclosure in this area is still mostly a matter of company and compensation committee preference, making company-to-company comparisons very difficult.Some awards are made outside of normal pay plans but, if implemented, can be considerable. For example, any additional pay realized as a result of executive service, such as severance or change of control awards or new signing bonuses must be reported, though some of these figures are buried in footnotes and sidebars. Such figures are often referred to as out-of-plan or outside-of-plan awards, as they represent awards that were not anticipated by the company’s various formulaic incentive plans.17

APPENDIX 4: MSCI’S CEO PAY SCORING METHODOLOGY

MSCI ESG Research evaluates CEO and other executive pay practices at all MSCI-rated companies, including, where disclosed, specific pay figures. Pay is scored primarily based on levels of pay relative to peers, as well as specific features of the pay program design.

While the current report is focused on U.S. CEO pay practices, MSCI ESG Research’s executive pay coverage can be used for companies around the world.

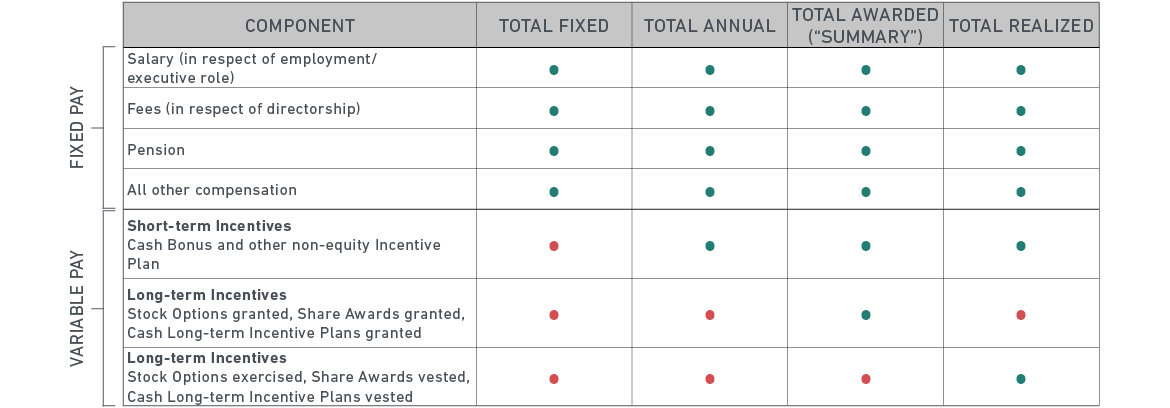

Exhibit A2: The Components of Executive Pay

EXECUTIVE PAY PEER GROUPS

Executive Pay Peer Groups are used by many of our pay key metrics for comparative, benchmarking and scoring purposes. Individual companies are assigned to these peer groups based on three criteria:

- Industry

- Market Capitalization

- Peer Market

Industry assignments are based on the GICS industry classification system, while Market Capitalization is based on the following size references, as updated quarterly.

Exhibit A3: MSCI’s Pay Peer Market Cap Classifications

Peer Market assignments divide companies into regional peers on the basis of a company’s home or primary trading market.

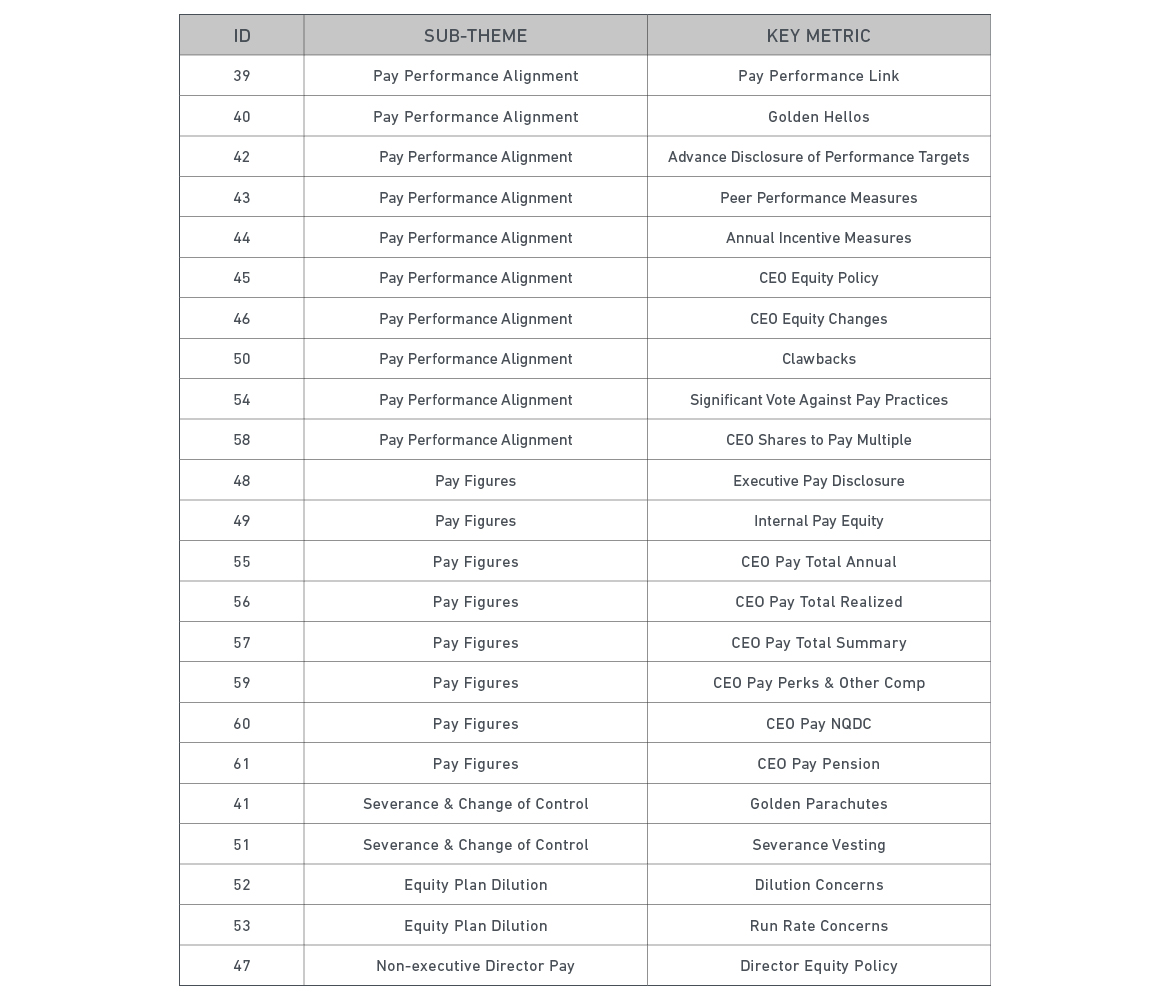

EVALUATING PAYScoring for corporate pay practices is based on the evaluation of 23 individual key metrics, which are further organized for company report presentation purposes under the following five pay sub-themes:

Exhibit A4: MSCI’s CEO Pay Sub-themes and Key Metrics

Key metrics included in the overall pay theme evaluate the following concepts:

- Total pay levels (annual cash pay, realized total pay and granted pay opportunity, as well as perquisites and pension values) relative to market-cap and industry-based peer groups and internal pay equity across the executive team.

- Sign-on and severance provisions, including golden hellos and golden parachutes, where special awards are paid without requiring performance conditions.

- Performance goals and the alignment of pay with performance in both short- and long-term incentive plans.

- Policies and practices regarding the use of equity, including dilution and run rate concerns, as well as policies regarding CEO and director equity ownership.

Reflecting the varying levels of disclosure across markets, pay rankings are also designed to prevent companies with poor disclosure from being rewarded.

16 U.S. Securities and Exchange Commission, Release Nos. 33-8732A; 34-54302A; IC-27444A; File No. S7-03-06 (March 2006).

17 For a recent summary of the size and frequency of such awards, see “Outside of Plan Awards 2015,” by the Canadian Pension Plan Investment Board and Ontario Teachers’ Pension Plan.

内嵌的应用

ESG Governance Metrics

ESG Governance Metrics

Learn more about how MSCI can help you identify risk associated with misaligned pay and other corporate governance challenges.

Quote