Extended Viewer

Sustainability Bond Indexes Were Resilient amid Market Turmoil

We have found in previous studies that stocks and bonds of companies that were more resilient to sustainability-related risks (as measured by MSCI ESG Ratings) exhibited lower market volatility, suggesting they could fare better during periods of market stress, as they did during the COVID-19-driven sell-off in March 2020. Through the initial market turmoil that followed the U.S. tariff announcements on April 2, we tested whether this resilience would hold true for corporate bonds.

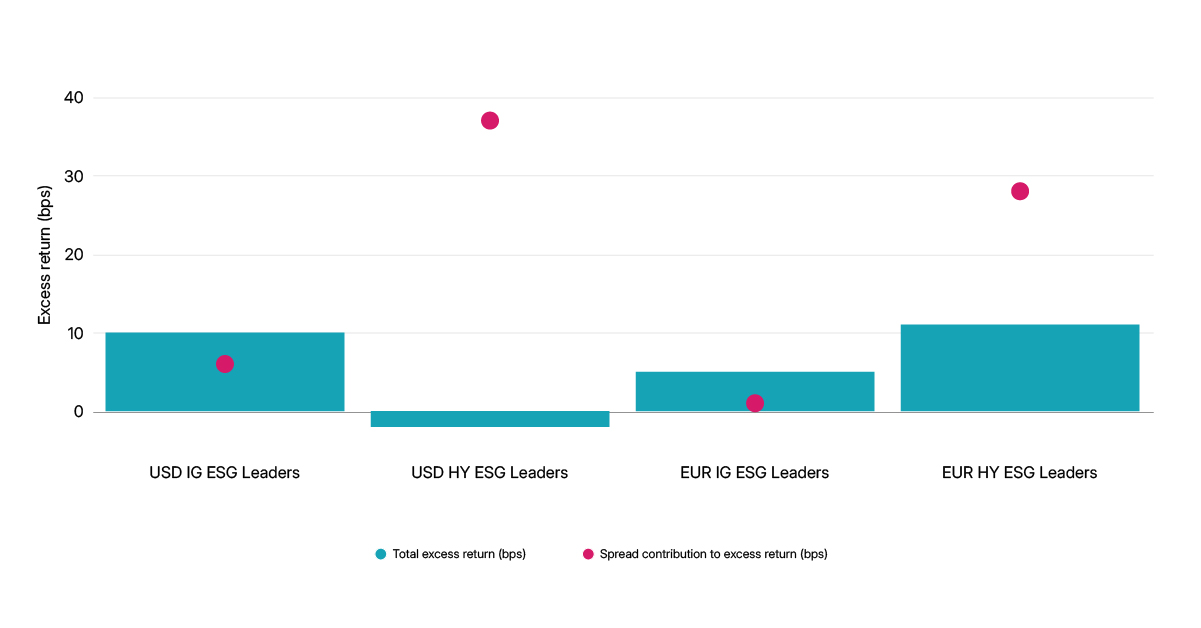

Between March 31 and April 11, 2025, we found that the MSCI Investment Grade (IG) and High Yield (HY) ESG Leaders Corporate Bond Indexes outperformed their parent indexes — in both USD and EUR (except for USD HY). Relative spread movement against the benchmark was the primary positive contributor to the excess return in all indexes, however, underscoring sustainability strategies’ potential in managing downside risks during stress.

Why might higher-sustainability-rated bonds behave more defensively?

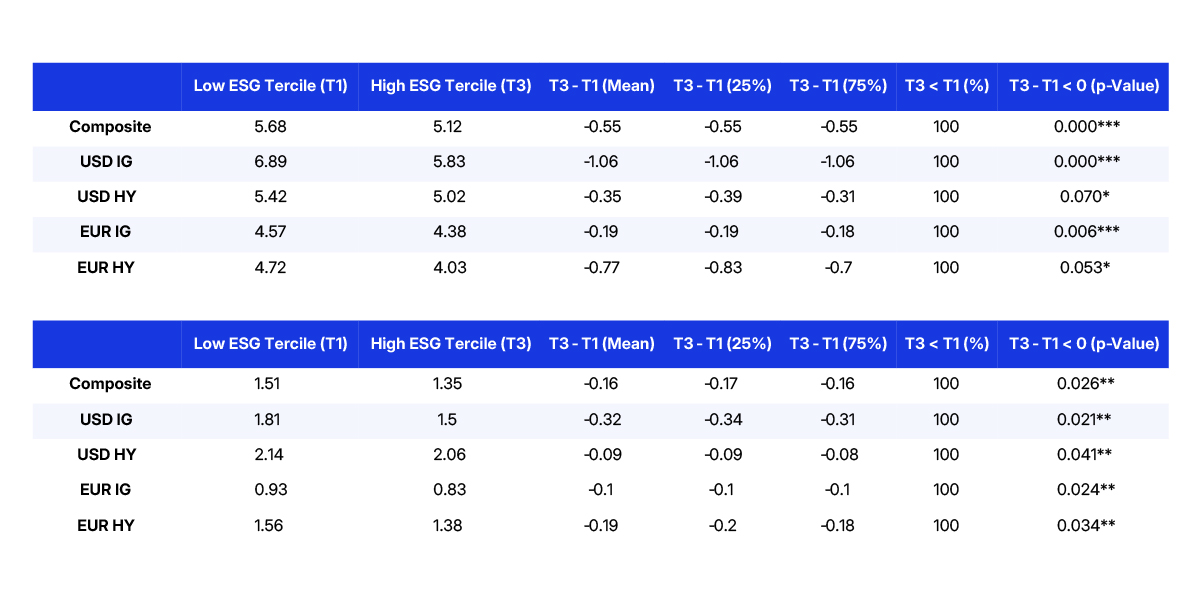

We previously found that companies with higher ratings showed stronger fundamentals — such as higher profitability and credit quality — and their outstanding bonds displayed lower systematic and idiosyncratic volatility. Their bonds, within their respective credit-quality universe, also less frequently experienced sharp price declines, suggesting they may provide additional information on top of traditional credit-quality assessments and be a useful tool for credit investors, especially during periods of market stress.

How sustainability corporate-bond indexes fared vs. broader indexes in wake of US tariff announcements

Higher-sustainability-rated companies had lower systematic and idiosyncratic risk