As Credit Risk Rises, Beware of Selection Bias in CLOs

Blog post

June 1, 2018

Investors in the booming U.S. Collateralized Loan Obligation (CLO) market likely need to be aware of the risks: record tight spreads,1 deteriorating credit quality, and, as our expanded CLO data analytics reveal, selection bias risk.

The U.S. CLO market achieved a new record in 2017. New issuance exceeded USD 240 billion and reset and refinancing deals were about twice 2016's volume. However, the credit quality of CLO collateral has been deteriorating. The exhibit below shows the trend in the weighted average credit rating factor ("WARF") for CLO collateral. WARF at issuance2 has been deteriorating significantly in recent years, especially since 2015, while WARF for seasoned deals has also been worsening steadily as they age.3 With securitization risk retention rules being repealed, WARFs may deteriorate further.

Credit quality has declined for both new and existing CLOs

Source: MSCI, INTEX

The leveraged loan market has seen similar credit deterioration in recent years. It is not clear, however, whether the collateral supporting CLOs is better or worse than for the loan universe in general. Nevertheless, selection bias was highlighted as one of the key drivers of the big deterioration in securitized loan performance during the 2008 financial crisis. We now use MSCI's enhanced CLO data analytics to investigate the extent of selection bias in the current market.

MSCI Securitization Research has matched CLO security loan data with IHS Markit proprietary bank loan data.4 The resulting enhanced CLO analytics are based on loan-level pricing and credit characteristics, including loan covenants. Our matching algorithms cover about 80% of CLO collateral.

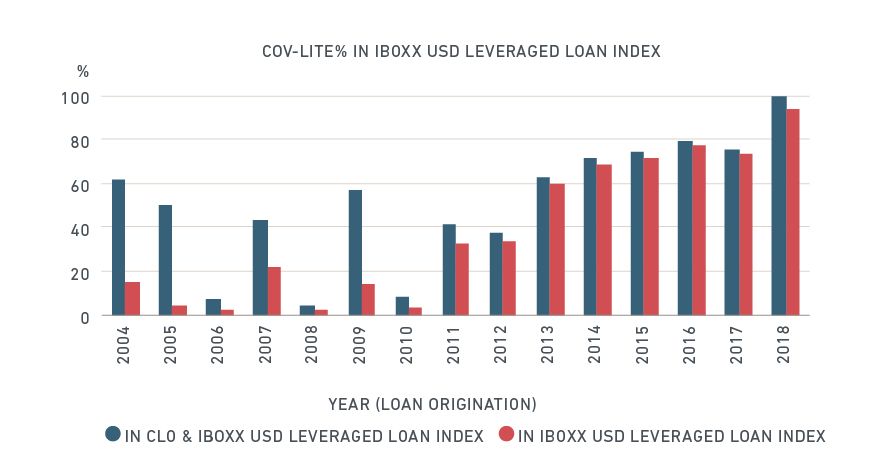

Historically, loan covenants provided investors with additional default and loss protection. However, in recent years, less restrictive covenant ("cov-lite") loans have become widespread in the loan universe as well as in CLO collateral. The next exhibit shows that proportion of cov-lite loans in the CLO universe have been marginally higher than in the total loan universe.

Proportion of cov-lite CLOs exceed those in total loan universe

Source: MSCI, IHS Markit

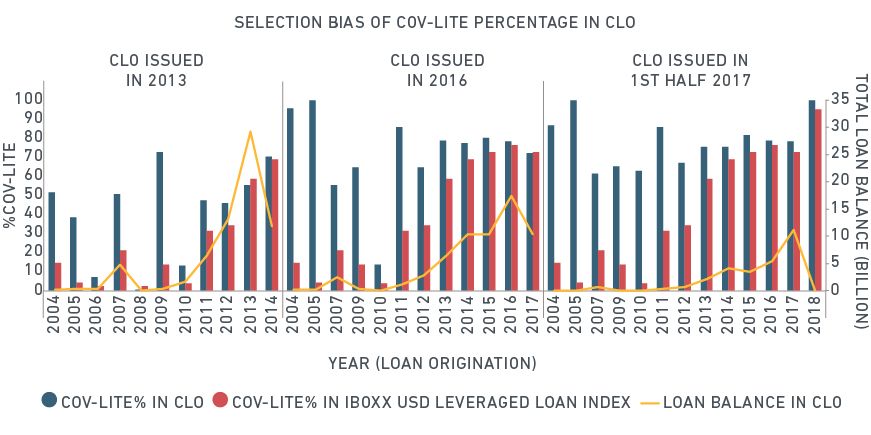

We used our expanded data tools to investigate potential selection bias. The final exhibit groups loans in CLOs and in the loan index based on the year of CLO issuance and loan origination. For loans originated around the same time as the CLO issuance, the cov-lite percentages were higher for CLOs than for similar age loans in the loan index. The gap has increased for recent CLO vintages. For seasoned loans, the cov-lite percentages have been much higher in the CLOs than for loans of a similar age in the loan index. Again, as more seasoned loans have been included in recent CLOs, the cov-lite gap has increased. These seasoned cov-lite loans were at the higher end of the risk spectrum when originated. As a result of these selection bias issues, the credit quality of loans in CLOs is generally lower than for loans of a similar vintage in the loan universe; the gap is increasing for recent vintages.

Issuers have added more seasoned cov-lite loans in recent CLO vintages

Source: MSCI

Our analysis indicates that selection bias is present in today's CLO market. Given uncertainties in the credit cycle and the tapering of monetary policy, investors may want to heighten their monitoring of collateral credit quality.

The author thanks Yini Yang for her contribution to this blog post.

1 See, for example, CLO Weekly, April 20, 2018, Bank of America Merrill Lynch Securitized Products Strategy Global

2 For example, the Moody's Ba1/speculative grade, B1/Highly speculative grade, Caa1/Substantial risks grade, may correspond to 940, 2220, 4770 WARFs.

3 An increase in the weighted average indicates a deterioration in credit quality,

4 "MSCI Expands Syndicated Loan Risk Analytics using IHS Markit Pricing and Reference Data." MSCI press release, Nov. 1, 2016.

Further reading

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.