Are Low Yields a Risk for your Private Real Estate Portfolio?

Blog post

June 8, 2017

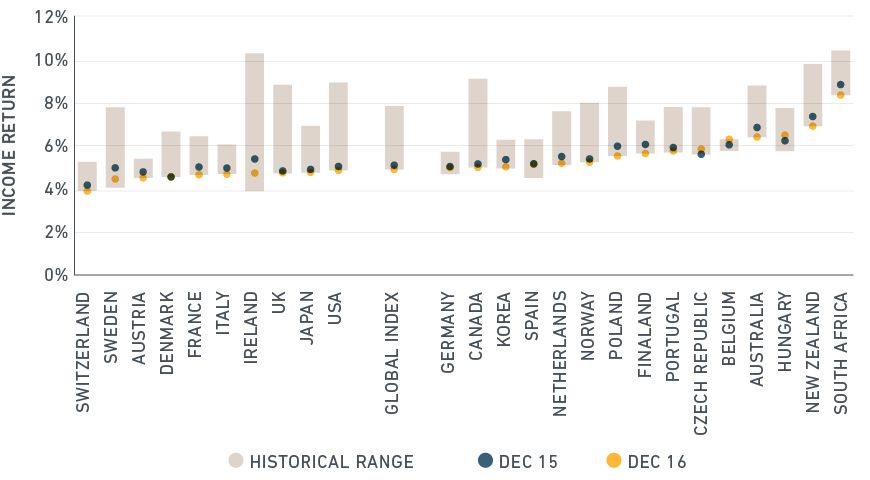

In a global environment of sluggish growth and low interest rates, yields on private real estate are under sustained pressure. Yields have been compressing since 2010 and are now lower than before 2007. Do these historically low yields represent a risk to portfolios? The answer largely depends on how one defines risk, but low yields do pose challenges for commercial real estate investors. Since 2008, policymakers across the developed world have slashed interest rates to record lows and employed unconventional tactics such as quantitative easing to reflate asset values and bolster sagging economies. While many economies remain sluggish, low rates have helped boost real estate prices by lowering both borrowing costs and discount rates on future operating income. As asset values have grown, yields have compressed. In 2016, the income return on the MSCI IPD Global Annual Property Index fell below 5% for the first time since its inception. Income returns are now at the low end of their historical ranges across many of the world's real estate markets.

Yields on real estate are at record lows in most markets

Income return histories shown here vary between 11 and 36 years depending upon individual market availability. Source: MSCI – Global Intel

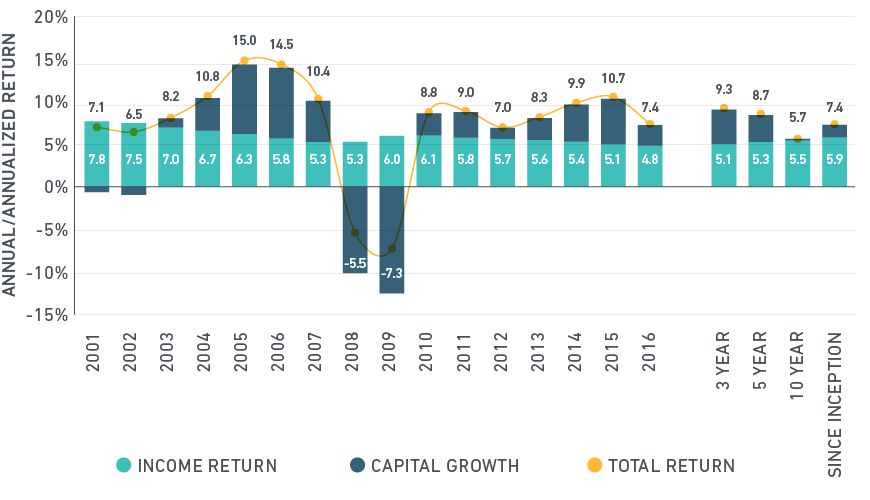

In the short term, low yields might be considered a risk factor for investors with higher total-return expectations. Historically, income returns have been relatively stable and made up a sizeable portion of the long-term return from direct investment in private real estate. Faced with falling yields, investors wanting to maintain higher total-return targets will be more reliant on capital growth tied to increases in net operating income (NOI).

Income comprises about 80% of long-term MSCI IPD Global Annual Property Index total returns

Source: MSCI – Global Intel

Longer term, it is not clear whether the shift toward lower real estate yields is sustainable. With the Federal Reserve raising U.S. interest rates again, there are concerns about a repricing of real estate assets. Rising rates could be bad for bond values, due to a discount-rate effect, but the prognosis is not as clear for real estate assets. Unlike bonds, cash flows from real estate are not fixed. Lower vacancies, higher rents or lower operating expenses can all help to boost NOI, and thus values.

For real estate, the cash-flow effect tends to dominate the discount-factor effect, making real estate values more sensitive to growth than to interest rates. Thus, the impact of rising rates on real estate values will probably depend on whether 1) rates rise in response to improved growth; 2) rates rise to curb inflation in a stagflation scenario; or 3) rates rise too soon, stifling growth. In the first scenario, stronger growth could result in rising NOI levels, which could offset the impact of higher interest rates. In the latter scenarios, the risks to real estate values are greater thanks to low growth prospects.

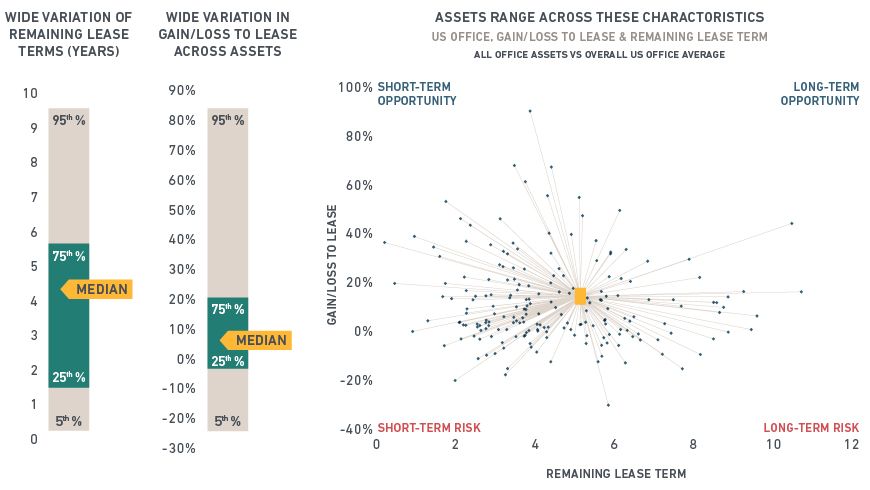

Asset specifics matter too. Some assets have growth potential even if the local market does not. For assets where existing rents are below market rents, there is potential for gains to be realized when leases expire and new ones are negotiated. The remaining duration of existing leases will determine how quickly potential growth can be realized. The sample of U.S. office assets below highlights how individual assets can experience vast differences in their income growth potential.

Wide variations exist in lease structures and income growth potential

Source: MSCI – IRIS

Given the diverse and unique nature of individual real estate assets, the risks faced by investors will vary greatly. For some investors, such as those with a high exposure to rents that are above market levels, low yields represent more of a risk than for others. Informed real estate investors may want to take a close look at their portfolios to see how they are positioned.

Further reading:

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.