面包屑导航

导航菜单

- MSCI ESG Focus Indexes

- Currency Hedged

-

Market Cap Weighted

- MSCI全市场指数

- MSCI China A Inclusion Indexes

- MSCI China All Shares Indexes

- MSCI China A International Indexes

- MSCI ASEAN Indexes

- MSCI Emerging Markets ex China Index

- MSCI US Equity Indexes

- MSCI Indexes for Canadian Investors

- MSCI Saudi Arabia Indexes

- MSCI US REIT Custom Capped Index

- MSCI Indexes for Australian Investors

- MSCI USA IMI Sector Indexes

- MSCI可投资市场指数

- MSCI新兴市场和前沿市场指数

-

Factors

- MSCI Single Factor ESG Reduced Carbon Target Indexes

- MSCI Factor Mix A-Series Indexes

- MSCI Diversified Multiple-Factor Indexes

- MSCI股息

- Índice MSCI All Colombia Local Listed Risk Weighted

- MSCI High Dividend Yield

- MSCI因子指数

- MSCI Equal Weighted Indexes

- MSCI Select Value Momentum Blend Indexes

- MSCI质量和高红利指数

- MSCI Top 50 Dividend Indexes

- MSCI最小波动率指数

- MSCI Growth Target Indexes

- MSCI风险加权指数

- Índices MSCI Mexico Select Momentum Capped & Mexico Select Risk Weighted

- Additional Index Profiles

MSCI Factor

MSCI factor indexes

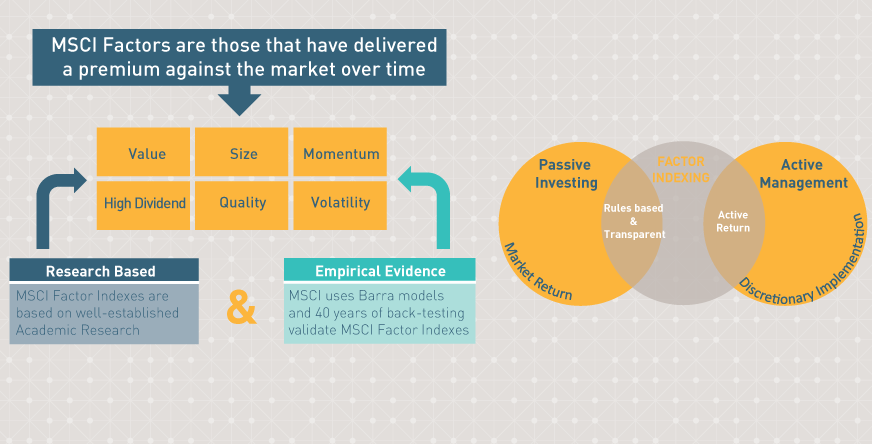

The MSCI factor indexes are rules-based indexes that capture the returns of systematic factors that have historically earned a persistent premium over long periods of time—such as Value, Low Size, Low Volatility, High Yield, Quality and Momentum and Growth.

Approximately USD 236 billion in assets are estimated to be benchmarked to MSCI Factor Indexes1

1 Data as of December, 2017 and reported as of March, 2018 by eVestment, Morningstar, Bloomberg and MSCI.

PERFORMANCE, FACTSHEETS AND METHODOLOGIES

Factor indexes (select your index by choosing the appropriate Indexes in the drop down menu)

MSCI USA Momentum SR Variant Index

Performance | Factsheet | Methodology

MSCI USA Enhanced Value Index

Performance | Factsheet | Methodology

MSCI USA Sector Neutral Quality Index

Performance | Factsheet | Methodology

MSCI USA Low Size Index

Performance | Factsheet | Methodology

MSCI World ex USA Sector Neutral Quality Index

Performance | Factsheet | Methodology

MSCI World ex USA Momentum Index

Performance | Factsheet | Methodology

MSCI World ex USA Enhanced Value Index

Performance | Factsheet | Methodology

MSCI World ex USA Low Size Index

Performance | Factsheet | Methodology

MSCI USA Quality GARP Select Index

Performance | Factsheet (USD) | Methodology

MSCI Emerging Markets Value Factor Select Index

Performance | Factsheet (USD) | Methodology

MSCI Emerging Markets Quality Factor Select Index

Performance | Factsheet (USD) | Methodology

MSCI ACWI Quality Index

ADDITIONAL INSIGHTS AND RESEARCH

Value:

Research Insight - Finding Value: Understanding Factor Investing

Quality:

Research Insight - Flight to Quality: Understanding Factor Investing

Momentum:

Research Insight – Riding on Momentum

Size:

MSCI Low Size Indexes Brochure

Research Insight - One Size Does Not Fit All: Understanding Factor Investing

GARP (Growth at a Reasonable Price):

What drives the capacity of factor index strategies?

What drives the capacity of factor index strategies?

As factor investing becomes increasingly “business as usual,” institutional investors have become keenly interested in the ability of strategies that replicate factor indexes to persistently capture the desired exposures.

ALL FAANGS ARE NOT CREATED EQUAL

ALL FAANGS ARE NOT CREATED EQUAL

FAANG stocks make up nearly 40% of the NASDAQ 100 index, and smaller but significant weights in many others. Commonly grouped as tech stocks or growth companies, it seems reasonable to assume they share many similar characteristics. However, when examined through the lens of performance-driving factors, their characteristics are far from homogeneous.

WHAT IS GOING ON WITH FACTOR RETURNS?

WHAT IS GOING ON WITH FACTOR RETURNS?

Value and momentum factors typically move in opposite directions — that is, when one outperforms the market, the other usually underperforms. However, as both factors have underperformed the market, several publications are beginning to question whether this change in market behavior is impairing quantitative strategies.