Social Sharing

Article 1 banner content

Office Real Estate: The Post-Pandemic Trends Affecting Investment

Article 1 content

It is not a matter of “if” but how the pandemic will change the way we work

There are convincing arguments for preserving the more flexible work practices of the past year, as well as for a return to the office for the sake of productivity. The new reality will likely be somewhere in between.

Investors in office real estate will need to adapt to this new reality. Lease terms could, to some extent, shrink both in duration and area as tenants capitalize on the savings resulting from a nimble workforce. High occupancy in gateway cities, and its attendant capital growth, are under threat as many employees have more choices of where to work and live.

Adaptation is equally an imperative for office real estate managers. The lockdown’s accelerated a flexible working trend already underway, so asset managers may need to step up and be more proactive. The new conditions call for managers to provide work spaces that meet tenants’ needs -- even anticipate them. That will be possible by deploying property technology.

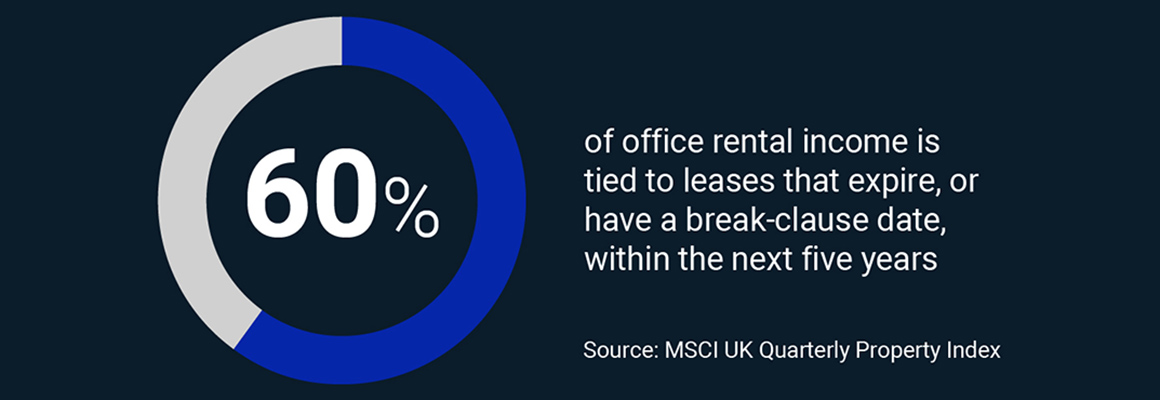

Office rental income in the UK is tied to leases

The full impact of COVID-19 on office real estate is yet to be determined, but a snapshot of the UK market points to challenging times ahead. Some 60% of office rental income in the MSCI UK Quarterly Property Index is tied to leases that either expire or have a break clause in the next five years.

An MSCI simulation of possible outcomes for income erosion based on the 2019 pattern of vacancy rates after a lease expiry or break clause exercise showed that, conservatively, around 40% of office rental income could be eroded by 2025.

Institutional investors may fear that the evolution of work customs and the consequent demand shock portend the end of the steady cash flows typical of office real estate investing. That needn't be the case.

As income streams become more directly linked to managers’ ability to innovate, two things could happen. First, managers may adapt their practices to offer workspaces that are engaging and functional. Then, investors could adjust their investments to the emerging office real estate landscape, likely realizing that the changes aren’t as traumatic as they seem at first.

Commercial real estate managers are awakening to the new paradigm

Ensuring a healthy and safe workplace, followed by identifying and generating cost savings, are the top priorities of global corporate real estate executives. Pre-pandemic, these leaders’ main goals were to enable the core business and provide quality service on time and within budget, according to a CBRE survey of 95 executives with a combined portfolio of 449 million square feet, conducted in mid-2020.

In a way, both office real estate investors and managers may need to redefine the meaning of stable income. This could be driven by managers skilfully understanding tenants’ business models and needs and providing them with a compelling product. After all, stability is enforced by a contract, and contracts reflect what is provided to tenants; if clients are satisfied enough they will stay in the property.

This dynamic is already at work in residential real estate investments. Investors in large apartment buildings, particularly in the US, are exposed to annual leases that, to many, spell high volatility. In fact, properties with dozens of units may provide some income diversification. They are also run by skilled and attentive management that is focused on sustaining the flow of tenants.

The growing need for active managers may also lead to greater specialization of real estate asset managers.

Those primarily focused on capital allocation to different asset classes and geographies may move further into offering targeted investment products, and tap into the pool of active office space managers as needed.

Managers involved in the intense running of real estate assets will likely become more specialized and eventually could market their products and services directly to institutional investors.

Furthermore, large operating platforms currently used for investing and managing retail assets, particularly in the US, could become a model for office real estate management. Institutional investors seeking to maximize their exposure will likely embrace platforms that invest in office real estate products and also own the underlying asset.

Proptech is becoming more commonplace in real estate management

Lastly, but not least, technology tailored to the real estate industry, or proptech, is looking to become more commonplace in office real estate management. The innovative use of data can equip managers with tools and information to better attract and retain tenants, as well as reduce operational costs.

Proptech has already ignited a transformation of real estate management in warehousing and malls. In an office setting, it can be used to measure productivity at desk level and apply the data and insights to help tenants optimise the use of space. The manager can then be more of a consultant in an increasingly fluid relationship with tenants.

If crisis breeds opportunity, then the workplace evolution is decisively pushing the boundaries of office real estate investment. The flexibility now cherished by office dwellers everywhere is equally required of institutional investors and asset managers if they are to prosper in a post-COVID world.

To read more insights on the impacts of COVID-19, read the MSCI Real Estate Research Snapshot report.

Article 1 related content

Related Content

COVID-19 and Office Income: What Could Lie Ahead?

Nearly 60% of the UK Quarterly Property Index’s office rental income comes from leases that expire or contain a break-clause date over the next five years.

Read the BlogReal Estate Investing

Our analytical solutions make it easier to increase and manage private real asset investments.

Read More