面包屑导航

Multi Asset Class Factor Models

Multi-Asset Class Factor Models

Multi-asset class factor models

We see a shift towards investors seeking outcome oriented strategies to help balance risk profiles with return targets. Multi-strategy, outcome-oriented and balanced funds, are all exposed to a broad set of risk and return drivers that are dynamic in nature, with interrelationships that change over time. Multi-Asset Class Factor Models help investors more clearly identify the drivers of risk and return in these complex, dynamic strategies.

The MSCI Multi-Asset Class Factor Model provides:

- Factor-based asset allocation to target key drivers of risk and return

- The identification of systematic strategies in equities, fixed income, commodities, and currencies

- Improved communication of portfolio exposures at different levels of granularity for different audiences

Asset classes are vehicles to gain exposure to drivers of risk and return

Factors have been proven by academic research for many years to exist across asset classes. Factor-based asset allocation can help:

- Simplify thousands of exposures to a smaller set of key risk and return drivers

- Reduce the number of risk and return forecasts and validate those choices

- Target risk factors with historical positive risk premia

- Make multi-asset class portfolio exposures easier to communicate

Factor based asset allocation provides a deeper lens into the key drivers of risk and return. As portfolios transition from traditional asset class allocation to a factor based allocation process, MSCI’s MAC Factor Model can help investors focus on factor exposures across asset classes in in a consistent manner.

MSCI’s latest factor innovation, the MSCI Multi-Asset Class Factor Model (MSCI MAC Factor Model), provides high to low granularity in looking at factors through an integrated and consistent framework.

The MSCI MAC Factor Model provides the following support and insights for global investing.

Supports factor-based asset allocation

- A consistent, integrated framework between high-level and detailed factors across asset classes

- Link asset class decisions to manager and security selection

Capture systematic strategies across asset classes

- Introduce systematic strategy factors beyond equities

- Multi-asset class systematic strategy factors distinguish factor betas from alpha and traditional beta

Provides multiple levels of granularity to communicate global, MAC exposures

- Align factor granularity with reporting to maximize effectiveness

- Consistent risk and return attribution

MAC Video

MSCI Multi-Asset Class Factor Model Video

DMF Button

The MSCI Multi-Asset Class Factor Model

Click on the pyramid below to learn more

Interactive Assets

- 9 top level factors to communicate and report the key drivers

- Designed for the board/top level reporting

- Integrated transition from board view to CIO/CRO to PM

- Strategic asset allocation across the 25 Factor Premias

- Review the investment objectives set by managers multi asset class portfolios

- Build portfolios that have active tilts towards targeted investment objectives

- Manage concentration and aggregate exposures across multi-managers across regions and sectors

- Deeper view of exposure of industries, countries, rates, real estate, etc.

- Ability to drill down into granular drivers of risk while maintaining consistency in SAA and reporting at top level

- Single manager analysis

- Strength of integration and consistency provides unparalleled depth in to asset allocation across equity models, fixed income factor models etc.

Download the factsheets

Download the factsheets to learn how each tier provides insight for better asset allocation.

内嵌的应用

内嵌的应用

MAC tier 1 factsheet

MAC tier 2

内嵌的应用

MAC Tier 3 factsheet

MAC tier 4 factsheet

MAC Content Part 02

Factor allocation across asset classes

The changing investment landscape and access to a greater number of multi-asset class factors is shifting many portfolios to actively allocate across asset classes. As the demand for new sources of alpha across asset classes increase, there is a need for a multi-tiered, multi-asset class factor model to provide consistency throughout the investment process.

The MSCI Multi-Asset Class Factor Model provides further insight and control into multi or single asset class investing. The tiered structure of the MSCI MAC Factor Model allows multiple levels of granularity.

Click on the asset class below to discover more

Interactive Assets

|

Factor-based Asset Allocation

|

||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| T1 Factors | ||||||||||||

| ASSET CLASSES | ||||||||||||

|

Factor-based Asset Allocation

|

Public Equity | Domestic Equity | ||||||||||

| Global Equity (DM) | ||||||||||||

| Global Equity (EM) | ||||||||||||

| Fixed Income | Global Governments | |||||||||||

| Global Corporates | ||||||||||||

| Global IPB | ||||||||||||

| Alternatives | Real Estate | |||||||||||

| Private Equity | ||||||||||||

| Commodities | ||||||||||||

| Hedge Funds | ||||||||||||

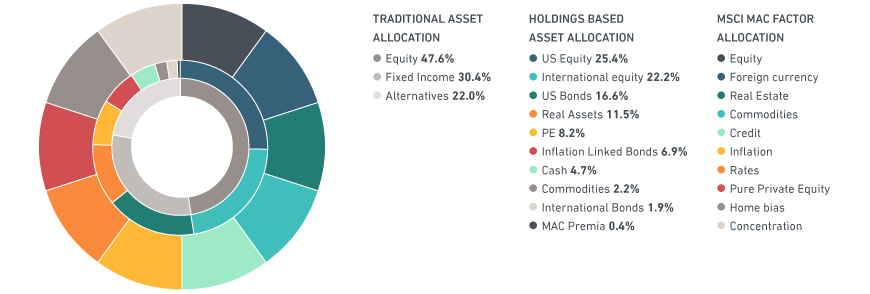

ASSET ALLOCATIONS IN A MULTI-ASSET CLASS PORTFOLIO

Asset allocations in a multi-asset class portfolio

The MSCI Multi-Asset Class Factor Model helps investors navigate the complex nature of the global markets. It is difficult to target and optimize global and systematic themes such as global credit, EM equity or EU sovereign spread in the construction of a portfolio. The MSCI MAC Factor Model enables investors to implement additional assets in order to better manage total portfolio investment objectives.

Download the MSCI Private Infrastructure Modelling Service factsheet to learn how infrastructure holdings impact a multi-asset class portfolio’s risk.

Download the brochure

(PDF, 163 KB) (opens in a new tab)

Applications

The MSCI Multi-Asset Class Factor Model helps solve some of the challenges in managing and communicating factor exposures in a portfolio by:

- Provides consistency across asset classes

- Supports factor-based asset allocation

- Introduces MAC systematic strategies

- Simplifies communication of key exposures with the appropriate level of granularity

- Detailed exposures for portfolios managers

- Core exposures for asset class managers

- Global exposures for asset allocators

Factors by MSCI

Factors by MSCI

MSCI has developed Factor Indexes, FaCS and Analytics backed by four decades of Factor research and innovation.

MSCI Japan Equity Factor Models

MSCI Japan Equity Factor Models

Leverage factors like sustainability, crowding and machine learning for building more resilient portfolios as market conditions change.

How Alternatives fit into a Multi-Asset Class Portfolio

How Alternatives fit into a Multi-Asset Class Portfolio

In this session, Yang Liu, Executive Director in private asset class research at MSCI provides thoughts on the role of private assets in diversified portfolios.