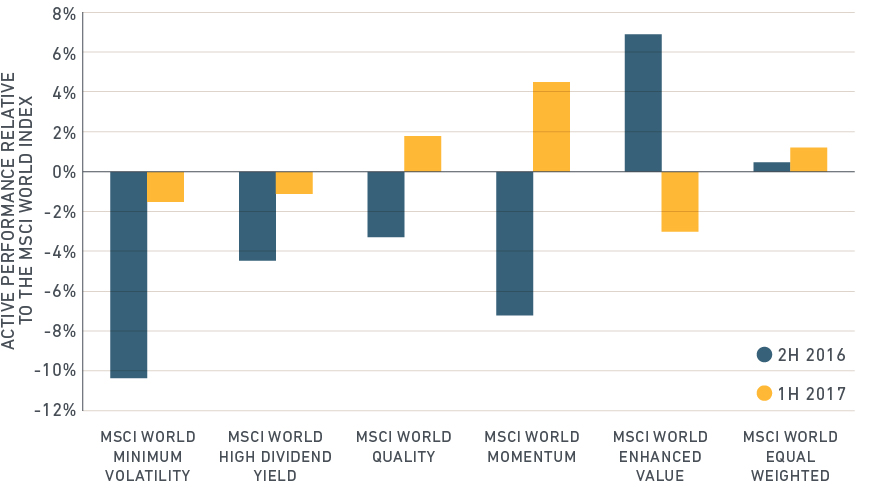

We have seen substantial rotation in factor index performance in the past 12 months. Value, the best-performing equity factor index in the second half of 2016, was the worst performer in the first six months of 2017. On the other hand, Quality, which had lagged last year, has performed well in 2017. But this has left quality stocks at peak valuations for the past decade, confronting investors with a question: Is it time to reduce exposure to this factor?

MSCI World Factors indexes: Value Reverses While Momentum and Quality Accelerate

Source: MSCI, Data as of 30-June-2017

The MSCI World Quality Index targets companies with modest leverage, strong profits and low earnings variability and is often used in connection with a defensive investment strategy. Since the 2008 financial crisis it has been the leading performer among MSCI World factor indexes. This suggests that investors have rewarded companies with durable business models and sustainable competitive advantages. Through June, Quality, along with Momentum, has been underweight financials and overweight technology, leading to similar outcomes in their performance.

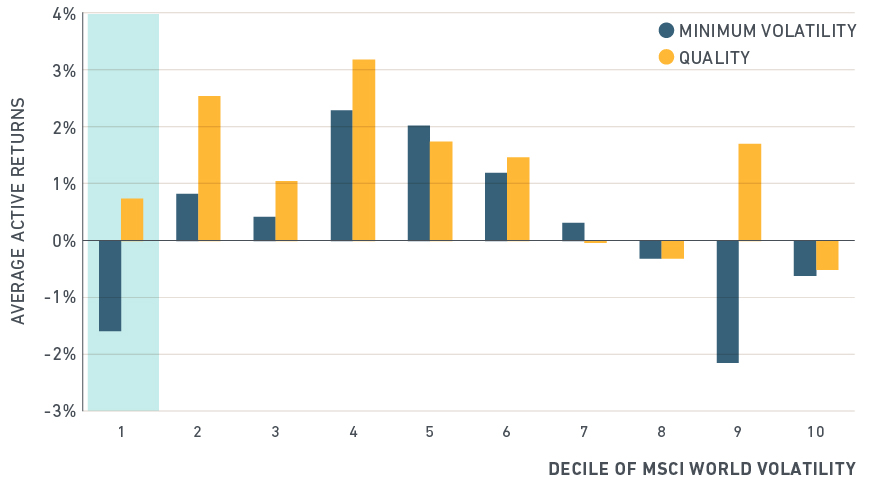

Minimum Volatility, like Quality, is typically a strategy with defensive characteristics. Through June, however, the World Minimum Volatility Index posted a modest negative active return while the MSCI Quality Index decoupled and outperformed.

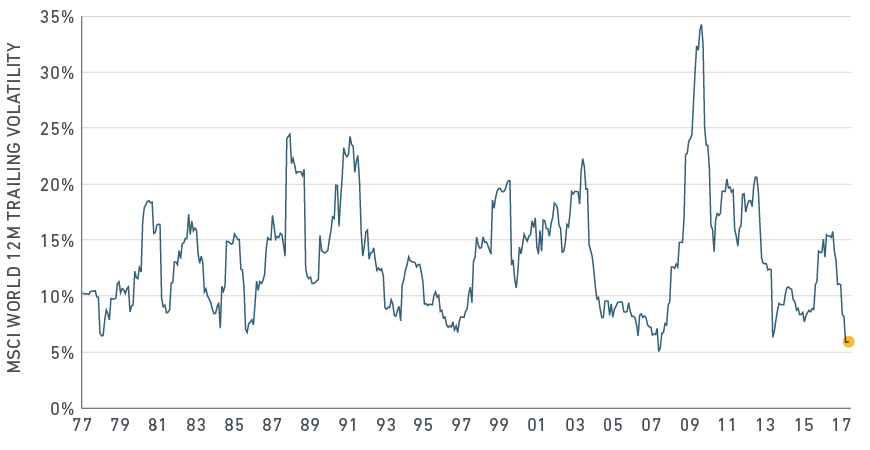

Amid central banks’ unconventional involvement in financial markets since 2008, the volatility of markets, earnings and bond yields have been compressed, and both bond and equity returns have risen. The MSCI World Index’s trailing 12-month volatility recently fell below 5.5%, its lowest level since the record 5.1% in May 2007. Based on the past 40 years, it is not uncommon for Minimum Volatility and Quality to decouple during periods of extremely low market volatility.

MSCI World Volatility Near an All-Time Low

MSCI data, 1975 to 2017

MSCI Minimum Volatility and Quality indexes Decouple When Market Volatility is Lowest

MSCI data, 1975 to 2017

Arguably, the inflation of asset prices and collapse in market volatility prompted by central-bank policies have dampened the price-discovery process, so corporates with weaker fundamentals may have had (artificially) much lower volatility on an absolute and relative basis. This could be why investors have recently preferred companies that have stronger fundamentals.

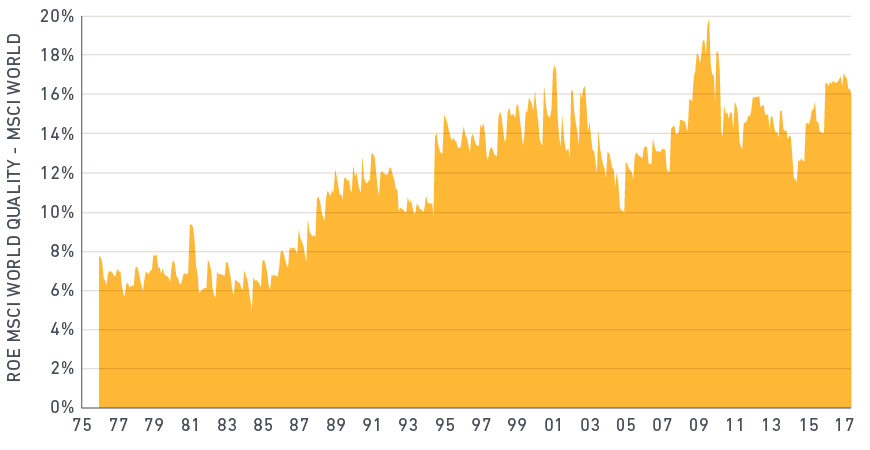

High profitability has been a key driver of MSCI World Quality Index outperformance. From a historical perspective, shown in the plot below, the ROE spread of the MSCI World Quality index versus its parent index is close to the highest levels spanning our dataset.

Profitability of Quality Stocks Nears All-Time High

MSCI

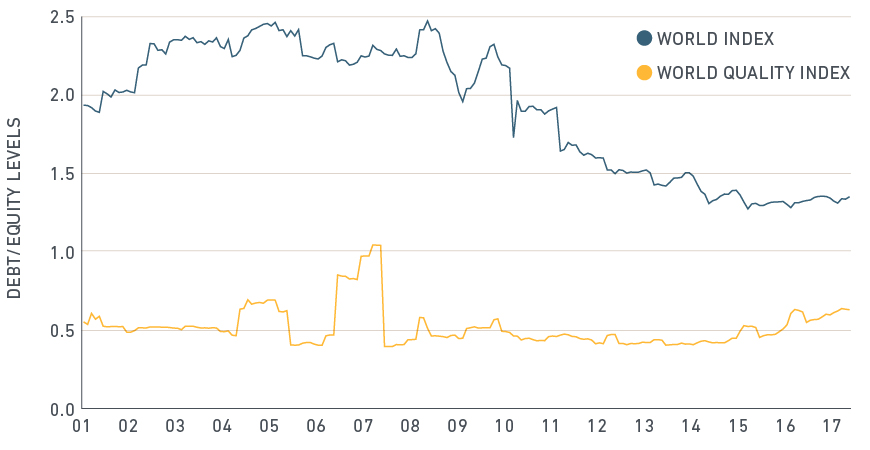

What are the risks for quality stocks? For one, the sustainability of high ROEs is an open question. ROE is also sensitive to levels of corporate leverage, and while debt/equity levels for the broad market are down, for quality stocks they have started to rise. In addition, Quality companies are very sensitive to changes in revenues.

Corporate Leverage Among Quality Stocks Has Started To Rise

MSCI

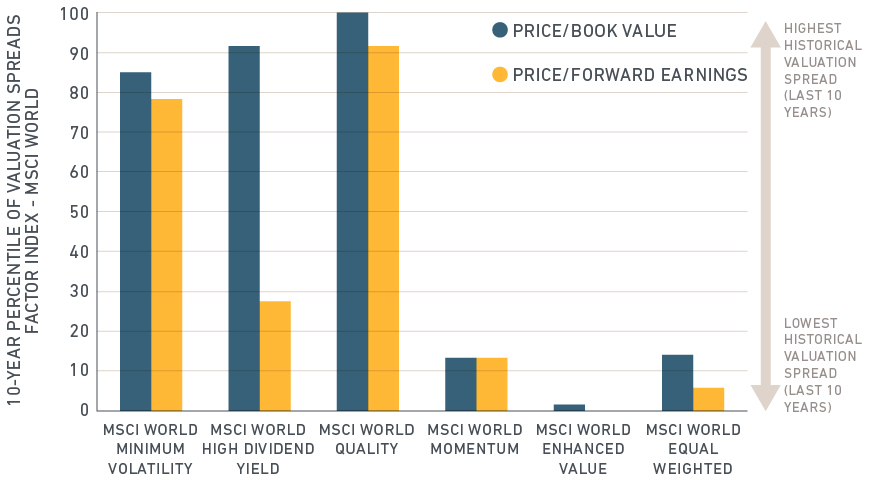

Meanwhile, comparing price/book and price/forward earnings (as of June 30, 2017) of factor indexes relative to the MSCI World Index over the past 10 years shows that the MSCI World Quality Index is priced at the top of its historical range on both metrics, while the MSCI World Enhanced Value, Equal Weighted and Momentum Indexes are close to their bottoms.

There is no guarantee that Quality stocks won’t appreciate further, of course, but given their performance institutional investors may want to ask: is it time to revisit quality factor fundamentals?

Twin peaks in Quality valuation spreads

MSCI Data, June 2007 to June 2017

Further Reading

Measuring the impact of factors

Bridging the gap: adding factors to indexed and active allocations