Has Inflation Affected the Bond-Equity Relationship? Title

Has Inflation Affected the Bond-Equity Relationship?

Social Sharing

6/21 QuickTake intro

June 21, 2022

The sharp rise in inflation over the past year and a half, combined with growing concern over the U.S. economy’s strength, may prompt investors to rethink basic assumptions underlying portfolios comprised of bonds, equities and other asset classes.

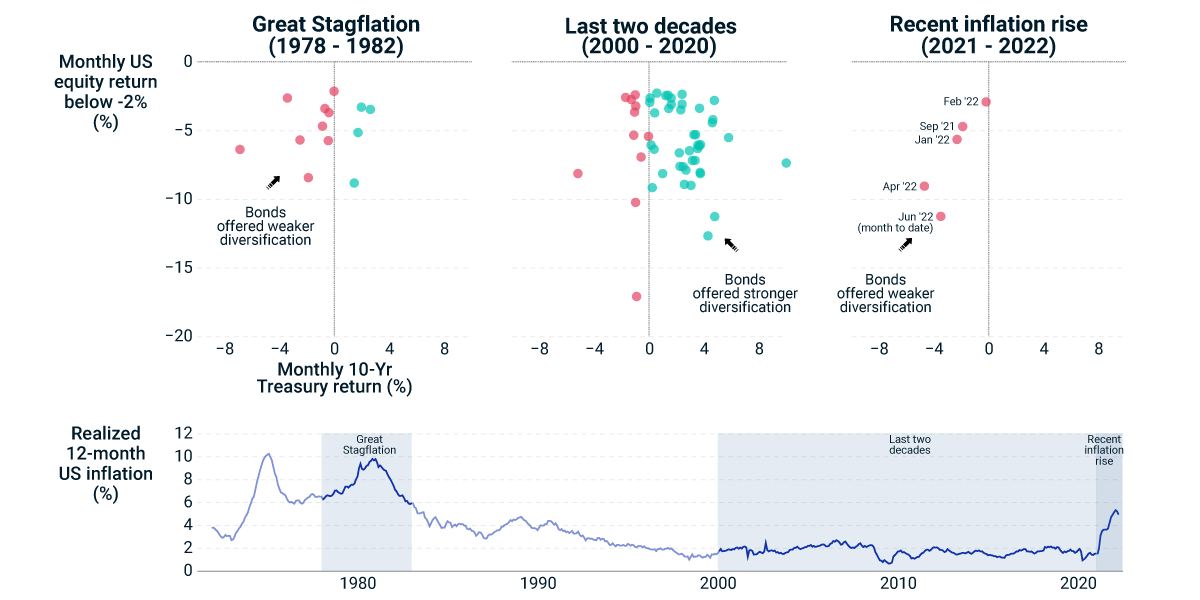

As shown below, major stock sell-offs (defined as monthly returns below -2%) since September 2021 coincided with sell-offs in Treasurys. By contrast, in the prior two decades, equity sell-offs tended to occur with Treasury rallies. Stated otherwise, bonds’ stabilizing influence in multi-asset-class (MAC) portfolios has been less apparent in the recent data. This calls into question the diversification benefits of balanced portfolios, including the popular 60%-equity/40%-bond strategy.

Investors may be further unsettled by observing that the recent Treasury-equity co-movement is similar to that during the Great Stagflation, between 1978 and 1982, when large equity sell-offs tended to coincide with sell-offs in Treasurys.

The beginning of a new era?

Investors trying to project future co-movements between bonds and equities now face the challenge of interpreting the historical data, identifying drivers and projecting potential paths of growth and inflation.

The Federal Reserve’s actions might also play an important role. During his June 15 remarks, Fed Chair Jerome Powell underscored the Fed’s intense focus on reducing inflation and expressed satisfaction that the tightening of financial conditions over the past seven months is healthy and will continue to temper growth and bring demand into better balance with supply.

Can the Fed affect the bond-equity relationship? The Fed’s credibility with market participants may be the key.1 A vigilant Fed bringing down market inflation expectations could help restore the role of bonds as diversifiers in MAC portfolios, tending to rally when equities sell off.

Are bonds still an anchor, or just added dead weight?

Treasury return is computed using the 10-year constant-maturity Treasury yield, retrieved from the Federal Reserve Bank of St. Louis’s FRED database. Equity return is from the MSCI USA Index. U.S. realized inflation is the personal-consumption-expenditures price index, excluding food and energy, from the U.S. Bureau of Economic Analysis.

1In MSCI's macro-finance model, elevated supply-side risk induces a negative inflation-growth correlation and may result in a positive return correlation between stocks and bonds.

6/21 Quick Take related content cards

Related Content

Fed Policy and the Threat of Stagflation

Russia’s invasion of Ukraine has amplified supply-driven inflation and growth concerns in the U.S. and led to a recognition that last year’s high, demand-driven inflation might not have been transitory.

Explore MoreAre rates and equities losing their balance?

For most of the past two decades, a benevolent relationship between bonds and equities has provided a hedge for asset allocators. We used our macroeconomic model to examine whether this risk protection could disappear in a secular shift.

Learn MoreBonds and Equities: Still Happy Together?

Investors accustomed to bonds anchoring their portfolios during stormy equity markets may seek to reevaluate their portfolio strategies.

Read More