面包屑导航

导航菜单

- MSCI ESG Focus Indexes

- Currency Hedged

-

Market Cap Weighted

- MSCI全市场指数

- MSCI China A Inclusion Indexes

- MSCI China All Shares Indexes

- MSCI China A International Indexes

- MSCI ASEAN Indexes

- MSCI Emerging Markets ex China Index

- MSCI US Equity Indexes

- MSCI Indexes for Canadian Investors

- MSCI Saudi Arabia Indexes

- MSCI US REIT Custom Capped Index

- MSCI Indexes for Australian Investors

- MSCI USA IMI Sector Indexes

- MSCI可投资市场指数

- MSCI新兴市场和前沿市场指数

-

Factors

- MSCI Single Factor ESG Reduced Carbon Target Indexes

- MSCI Factor Mix A-Series Indexes

- MSCI Diversified Multiple-Factor Indexes

- MSCI股息

- Índice MSCI All Colombia Local Listed Risk Weighted

- MSCI High Dividend Yield

- MSCI因子指数

- MSCI Equal Weighted Indexes

- MSCI Select Value Momentum Blend Indexes

- MSCI质量和高红利指数

- MSCI Top 50 Dividend Indexes

- MSCI最小波动率指数

- MSCI Growth Target Indexes

- MSCI风险加权指数

- Índices MSCI Mexico Select Momentum Capped & Mexico Select Risk Weighted

- Additional Index Profiles

DMF hero image

Diversified Multi-Factor Indexes

MSCI diversified multiple factor indexes

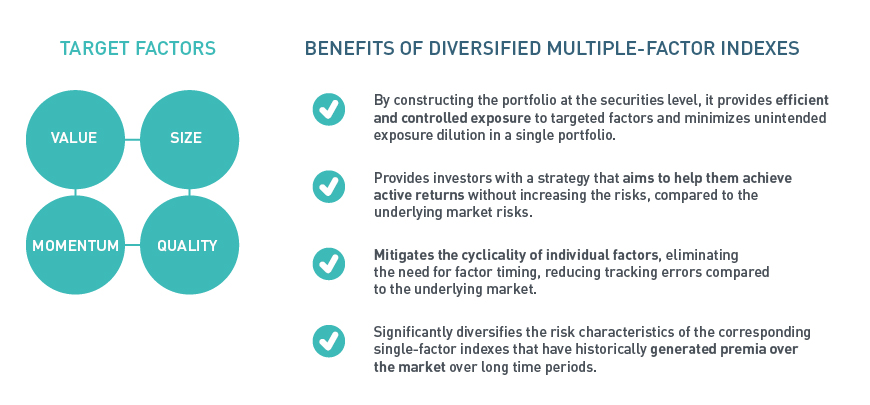

MSCI Diversified Multiple-Factor Indexes use the Barra product risk tools to construct indexes that track the performance of four factors – Value, Momentum, Quality and Low Size – which have, over time, provided higher return than the overall market while keeping risk at the level of an underlying parent index.

The innovation is in capturing optimal exposure to a diversified set of factors while aiming to keep risk similar to that of the market. These indexes can be used by investors looking to construct diversified portfolios that are exposed to multiple factors.

Diversified factor performance of GICS-based sector indexes

MSCI USA Diversified Multiple-Factor Capped Sector Indexes are based on parent indexes containing U.S. large and mid-cap securities within nine individual MSCI USA sector indexes. The indexes aim to maintain a risk level similar to the parent index while maximizing overall exposure to four target factors, so that institutional investors can benefit from the improved performance of combining factors while expressing single sector views. The issuer-level weights of the constituents are capped at 25%.

PERFORMANCE, FACTSHEETS AND METHODOLOGIES

MSCI Diversified Multiple-Factor Indexes

MSCI ACWI Diversified Multiple-Factor Index

MSCI Emerging Markets Diversified Multiple-Factor Index (USD)

MSCI World ex USA Diversified Multiple-Factor Index

MSCI World ex USA Small Cap Diversified Multiple-Factor Index

MSCI USA Diversified Multiple-Factor Index

MSCI USA Mid Cap Diversified Multiple-Factor Index

MSCI USA Small Cap Diversified Multiple-Factor Index

MSCI DIVERSIFIED MULTIPLE-FACTOR CAPPED SECTOR INDEXES

MSCI USA Energy Diversified Multiple-Factor Capped Index

MSCI USA Materials Diversified Multiple-Factor Capped Index

MSCI USA Industrials Diversified Multiple-Factor Capped Index

MSCI USA Consumer Discretionary Diversified Multiple-Factor Capped Index

MSCI USA Consumer Staples Diversified Multiple-Factor Capped Index

MSCI USA Health Care Diversified Multiple-Factor Capped Index

MSCI USA Financials Diversified Multiple-Factor Capped Index

MSCI USA Information Technology Diversified Multiple-Factor Capped Index

MSCI USA Utilities Diversified Multiple-Factor Capped Index